Then to now…and beyond

In 1991/92, basic rate income tax – then at 25% – was the top rate of tax paid by 96.5% of UK adults. The remaining select 3.5% paid higher rate tax (at 40%, as it is now outside Scotland). Up until the end of the 2000s, the starting point for higher rate tax generally followed inflation. However, in that period earnings outpaced prices, with the result that there was a steady rise in the numbers dragged into higher rate tax.

Matters worsened in the 2010s, with both freezes in the higher rate threshold and the introduction of additional rate tax on incomes over £150,000. The freezes stopped after 2015/16, only to reappear in the 2021 Budget. The Chancellor at the time, Rishi Sunak, fixed the higher rate threshold (again outside Scotland) at £50,270 through to 5 April 2026. At the time inflation was not projected to rise to the dizzy heights of 2% until 2025, meaning the impact of the freeze was expected to be limited.

In March 2023, Mr Sunak’s next but two successor as Chancellor, Jeremy Hunt announced:

- a further two-year extension to the higher rate threshold freeze (outside Scotland), meaning it would run up to and including 2027/28; and

- a reduction in the threshold for additional rate tax (45% outside Scotland) from £150,000 to £125,140 (a move Scotland followed).

The result

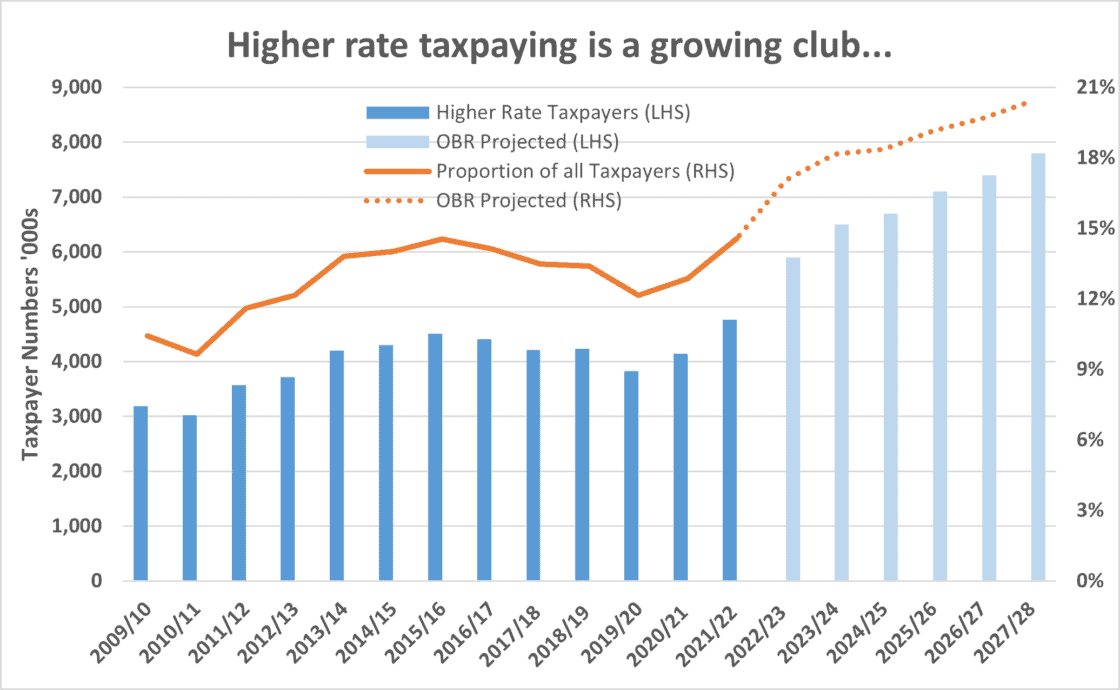

The IFS used data from the Office for Budget Responsibility (OBR) to calculate the impact of the Sunak and Hunt freezes combined with inflation at a level which was almost inconceivable just over two years ago. By April 2028, 14% of all adults and about one in five of all taxpayers will face a marginal rate of tax of 40% or more. The graph below shows the unhappy trend. In terms of tax increases, the IFS calculates that the threshold freezes will represent the single most significant tax increase since the rate of VAT was raised from 8% to 15% in 1979.

That only one number has changed – the additional rate threshold – makes the size of this tax increase difficult to believe…until you remember inflation. In effect, the Treasury has delegated tax policy to the soaring Consumer Prices Index (CPI).

Sources: HMRC, OBR

What can you do?

If you pay tax at more than basic rate already, or are likely to in the next five years, there are a range of factors to discuss with your financial adviser:

- What is your marginal rate of tax – the tax you pay on the next £1 of income? It may not be either of the ‘advertised’ rates of 40% (42% in Scotland, 33.75% on dividends) or 45% (47% in Scotland, 39.35% on dividends). The labyrinthine structure of the UK tax system with tapered allowances and cliff edge eligibility thresholds can create much higher marginal tax rates. For example, if your income is between £100,000 and £125,140 your marginal tax rate could well be as high as 60% (63% in Scotland).

- Are your investments held in the optimum framework, given your marginal tax rate? You may have been dragged into a higher tax band because of the threshold freezes, in which case the way you hold your investments may need to be revised. Remember too that the dividend allowance has been halved to £1,000 this tax year and will halve again in 2024/25. You could soon be a dividend taxpayer, if you are not already.

- Can you take advantage of independent taxation? Married couples and civil partners are taxed individually, so it might make sense to transfer investments if you each have different marginal tax rates.

- Can you restructure your income? For instance, if you are a private company director you may be able to choose between dividends and salary and save tax.

- Are you making the most of the tax reliefs available on pensions and venture capital investments? The rules in both areas changed (yet again) in 2023/24, creating some new opportunities.

Action

It is still relatively early in the tax year, so there is time to take action that can have an impact on your 2023/24 tax bill. But the longer you delay, the more you will experience the chill of threshold freezes.

Call us today to arrange for an income tax planning review.

From 0.2% to 11.1% in 26 months

A couple of years ago, inflation appeared to be a dragon that had been well and truly slain. Bar a few hiccups, the Bank of England had succeeded in meeting its remit to keep inflation, as measured by the CPI, at 2%. For example, between December 2009 and December 2019, CPI averaged 2.1% and only once briefly exceeded 5%. This decade started with pandemic-driven concerns about deflation – falling prices. As recently as August 2020, annual CPI inflation reached a low of 0.2%.

The picture began to change in the following year, although even as recently as July 2021 inflation was spot on the Bank’s target at 2.0%. However, by December 2021 it had risen to 5.4%, a figure which was regarded as ‘transitory’ by many economists. As we now know, they were wrong.

Where are we now?

Inflation now looks as if it peaked at 11.1% in October 2022. It was still 10.1% in March 2023, but in April it dropped to 8.7%. The drop was not a surprise – in fact the consensus had been for a larger fall to 8.2%. The decline is currently expected to continue for the remainder of 2023, before slowing in 2024.

April’s sharp fall is a quirk of the way inflation is measured. For example, March 2023 inflation is the increase in prices between March 2022 and March 2023 and April 2023 inflation is similarly the increase in prices between April 2022 and April 2023. That means the difference between March 2023 annual inflation and April 2023 annual inflation is accounted for by only two months:

- Inflation between March 2022 and April 2022, which drops out of the annual comparison; and

- Inflation between March 2023 and April 2023, which enters the annual comparison.

Between March and April last year, utility prices jumped as the Ofgem cap rose by 54.3%. In 2023 there was only a minimal change in utility prices, thanks to the Government energy price guarantee. Thus, April 2023’s annual inflation had a built-in fall. The same step down will happen again, albeit to a lesser degree, in July and October as new Ofgem price caps replace last year’s limits.

So, can we forget inflation again?

The answer is no. Even before April’s disappointing inflation numbers, the Bank of England did not see inflation reaching its 2.0% goal until early in 2025 – it estimated 2023 inflation would end at around 5%. That would be just enough to allow the Prime Minister to meet the pledge he made in early January to halve inflation in 2023, which relied heavily on that utility price mathematics. Falling inflation is good news, but:

- It does not mean that overall prices are falling. Some prices may drop year-on-year – energy costs being the classic example – but, more broadly, price increases will continue, albeit at a slower rate. Think of the impact of overall inflation as a ratchet: what goes up normally stays up. Periods of falling overall prices – deflation – are rare and not good news for the economy.

- The impact of previous inflation does not disappear. Based on April 2023’s CPI, the January 2020 £1 now has a purchasing power of 83.36p. Had inflation been at the Bank’s 2.0% target, the figure would be 93.77p.

Those two facts are directly relevant to your personal financial plans. A corollary of the falling value of money is that your January 2020 level of life cover, income protection, pension contributions and savings need to be a fifth higher just to stand still in purchasing power terms. No fall in the future rate of inflation will change that fact – unless inflation turns negative.

Action

Price inflation has outpaced earnings in recent years and tax allowances and bands have been frozen, meaning the buying power of your net income has probably dropped even faster. In such circumstances, there may be difficult choices about which parts of your financial planning to update.

Call us today to discuss your options and priorities in making inflationary adjustments to your financial plans.

Rethinking retirement plans

The March 2023 Budget contained two announcements which could alter your retirement planning strategy. The first, an increase in the annual allowance, was not a great surprise, as the Chancellor had been under growing pressure to alleviate pension tax issues for NHS consultants. The second, a two-stage abolition of the lifetime allowance, was totally unexpected.

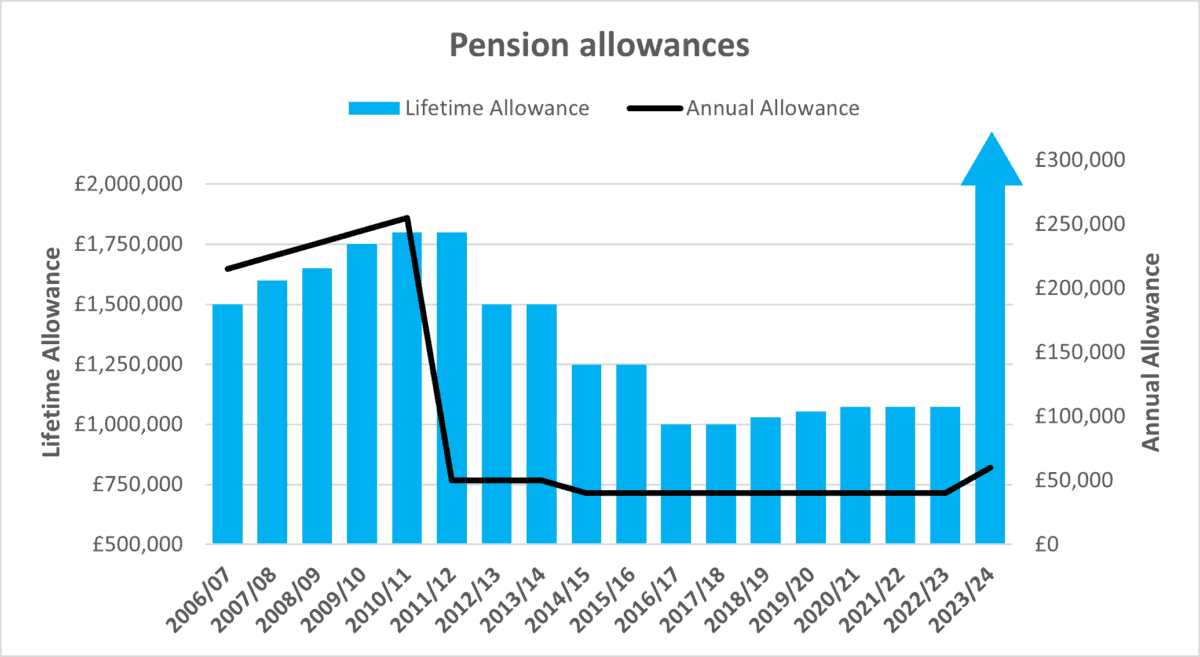

Source: HMRC

The annual allowance increase

Broadly speaking, the annual allowance sets the maximum tax-efficient total contributions during a single tax year to all your pension arrangements from all sources. As the graph demonstrates, it was sharply cut in 2011/12 and cut again three years later. The 2023 Spring Budget raised the maximum annual allowance from £40,000 to £60,000 from 6 April 2023. However, the important word to note here is ‘maximum’, as the complex rules that taper the annual allowance for high earners remain in place, albeit the minimum tapered annual allowance also increased, from £4,000 to £10,000.

A £6,000 increase to £10,000 also applies to the money purchase annual allowance, which restricts your contributions if you have used the pension flexibility rules to draw a taxable benefit.

The lifetime allowance changes

The lifetime allowance was a parallel limit to the annual allowance, setting the maximum tax-efficient value of all pension benefits. It too suffered cuts and freezes from 2011, although each cut was accompanied by transitional protections, complicating the pension tax regime further. While there had been calls for the lifetime allowance to be scrapped because the annual allowance was arguably a sufficient restriction, nobody expected such logic to prevail. When it did, it appears to have surprised even the Treasury.

The proof of that emerged in the various explanations of the changes which the Treasury produced in the weeks after the Budget. What appeared on Budget Day to be an outright abolition on 6 April 2023, later proved to be:

- The lifetime allowance remains in the pension legislation for the time being, but

- For 2023/24 there is a reduction in the rate of the lifetime allowance tax charge to 0% from the previous 55% for lump sums and 25% where funds were used for income. However,

- For certain lump sums, the lifetime allowance charge has been temporarily replaced with an income tax charge before

- Full abolition takes effect from 6 April 2024. It is not clear whether this will be achieved by next year’s Finance Act or later legislation.

The need for review

In theory, the Budget changes could mean that a handful of higher earners who had long given up on paying into a pension could arrange pension contributions of £180,000 in 2023/24, taking advantage of the carry forward rules for three previous tax years of unused allowances.

In practice, how much you can benefit from the allowance changes is dependent on your individual circumstances and retirement goals. There will be situations where it makes no sense to revise your pension strategy, particularly as the Shadow Chancellor, Rachel Reeves, has said the lifetime allowance would be reintroduced if the Labour Party wins the next election. On the other hand, this may be the golden opportunity to boost your pension pot before the gates slam shut again.

Action

Navigating changes – and potential changes – in pension tax law requires expert advice. It can also take considerable time, given the data that may be required from a range of pension providers.

If you want to explore the impact of the Budget changes on your retirement planning, contact us as soon as possible so that the process can begin.

State Pension Age – still no clarity

If the lifetime allowance reform was a surprise inclusion in the Budget, an announcement on when State Pension Age (SPA) would rise to 68 was an unexpected absence.

2037 or 2044?

The Government had been required by law to publish its latest SPA review by early May. As SPA changes have a significant effect on Government finances, it was thought that Jeremy Hunt would confirm that an SPA of 68 would be phased in between 2037 and 2039. However, the Budget passed with no mention.

Just over a fortnight later, the DWP published its ‘State Pension Age Review 2023’. Simultaneously, the Secretary of State announced that the final decision on the introduction of a SPA 68 would only be taken after yet another review. The timing of that assessment is to be ‘within two years of the next Parliament’, conveniently making the resolution a post-election issue. In the meantime, the existing legislation, which starts the SPA 68 phasing in from 2044, stays in force.

SPA changes have been a hot potato in previous elections, so the sidestep is politically understandable, if not helpful for anyone planning retirement in the next few years. The Government has said it will give at least ten years’ notice of a change to SPA. This latest decision deferral just about leaves sufficient time for 2037 to still be selected as the start date.

Action

The DWP’s March 2023 announcement is a further reminder that relying on the State for your retirement income has its risks.

If you are planning to retire before your SPA – whatever that might be – make sure your plans provide cover for the income gap until you reach the magic (ever-increasing) age.

31 July deadline extended

In March, the DWP and HMRC learned a lesson that you might have thought both bodies would be very familiar with: hard deadlines create last minute surges.

State Pensions and National Insurance contributions, take three

The original deadline, 5 April 2023, had been known about for many years – it was set as part of the transition to the New State Pension regime introduced in 2016. Two aspects of that were worse than its predecessor:

- The minimum National Insurance Contributions (NICs) record (including any credits) to receive any State Pension increased from one year to ten; and

- The NICs record for a full pension was raised by five years, to 35 years.

To help people with patchy NICs records, the rules for filling up gaps with voluntary NICs were temporarily relaxed, allowing contribution catch-up to go back as far as 2006/07 rather than just the previous six tax years. That was all meant to end on 5 April 2023, after which catch-up would stop at 2017/18.

As the deadline neared, its significance for some people became more apparent thanks to a snowballing press coverage. Stories that rightly – if extremely – suggested one year’s voluntary NICs (£824.20) could mean £58.24 a week of pension drove the flood of enquiries to HMRC and the DWP. Eventually, on 7 March, the tsunami prompted a deadline extension to 31 July 2023. However, on 12 June 2023, the Government announced a further extension. People will now have until 5 April 2025 to fill gaps in their NICs record from April 2006.

Action

If you have gaps in your NICs record from 2006/07, you may be able to boost your State Pension – even if you have already retired – by paying voluntary NICs. But it is not automatically the case you will gain.

Talk to us if you have – or think you have – gaps in your NICs record since April 2006.

Past performance is not a reliable guide to the future. The value of investments and the income from them can go down as well as up. The value of tax reliefs depend upon individual circumstances and tax rules may change. The FCA does not regulate taxor benefit advice. This newsletter is provided strictly for general consideration only and is based on our understanding current law and HM Revenue & Customs practice as at 12 June 2023 and the contents of the Finance (No 2) Bill 2022-23. No action must be taken or refrained from based on its contents alone. Accordingly, no responsibility can be assumed for any loss occasioned in connection with the content hereof and any such action or inaction. Professional advice is necessary for every case.

This article is not a recommendation to invest and should not be construed as advice. The value of an investment can go down as well as up, and you may get less back than you invested.