US equity markets are still in positive territory this year, with the NASDAQ 100 up nearly 30%, albeit this is largely attributable to a handful of companies benefitting from recent AI related gains.

And… the widely expected surprise! UK Interest rates rose by 0.5% in June as the May inflation figures did not budge from the 8.7% CPI figure recorded in the previous month. Core inflation also rose from 6.8% in April to 7.1%.

While many in the media portrayed this as a “shock” interest rise, completely out of the blue, investors had in fact already priced in a 40% probability and therefore markets did not react too badly.

Still, perhaps we should be thankful – this month the Turkish Central Bank raised its own base rate by 6.5% in one jump in the face of an inflation figure of 39.6%!

Both the Bank of England and Prime Minister Rishi Sunak (who promised to get inflation down by half by the end of this year) are now in a difficult situation. With the UK consumer growing frustrated and higher mortgage rates progressively stripping more income from UK pockets, how do they propose bringing inflation under control?

One area of focus for Sunak is the controversial block on public sector pay rises. The disputes over public sector pay continue and we are likely to see more disruption from strikes ahead. Fiscal policy (raising taxes or cutting government spending) is the only other option, but this will not be a popular alternative with a general election on the horizon.

As we discuss later, one of the main issues affecting the UK economy is the tightness of its labour market. Unemployment for the first quarter of the year was 3.9% and average wage growth excluding bonuses was still high at 5.8% (albeit below inflation). Interest rates are likely to stay “higher for longer” and this data again highlights a structural problem in the UK, an ageing population and a declined workforce leading to wage growth.

UK equity markets dropped over the past month and while the FTSE 100 and FSTE All Share are still in positive territory this year, they have given up much of their gains as the economic outlook worsens.

Elsewhere in the world, China (where the economic recovery has not been smooth sailing) has experienced large depreciations in its domestic currency, the Renminbi, against the US Dollar. Some of this is a function of rising US interest rates at a time when Chinese interest rates are falling. Investors are also doubtful of the country’s economic fundamentals which they believe will not hold up.

With economic exports dropping last month by 7.5% YOY, a depreciating currency will help to make the country’s exports more competitive. However, a key risk is again present in the property sector (remember Evergrande?).

Chinese property companies hold large amounts of offshore debt which they repay in US Dollars. A weaker currency makes the interest on this debt more expensive, putting further pressure on companies.

This uncertainty has been reflected in Chinese equity markets. Having started the year so positively amid the economic reopening, the period between April and June has a continuous downward slope. Markets did react positively to recent central bank interest rate cuts which helped to reverse some of these losses.

Areas of focus

- Due to the “inverted yield curve” (which we cover later) the yield on the UK 10 year Gilt has risen by 9% over the last month while the 2 year yield has risen by 20%. Despite the resulting capital loss, the 2 year yield offers a yield advantage and a lower volatility and is preferred for income.

- Japanese equities are the preferred developed market asset. With more compelling economic fundamentals and structural reforms coming into play again, the Nikkei 225 has risen by over 27% YTD.

- Emerging market (EM) equities are preferred over developed market equities in the short-term as these economies are generally later in their monetary policy cycle, and interest rate cuts are expected in order to stimulate growth.

- Emerging market debt is also looking attractive. A bottom-up selection is required here due to the various differences between individual emerging countries and their debt types.

- US equity continues to steam ahead, recovering most of the losses experienced last year. These values likely do not reflect potential earnings damage in a recessionary environment, which is a risk.

- UK equities face headwinds as interest rates look to keep rising, likely strengthening the pound.

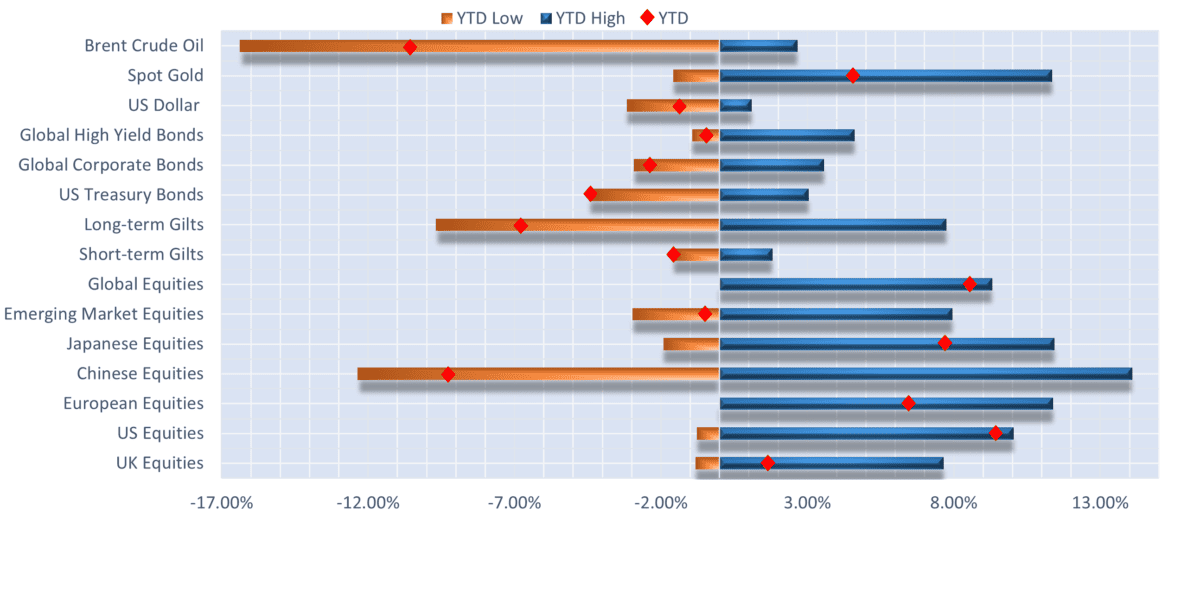

Selection of assets YTD returns and YTD range of returns as at 07.07.2023 (the two ends of the bars represent the range of YTD returns and the red dots represent the current YTD return). Indexes used: FTSE All-Share, Russell 3000, STOXX Europe 600, MSCI China, MSCI Japan, MSCI Emerging Markets, FTSE UK Conventional Up To 5 Years, FTSE UK Conventional Over 15 Years, ICE BOFA US Treasury, ICE BOFA Global High Yield, ICE BOFA Global Corporate, US Dollar Index, Spot Gold, Brent Crude Oil. Returns hedged back to GBP with exception of Spot Gold, Brent Crude Oil and US Dollar which are in US Dollar terms. Data from FE Analytics and MarketWatch. Correct as of 07.07.2023.

UK

The Bank of England raised interest rates by 50 basis points in June, bringing the UK base rate up to 5% – the highest since 2008. The bank was forced to make a reversal back to higher rates after inflation data for May showed that CPI stayed at 8.7%, higher than expected for the fourth consecutive month. In addition, core inflation (CPI minus the cost of food and energy) increased by 7.1% in the 12 months to May 2023, up from 6.8% in April – itself the highest rate since 1992.

While this is better news for savers, with a return of over 5% now available in fixed term deposit accounts, the real value of this cash is still being eroded by higher inflation. As an asset cash has only been such an attractive alternative to equities twice this century: during the dotcom bubble and just before the 2008 financial crash.

During these events in 2000 and 2008, markets were almost instantly calmed with interest rate cuts. With inflation persisting at the current high levels, loose monetary policy by central banks is not possible – and yet economies are still proving reasonably resilient.

The UK is struggling in its inflation battle and has a much bigger inflation issue than other developed economies. The main initial drivers of global inflation have been tamed, namely the COVID-19 supply-side issues, lax monetary policies, and high energy costs (to some extent).

However, second-round inflation effects are now feeding into core inflation in the UK. Rising inflation expectations and a tight labour market are leading to wage growth and companies appear to have maintained their pricing power, passing on higher costs to consumers while preserving or boosting their profit margins.

The UK is therefore somewhat stuck on an inflation and labour roundabout. Companies are reluctant to let go of workers over the fear they will be unable to hire them back. This in turn means that in order to maintain the same profit margins, they are raising their prices for consumers.

The most recent housing market data shows that a typical five-year fixed mortgage deal now has an interest rate of over 6%. Despite calls for help, Rishi Sunak has ruled out extra support for UK homeowners struggling to afford the soaring mortgage costs. The rationale for this is that by supporting consumers income, it is likely to feed into higher inflation figures, exacerbating and prolonging the problem.

Recent OECD data shows that only 28.04% of the UK population owned a property with a mortgage in 2020, down from 35.48% in 2010. In addition, fixed-rate mortgages are now more popular than flexible ones, where higher interest rates impact households’ purchasing power almost instantly. OECD data shows that floating rate mortgages have decreased from over 70% in 2011 to only around 10% this year. This shift in the housing market is creating a longer lag than usual and could explain why interest rates are not yet being as effective as expected in reducing consumer spending.

That said, UK households withdrew a record amount from bank accounts in the past month. A net £4.6bn was taken out from banks and building societies in May, the highest level of withdrawals since records began in 1997, according to recent Bank of England data. This provides strong evidence that people are dipping into their excess savings built up during the pandemic to sustain their living standards – ultimately a finite resource.

If the latter is the case, inflation may stay elevated until these savings are extinguished. What all of the above points to is inflation settling above the Bank of England’s 2% CPI target and higher interest rates for longer. This in turn puts more pressure on the economy and means certain areas of the UK market, namely smaller companies, lower quality corporate bonds and longer-term gilts will experience a subdued performance.

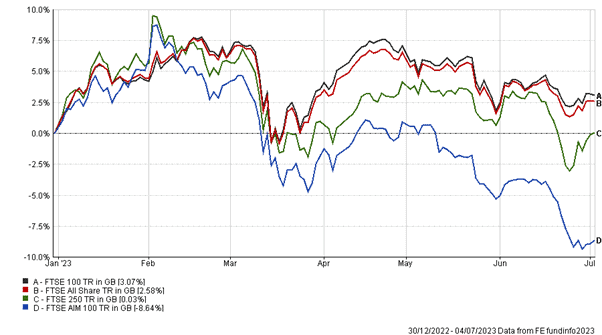

YTD performance of UK equity markets

UK equities have been struggling in recent weeks, pricing in higher downside risk. The FTSE AIM index of smaller companies has given up all of its gains from the first quarter and now sits at -8.64% when compared with the start of the year. Since the beginning of 2022, the FTSE AIM is down over 38% and there are very few signs this will improve in the short-term. Usually when UK equities have fallen in value, private equity firms see this as a good opportunity to takeover these firms. With higher interest rates and a stronger pound this will prove trickier, but is still a risk for UK companies.

A stronger currency, falling oil prices and the Bank of England’s hawkish interest rate policies have all damaged major UK indices in Q2 2023. The FTSE 100, rich in oil majors and cash generative value stocks, has completely missed out on the recent hype surrounding artificial intelligence. Over the long-term, AI technology stocks and clean energy stocks should outperform. The UK is lacking in this area, despite the recent political moves to make the UK more attractive to companies in these sectors.

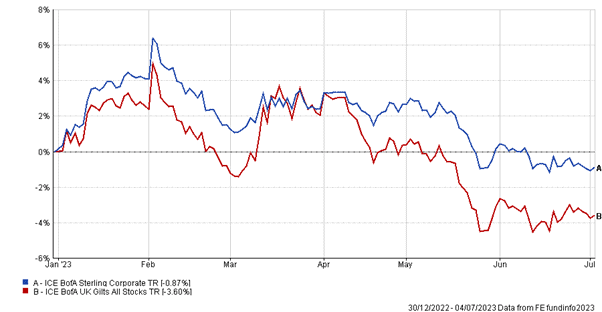

YTD performance of UK bond indices

As shown above, UK bond prices have fallen significantly since the start of the year, reflecting the continually-changing outlook for interest rates. Corporate bonds have held up better than government bonds due to their higher coupon rates.

The yield curve is becoming increasingly inverted – i.e. lower interest rates paid on longer-dated bonds, which is the reverse of the normal trend – which is usually a sign that a recession is on the horizon (see US section below).

US

US equities continue to rally as optimism sneaks back into the market. The three major US stock market indices – the S&P 500, the NASDAQ 100 and the Dow Jones Industrial Average – all rose during the month, gaining 5.51%, 5.15%, and 5.94% respectively. So far this year these indices are up 16.6%, 39.35%, and 6.27% respectively.

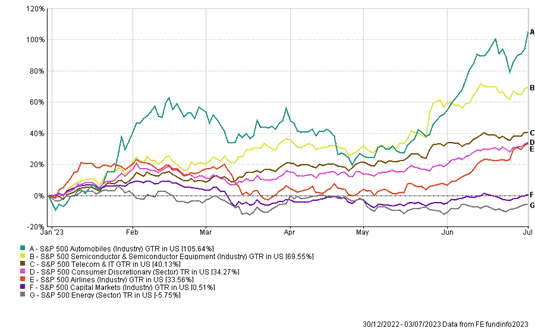

YTD performance of select S&P 500 industries

As the above chart shows, industries which benefit from a growth environment are climbing high. Automobile stocks (which tend to be a discretionary purchase) have shot up, likely led by Tesla’s improved financial results and its decision to lower prices to attract demand. Telecom and IT have also clearly benefited from the recent AI trend, and have semiconductor businesses, which are needed for the hardware underpinning the AI technology itself.

Hope of a recession-free year seems to emerge and fade each time economic data is released, as inflation appears to be coming down whilst unemployment remains low.

However, there are mixed views on this. Some view a possible high employment recession where economic growth deteriorates, but companies retain their employees as they fear they will not be able to hire them back owing to a labour shortage.

Those investors who do not believe a recession is approaching are actively taking positions in developed equities, helping to drive the recent rally. On the other hand, those who consider a recession is imminent are assessing what is priced into assets presently and in our view, it is this latter risk (of recession) which is not fully priced into market valuations.

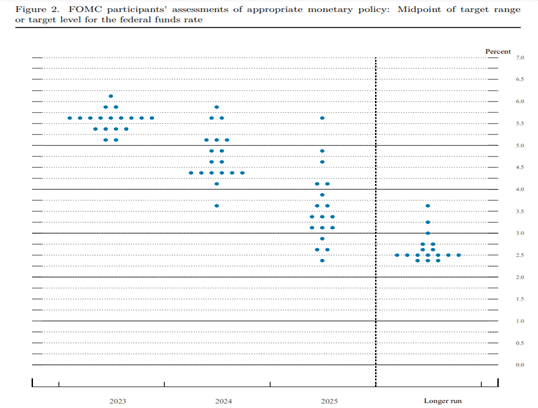

For the first time since March 2022, the Chair of the US Federal Reserve Jerome Powell decided not to increase interest rates further. Instead the Fed decided to “skip” in their last meeting, opting to keep their benchmark rate at 5.25% while signalling to markets that rate cuts are not on the cards. They currently expect two more 25 basis point rate hikes before year end. This extremely hawkish stance is intended to prevent a stop-start inflation fight.

While a skip may seem confusing when the Fed have indicated that they will continue to raise interest rates regardless, the reasoning is due to the time delay between an interest rate rise and the consequent impact on the markets and consumer behaviour.

Typically, a change in interest rates takes around 18 months to have its desired effect. Therefore, the Fed’s likely rationale is to take a month to see what the economic situation looks like before proceeding. In the unlikely event the outlook is deemed positive, or at least more positive compared with current conditions, then they may decide to step back from future rate hikes. At present this seems highly unlikely given their recent forecast for interest rates (see dot plot below).

Markets view this as fairly redundant information because the Fed can monitor the economy and raise rates at the same time. It is effectively the sum total of interest rate hikes that is important, not necessarily the path taken to get there.

Dot plot from Federal Reserve Board June 2023 meeting (www.federalreserve.gov)

As the dot plot above shows, 12 of the Federal Open Market Committee board members forecast interest rates to be above their current rates at the end of 2023. They then forecast that in 2024 interest rates will drop slightly, but over the longer term rates will be above what we have seen since the 2008 financial crisis.

Year on year CPI inflation dropped from 4.9% in April to 4.0% in May. Over May, the monthly figure rose slightly by 0.1%. The Feds preferred measure, core inflation, which excludes the more volatile food and energy items, decreased from 5.5% to 5.3%. This difference can be attributed to the decline in the price of energy, with crude oil trading at over $110 a barrel a year ago as opposed to $70 today.

The price of crude oil has decreased over the last 12 months due to a number of factors; the US draining the strategic petroleum reserve to bring down the price at the pump, low Chinese economic activity, and high exports from Russia despite sanctions from the West.

As oil is a key input in most manufactured goods, the price per barrel is an important contributor to the outlook for inflation. As a result of lower oil revenues, OPEC (the Organisation of Petroleum Exporting Countries), decided to cut supply in order to support prices. These changes are expected to feed into markets in the coming months.

This in turn could prove troublesome in the Federal Reserve’s fight against inflation. Combine higher oil prices with higher global demand from developing nations, geopolitical division, and less production due to the transition to a lower carbon world in the West, and we may see long term inflation becoming sticker than anticipated, staying above the Fed’s pre pandemic inflation target of 2%.

Inflation is not the sole determinant of monetary policy and the Fed’s dual mandate also includes tackling unemployment. As outlined in our last commentary, jobs and unemployment data remains strong with wages continuing to rise. Wages are believed to be rising due to a labour shortage and demands for pay to reflect rising prices.

There are an estimated 10 million job openings in the US according to US Chamber of Commerce. With 6.1 million unemployed persons in the US, there are 1.6 jobs available per unemployed person. Naturally, this strength is expected to decline in a recessionary environment.

As mentioned previously, companies could look to keep workers on despite falling revenues in case they are unable to hire them back when the recessionary environment disappears. This would mean a potentially lower valuation for equity markets as revenues drop but costs remain higher than they otherwise would. It also indicates higher long-term inflation.

Along with a resistance from central banks to hold rates high, we do not have a typical recessionary response.

Our present view is that interest rates will remain high, but we are cautious about the lag effects of the rapid increase in such a short period of time. Interest rate hikes take time to seep into the economy, so time to assess the effect that the rate hikes have already had is needed. Tightening too much too quickly increases the risk of a recession, making interest rate decisions even more difficult.

As we have said before, we think the Fed will use a recession to bring inflation down. The real question will be how deep this recession will be.

According to a study by Blackrock on the last 12 recessions since 1978, from the moment that the US 2- and 10-year yield curve inverts, it takes an average of 18 months to reach the following recession. The US 2- and 10-year yield curve inverted 11 months ago in July 2022.

Further data from Blackrock identifies that the neutral interest rate (the rate at which there will be no effect on economic growth) is now below the current Fed interest rate. This implies any further rate rises will create economic damage.

The US 2-year Treasury Note is currently yielding 4.76%, up from 4.45% a month ago. The 10-year Treasury Note yield is at 3.73% compared to 3.69% a month ago. In this environment, short duration (shorter maturity bonds) looks more attractive because of the healthy yield and a greater potential for capital preservation. If and when interest rates are forecast to drop, the reverse applies – longer duration will be preferred as these bonds have greater interest rate sensitivity and so will experience a greater capital appreciation relative to shorter dated bonds.

Historically, stocks and bonds have had an inverse relationship – bond prices rise as stocks fall, mitigating the downside in equity drawdowns, and vice versa. This was not the case in 2022 as stocks and bonds sold off together, leading some investors to believe this to be the “new normal”. Although this may prove to be correct, as central banks will be reluctant to decrease interest rates, caution should always be applied when investors believe “this time will be different”.

Chart showing YTD performance of US equity indices

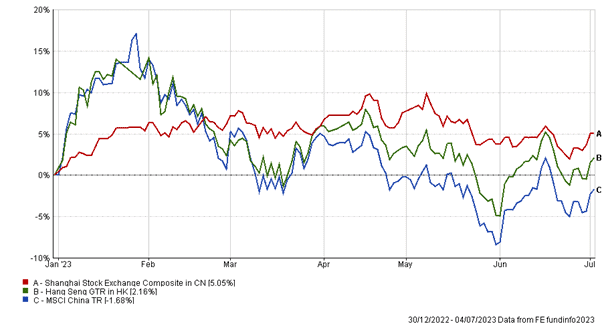

China

China’s long-awaited economic reopening continues to show weakness as the Hang Seng index and the Shanghai Stock Exchange struggle, well below their high-flying performance at the start of the year.

That said, the Hang Seng recovered well in June, up 3.23%, whilst the Shanghai Composite remained flat, gaining just 0.47%. China has been the engine room for global growth over the last 25 years, providing the global economy with cheap manufactured goods. For this reason, it is unlikely that we can see a sustained global bull market without China participating.

In an attempt to stimulate their domestic economy, the People’s Bank of China cut its prime lending rates by 1%. This reduction represents the first rate cut in over a year, bringing the 1-year rate to 3.55% and the 5-year rate to 4.20%. The 5-year lending rate is very important in supporting a struggling housing market because this is the rate which is typically used to price mortgages.

The Chinese property market makes up 25% of the country’s annual GDP, so it is vitally important the Chinese government do all they can to protect it. Lowering the borrowing rate may increase domestic demand and ease the burden on the huge debt levels property developers have when they refinance.

The property market faces a greater headwind in the form of a weakening currency (the Renminbi) against the US dollar. Chinese property companies hold a significant amount of offshore debt denominated in dollars – they are therefore hit twice, as their revenues are in Renminbi, which is weakening, and debt repayments are in dollars, which are strengthening.

One could argue that the effect on the Chinese economy will be balanced by exports to foreign buyers, which look more attractive when the Chinese currency is weaker. However, with exports down year on year, this may only soften the blow slightly.

For this reason, Goldman Sachs has reduced its GDP growth rate estimate for China from 6% to 5.4%. This is still above the Chinese Government target of 5% but certainly not at the levels investors have become used to over the past 20 years.

As we have noted on many previous occasions, geopolitical risk still remains when investing in China.

Chinese President Xi Jinping may however be less aggressive with his decisions after seeing the outcome for Russia in its invasion of Ukraine. China would be less able than Russia to deal with similar sanctions imposed by the West, given its reliance on actively participating in the global economy.

One major advantage the Chinese economy currently has over the majority of developed nations is persistently low inflation. The Chinese consumer price index rose just 0.2% in May compared to a year ago, with month-on-month deflation of 0.2%. This certainly gives the central bank room to decrease rates further, stimulating economic activity without the immediate risk of inflation.

Chinese government bonds have also benefitted from a looser monetary policy, but developed market debt is preferred due to its yield advantage. The current yield on the two-year Chinese government bond is 2.091%, compared to two-year US treasury debt which yields 4.909%.

Investor sentiment surrounding China has been very poor in recent months given the slow economic restart, giving markets plenty of room to run if data starts to turn positive. However, the long-term outlook is still somewhat bleak given the country’s aging demographics and the shift of global manufacturing to other developing (or even developed) nations.

YTD performance of Chinese stock market indices

Europe

In contrast to the UK, recent Eurozone inflation figures revealed that the area’s annual inflation rate fell by more than expected in June to 5.5%. This was below forecasts of 5.6% and down from the 6.1% inflation figure recorded in May. A reduction of 5.6% in the cost of energy during the month of May contributed the most to the decrease in inflation.

Despite a fall in the headline inflation figure, core CPI (which excludes volatile items like food and energy) increased by 5.4% – preventing any hope of relief for EU policy makers. This was driven by an acceleration in the cost of services in the region after Berlin reduced subsidies for public transport. The ECB interest rate currently sits at 3.5% but is widely expected to rise to 4% in September.

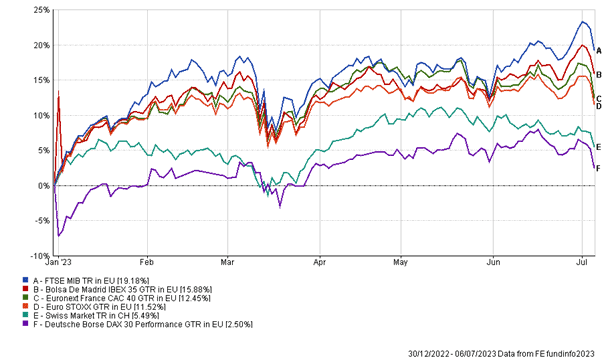

YTD performance of European equity indices

Nonetheless, European equities are having a strong 2023. This is clear from the chart above, with all 6 major European stock markets showing positive returns.

The FTSE MIB, the benchmark index for the Italian national stock exchange, has increased by almost 20% this year to date. France’s CAC 40 is up 14% year to date, powered by a rally in luxury goods companies. LVMH, Kering and Hermes have accounted for close to a third of the CAC 40’s gain, a stock market performance that ranks among the best in Europe. This recent growth has been heavily fuelled by optimism over the reopening of the Chinese economy, which is a major market for companies like LVMH.

European equities have benefited more broadly this year from cooling inflation, resilient economic activity and mild weather that averted a much-feared energy crisis.

Europe also has its fair share of technology companies, representing 7% of the European equity market. It cannot compete with the US in this respect, however, where technology companies comprise 30% stock market.

This makes it difficult for European equities to keep up with the US markets when growth stocks are performing well. In addition, the recent underwhelming economic data coming out of China could lead to reduced demand for European exports in the near term.

The most recent European inflation data led investors to adjust their expectations as to when the ECB’s tightening cycle might end. This caused the recent bond sell-off to continue, leading to higher yields – 2 year German bunds currently sit at 3.3%, which is up by 20% over the past month, while the yield on 10 year German bunds is lower 2.5%. Again, this inversion of the yield curve is often interpreted as a sign of approaching recession.

Robert Dougherty, Associate IFA

Ryan Carmedy, Graduate Trainee IFA

Harry Downing, Graduate Trainee IFA

July 2023

This article is not a recommendation to invest and should not be construed as advice. The value of an

investment can go down as well as up, and you may get less back than you invested.