Markets continued to be bombarded with a flurry of headlines this month, and while most generally trended downwards, the consensus was that markets have been in a “holding pattern” awaiting the much anticipated 2nd April ‘Liberation Day’ (or Demolition Day according to one economist).

Uncertainty over tariff policy has clouded how much risk needs to be priced into markets. Soft economic data in the US showed a gloomy outlook with consumer and business confidence continuing to drop. On the other hand the hard economic data (the unemployment rate, manufacturing output etc) continued to show a strong economy. Fund managers increased their probability of the US entering a recession this year, but as US policy is still uncertain this could quickly change.

The biggest risk is whether the worrying US soft data is a self-fulfilling prophecy – worried consumers cut back their spending, causing a recession.

Trump announced a flat 10% tariff on all goods imported into the US, with higher tariffs on companies deemed to be the worst actors. Markets reacted badly to this news with large downturns in global equities and falling yields on government bonds. Treasury Secretary Scott Bessent has said this is a ceiling, not a floor and Trump said if other countries reduce their tariffs, the US will bring its down. So there is certainly room for negotiation, which is the best case scenario.

Trump will now start work on his ‘big beautiful bill’, that is his planned tax cuts and reregulation. While tariffs may impact demand, prices and earnings in a negative way, this bill should have a positive effect.

A complicating factor is in how different companies will be affected by tariffs. For example, the 25% tariff on automobiles being imported into the US may well damage the earnings of non-domestic US car manufacturers importing into the US, where as a company like Tesla, which builds 100% of its cars in the US, may fare better. The 1964 ‘chicken tax’ is a good example of how tariffs in practice may not have their intended consequence.

Despite countries looking to be more protectionist, the theme of this month is very much interconnectedness.

We have seen this in more obvious places such as massive proposed German defence and infrastructure spending on the back of evolving US foreign policies, but also in a less thought of area such as Gold.

With Gold prices continuing to drive higher as investors park their capital in the non-yielding safe haven asset, an unintended consequence of this has been the impact of Cocoa production in countries such as Ghana (as reported in the FT early March). Illegal gold mining in Ghana to take advantage of these high prices has destroyed farmland, leading to difficulty in farming the much-loved commodity.

The butterfly effect – small changes in the initial state of a system, leading to significant and unpredictable outcomes – is certainty what we are seeing with Mr Trump’s change in US policy. The problem is markets cannot see what these different outcomes are and this has created the high uncertainty we have seen. Once again we reiterate how important diversification is.

German 10 year Bund yields rose on the news of the massive fiscal spending package in the region, not because investors think the spending is too much, but rather they expect future growth and inflation to pick up. Defence companies’ valuations shot up and smaller and mid-sized companies values also rose. Bringing this potential back down has been the retaliatory tariffs imposed by Mr Trump.

While this has been positive for the German market, the knock-on effects of this have been other Euro-area bond yields have picked up. French OATS and Italian bond yields also rose, and as these countries are in much more difficultly debt-wise, this could cause further complications.

Meanwhile the Federal Reserve held interest rates and cut its expectation for US growth while increasing the expected level of inflation for the year. Markets had anticipated this, with the Fed Chair Jerome Powell conveying a very calm tone to reassure markets.

The Fed has arguably the most difficult job in the world right now, sifting through the noise to find the signals, and tariffs are creating a lot of noise. The Fed has a dual mandate of achieving maximum employment and price stability. The price stability side of the mandate has the most upside risk and therefore rates are likely to remain as they are, with potentially one cut now priced in for the rest of the year.

As Powell said, it is the net effect of tariffs, tax cuts and deregulation that matters. All focus has been on the former and not the latter, making policy decisions very difficult. Investors should remind themselves of this and remain focused on the long-term.

Closer to home the UK market was fairly quiet this month, with major indices slightly down on the month as uncertainty and tariff threats weigh on the stock market as well. Rachel Reeves announced her March budget which contained very little information that markets had not already priced in.

We saw difficulties in Emerging Markets, predominantly in Turkey where President Erdogan‘s arrest of his main political rival puts the country’s democracy in doubt. We explain the investment implications of this later in the article.

Areas of focus

Technology companies have seen some of the biggest drops in value, initially due to investors taking profits from the best performing companies. The long-term outlook for the sector is still very positive and the potential for development is massive. Although the recent CoreWeave IPO in the US has rattled investors (partly due to company specific issues), we remain positive on the sector long term.

Gold prices continue to rise, pushing past $3,100 per troy ounce.

Automobile manufacturers face huge pressure amid 25% import tariffs.

European longer term bond yields rose, steeping the yield curve as growth in the region is expected to pick up (although high tariffs from the US will negate this positive effect).

US high yield bond spreads have widened by 39% since the start of year as investors price in greater risk to lower quality companies.

Value stocks and strong dividend payers have shielded investors from some of the volatility this year relative to their growth counterparts. Over the past month the Russell 1000 Value dropped 6% while the Russell 1000 growth dropped 17% (hedged back to GBP).

Although most stocks have fallen in value recently, we expect the providers of Veblen goods (see our new bi-weekly investment terms article for more information) such as Ferrari and LVMH to fare better amid higher tariffs.

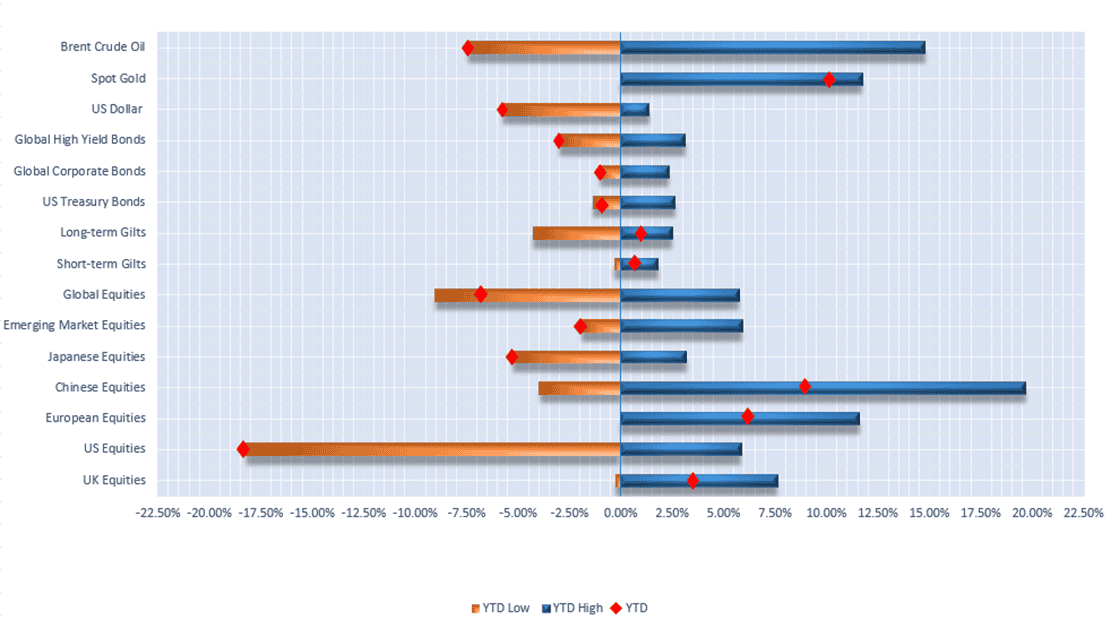

Selection of assets 2025 YTD returns and range of returns as at 04/04/2025 (the two ends of the bars represent the range of YTD returns and the red dots represent the current YTD return). Indexes used: FTSE All-Share, Russell 2000, STOXX Europe 600, MSCI China, MSCI Japan, MSCI Emerging Markets, FTSE UK Conventional Up To 5 Years, FTSE UK Conventional Over 15 Years, ICE BOFA US Treasury, ICE BOFA Global High Yield, ICE BOFA Global Corporate, US Dollar Index, S&P GSCI Gold Spot, S&P GSCI Brent Crude Spot. Returns hedged back to GBP with exception of US Dollar which is in US Dollar terms. Data from FE Analytics and MarketWatch

US

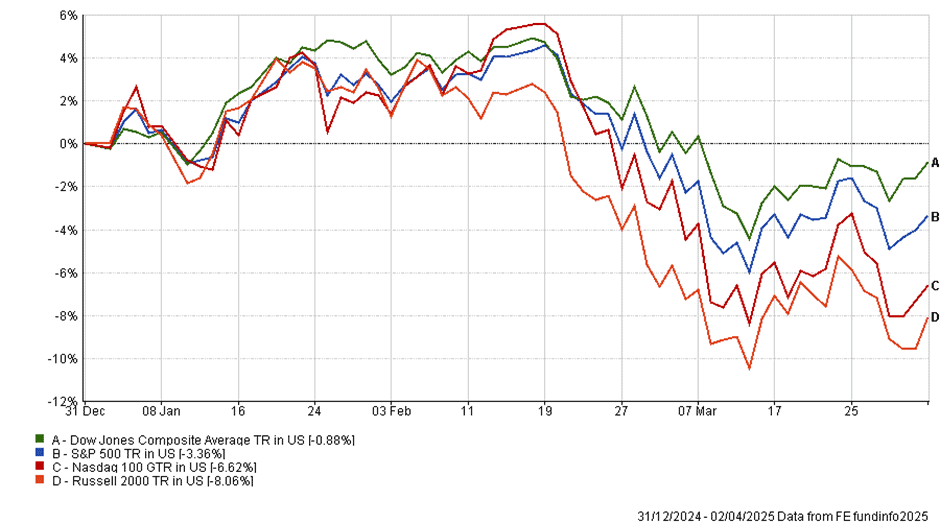

YTD performance of US equity indices (Source – FE Analytics)

US equity markets experienced a broad downturn in the month of March as major indices had their most significant monthly declines since late 2022.

Unsurprisingly the major catalyst for this was the markets’ anxiety surrounding Trump’s tariff policy and the announcements on “Liberation Day” on 2nd April. The announcement included sweeping reciprocal import tariffs for essentially the entire world, and we will delve more deeply into this later in this article. Investors fear that this could be the start of a global trade slowdown and perhaps higher prices, as companies pass the added costs through to consumers.

Technically, the Russell 2000 has entered a “bear market” as peak to trough declines are now just over 20%. The S&P 500 and Nasdaq 100 are in the “correction” phase with declines of over 10%, whereas the Dow Jones Composite Average remains resilient as it flirts with the 10% decline threshold.

The Dow comprises 30 “blue chip” large companies, suggesting that investors favour companies that are more value-oriented in times of uncertainty as opposed to those with high valuations to grow into.

Nvidia has been particularly affected by the ongoing trade talks as its business model is very much reliant on global free trade. As always, there are always pockets of outperformance in all market conditions, with the energy and utilities sectors managing to post positive returns in the month. Such performance cannot be captured with market capitalisation weighted indices and therefore active management is required.

In terms of economic data through the month of March, readings were very mixed but overall weaker. Of course, the latest trade policies will not feed through to be reflected in the data for at least a few months. Firstly, CPI for February (reported in March) came in at an increase of 2.8%, down from January’s 3.0% print and slightly below analysts’ 2.9% expectations.

The unemployment rate ticked up 10 basis points to 4.2% for March with 228,000 jobs added, much stronger than the 151,000 added in February. Manufacturing and services PMI fell to 49.00 and 50.80 from 50.30 and 53.50, respectively. These two indicators both suggest that the US economy is starting to slow. Some economists have also now changed their GDP forecasts to show decline in 2025, with Goldman Sachs now placing the probability of a recession at 35%.

| 4th March 2025 | 4th April 2025 | Change | |

| US 2 Year Yield | 4.01% | 3.64% | -0.37% |

| US 10 Year Yield | 4.25% | 3.95% | -0.30% |

| Dollar Index | 105.74 | 102.45 | -3.29 |

YTD changing in US bond yields and the US dollar index (Source – MarketWatch)

Not all US investors were upset with the recent equity market sell off – bond market investors welcomed it. The yields on both the two- and ten-year Treasuries (US government debt) dropped to reflect the lower growth prospects for the US economy and a flight to safety.

After the painful experience in 2022, where bond and equity markets fell simultaneously, many investors assumed that the historic negative correlation was over. However, the past few months has proven otherwise, highlighting the importance of diversification across asset classes. The dollar index also declined further and as mentioned in last month’s commentary, this is what the Trump administration is aiming for and will help prices of risk assets going forward.

The Fed’s independence and adherence to the dual mandate only will be tested if markets continue to decline. Many market commentators have already called for the Fed to ease financial conditions in future meetings, citing that lower rates could guide the US out of a looming recession and a negative year for equity returns. The CME FedWatch tool now puts a 92.4% probability of an ease coming in June with rates being 1% lower by year end than they are now. Current Fed rhetoric indicates that they will be cognisant of not undoing their hard work getting inflation down with the potential of tariffs reigniting inflation.

With all this negative sentiment, it is important to take a step back and look at the bigger picture. As Warren Buffett’s mentor, Benjamin Graham, once said, “In the short run, the stock market is a voting machine. But in the long run, it is a weighing machine.” This rings true today; markets may be driven by headlines currently, but over the longer term they are driven by corporate earnings. Bullish factors, such as AI and the prospect of lower interest rates, have not gone away and the intelligent investor is seeing this sell off as a great opportunity to buy their favourite company on sale.

Tariffs

It may be useful to understand the fundamentals and purposes of tariffs as a trade policy tool. At its core, a tariff is simply a tax imposed on the value of a good or service being brought into the country. The purpose is to increase the cost of importing the good, making goods manufactured domestically relatively more attractive. The tax itself is typically paid by the importer; however in reality, it is shared between the importer, the exporter, and the final consumer.

Historically, tariffs have been used a significant source of government revenue but this has diminished with the advent of other forms of taxation. The rise of globalisation also put pressure on governments to reduce restrictions in favour of free trade. More recently, they have been used as a bargaining chip to negotiate other related issues for the Trump administration.

Since Trump’s inauguration, many countries (and sectors) have felt the wrath of his tariffs. Most notably, Canada, Mexico, China, and the auto industry. However, policy changes have come so frequently, often via an overnight tweet, that it would have been counterproductive to take note until a concrete plan is in place. In comes, “Liberation Day”.

“Liberation Day” set out a two-tiered tariff structure. First, a baseline 10% tariff will be imposed on virtually all good entering the United States (including from the Heard and McDonald Islands, which has no human inhabitants and is occupied by mostly penguins…). The second tier consists of higher “reciprocal tariffs” on imports from approximately 60 countries. These higher rates have been calculated based on Trump’s assessment on the trade barriers that these countries apply to the United States. The only real exception applies to Canada and Mexico where the US will honour the US-Mexico-Canada Agreement (USMCA). The 25% tariff on automobiles will also continue to apply.

Going forward, we will be watching how countries will retaliate. At the time of writing, China has already come back with a 34% retaliation tariff. Further news-driven downside could be prompted if other countries follow suit.

Looking longer term, the consensus outcome is an increase to inflation as producers push the higher inputs costs onto the price of the good for end consumers, which is quite probable.

However, the other side of the coin could be that global trade slows, lowering aggregate demand and actually pushing prices lower. The first outcome would tie the Fed’s hands, meaning they will be unable to reduce interest rates. The second outcome would give the Fed even more reason to cut rates. In our view, the best case scenario here is that exporters pay the tax, reducing US government debt, and more goods are produced and consumed domestically, boosting GDP growth. At this stage, it is too early to tell but needless to say, it is something that we will be watching very closely.

UK

Last month, Chancellor Rachel Reeves’ Spring Statement outlined a series of fiscal policies aimed at steadying the UK economy amid global uncertainties.

During the statement, it was highlighted that the Office for Budget Responsibility (OBR) halved the UK’s growth forecast down to 1% for 2025. The OBR also expects inflation hitting 3.2%, before falling to 2.1% next year (although this did not take into account any tariff effects).

Based on the OBR’s forecasts, the Chancellor also highlighted the government’s aim to transition from a £36.1 billion deficit in 2025-26 to a £6 billion surplus by 2027-28.

Welfare reforms were the most significant announcement, projected to cut £4.8 billion in spending by 2029-30, particularly affecting PIP and Universal Credit payments. The government also reiterated plans to increase revenue through freezing income tax thresholds.

Meanwhile, an extra £2.2 billion has been allocated to defence, with spending expected to reach 2.5% of GDP by 2027. The hope is that this will stimulate the otherwise lacklustre economic growth outlook.

In housing and infrastructure, a commitment was made to build 1.3m new homes over the next five years, targeting 305,000 homes annually by the end of the decade.

Coming in just a week after Reeves’ Spring Statement, Trump’s ‘Liberation Day’ announcements mean that the UK will be subject to the baseline 10% tariff on all exports to the United States from Saturday.

The UK exported £59.3 billion worth of goods to the US last year, most of which will now face at least a 10% tariff.

According to the Institute for Public Policy Research think tank, UK car manufacturers such as Jaguar Land Rover could be the most exposed to their US tariffs, which are 25% for companies in this industry. It is thought that 25,000 jobs in the industry could be at risk as, currently, one in eight UK built cars are exported to the US.

The UK pharmaceutical industry is also heavily reliant on trade with the US. For example, the US comprises 40% of AstraZeneca’s sales and 50% of GSK’s sales. In both companies, raw ingredients for their medicines often travel between the US, UK and Europe several times before being developed. These materials could face multiple tariffs as they cross borders.

While tariffs have clear negative effects to certain sectors within the UK, they may make others more competitive internationally. With the UK subject to the baseline tariff of 10%, UK exports will now be relatively cheaper for UK consumers when compared with other nations facing higher tariffs such as China.

In addition, the UK is the second largest exporter of services globally. This means that US tariffs (focused on goods rather than services) are likely to have a lesser impact than they will on other nations.

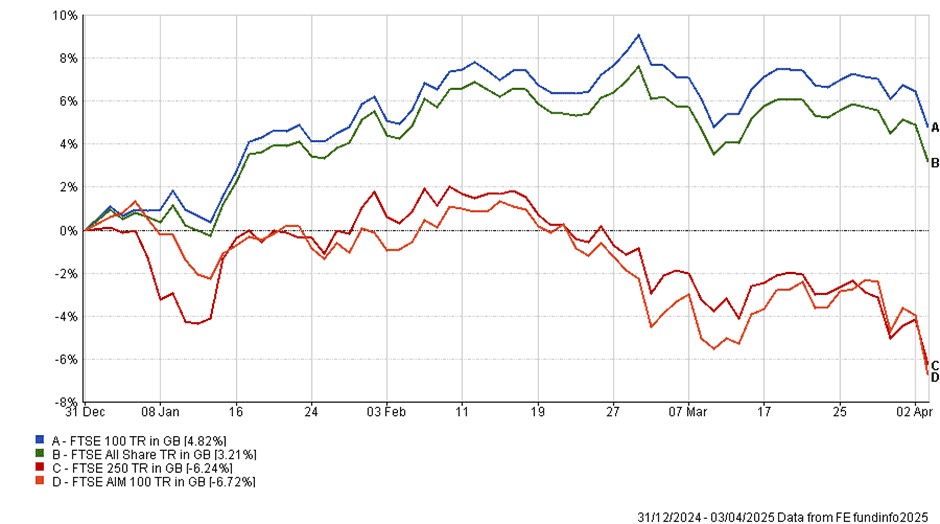

YTD performance of major UK stock market indices (Source – FE Analytics)

As investors sought to diversify portfolios away from the US into more defensive stocks, large cap UK equities have been quietly outperforming YTD. In part, this is because the FTSE 100 offers exposure to global companies in more “traditional” industries such as banking and energy.

On the news of the tariffs, the FTSE 100 declined 1.3%, reflecting the potential impact on the regions key industries. Smaller company stocks (which tend to be more dependent on the prospects for the UK domestic economy) fared worse, with the FTSE 250 index suffering a 2.1% drop, its largest singe day decline since August last year.

The recent turbulence in markets has caused gilt yields to fall, as investors seek safety in government bonds.

| Yield as at 04/04/2025 | YTD change | |

| 2Y Gilt | 3.95% | -9.78% |

| 10Y Gilt | 4.44% | -2.89% |

UK bond yields and YTD change as at 04/04/2025

As shown above, 2-year gilt yields have decreased almost 10% year-to-date whilst longer dated bonds are down just under 3% over the same period, reflecting heightened inflation expectations over the longer term.

Emerging Markets

This month saw considerable volatility in a number individual emerging markets, which we cover in more detail below.

China

Since the start of the year, there has been a renewed sense of investor confidence in Chinese equities, especially in the technology sector. In response, the Hang Seng technology index has increased by 30% YTD. US tariffs on Chinese exports have created some volatility in Chinese markets over the past week, and this is set to continue as the trade war intensifies.

In response to liberation day, China has stated that it will impose a reciprocal blanket tariff of 34% on all imports from the US from 10th April, escalating a global trade war between the two largest economies.

This was accompanied by typically strong rhetoric: “This practice of the US is not in line with international trade rules, seriously undermines China’s legitimate rights and interests, and is a typical unilateral bullying practice” China’s State Council Tariff Commission said while announcing the tariffs.

Turkey

In March, Istanbul’s mayor Ekrem İmamoğlu was arrested on charges of bribery and abuse of office. Prior to his arrest, he had been expected to announce his candidacy for Turkey’s 2028 Presidential Election. In response, huge protests arose in the region, as many Turkish people perceived the arrest as politically motivated.

Markets also responded quickly, with the Turkish Lira plunging over 12% against the dollar to record lows. The Borsa Istanbul (BIST) 100, Turkey’s main equity index, fell 16% with banks suffering the most. Turkey’s 10-year government bond also jumped more than 4% to almost 31%.

In response, the central bank sold around $25bn of foreign currency and increased its overnight lending rate to 46% to prevent further declines in the currency.

This political uncertainty has triggered market volatility and cast doubt on Turkey’s economic stability. The increased uncertainty may lead to a higher risk premium, making borrowing more expensive and discouraging foreign investment in the region. As a result, Turkey’s economic recovery could face further challenges and investors should remain cautious of further political developments.

Indonesia

Indonesia’s stock market has experienced significant volatility over the past month due to both domestic policy shifts and external economic pressures.

The Jakarta Composite Index (the primary index for the Indonesia Stock Exchange) ceased trading on March 18th after a 5% decline.

Several factors contributed to the decline. Internally, President Prabowo Subianto’s policies, including substantial public spending initiatives like a $28 billion free meals program, raised questions about the country’s fiscal stability. Externally, the risk of US tariffs heightened fears over the country’s export led economy.

Brazil

Like the UK, Brazil faces a 10% tariff on goods exported to the US. Due to shifting trade dynamics, economists suggest that Brazil’s baseline tariff could be positive for the region – making various sectors more competitive than those in regions with higher US tariffs.

As an example, during Trump’s first term in office and the China/US trade war of 2018-2020, demand for commodities such as soybeans and corn shifted from the US to Brazil.

As a result, the country’s stock index has experienced a gain of 9.07% year-to-date and the Brazilian real appreciated against the dollar.

Europe

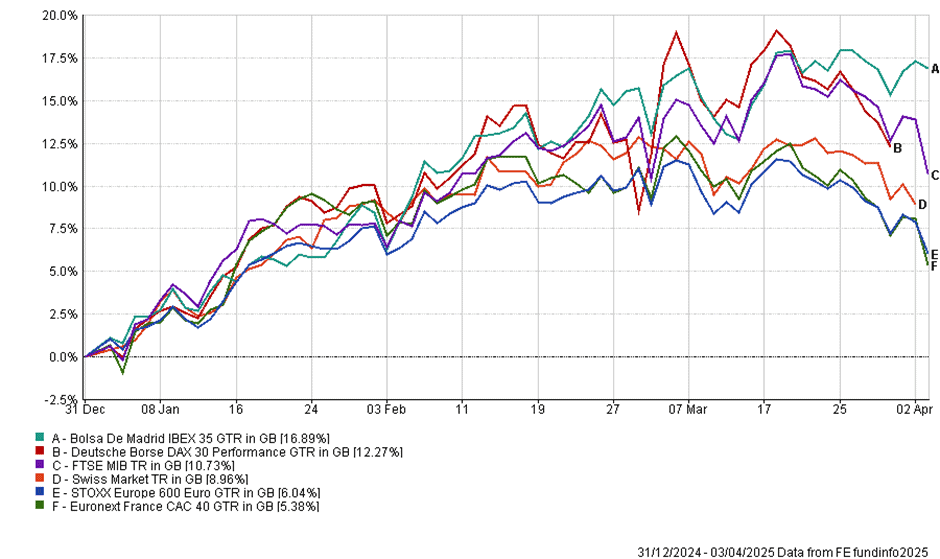

The Eurozone has had a positive first quarter of 2025. The STOXX 600 (an index of Eurozone equities) has demonstrated remarkable performance in the last few months, outperforming many of its global rivals, including the S&P500.

YTD performance of major European stock market indices, hedged to GBP (Source – FE Analytics)

Despite a 4.82% fall in March, it has achieved an overall year-to-date (YTD) gain of just over 6%. It remains to be seen whether this is simply the result of a US equity sell off given the uncertainty and unpredictability of the US equity and economic environment, or whether this marks a more persistent shift, given the improving macroeconomic conditions and relaxing of stringent fiscal, monetary and regulatory policies.

Inflation in Europe (HICP) fell from 2.3% in February to 2.2% percent in March, with annual inflation resting just above the ECB’s 2% target, which suggests the European Central Bank may be able to resume further interest rate cuts in April.

The ECB is likely to remain cautious in its approach given the potentially inflationary impact of Trump’s tariff fallout, as well as the risk of a broader global trade war which has the potential to affect all countries concerned. In addition, the ECB is also likely to be wary of increased spending on infrastructure and defence across the EU, in Germany in particular, which whilst a positive for the bloc, could also contribute to inflation.

Recent stock market outperformance in Europe could be attributed to a shifting global dynamic driven by changes made by the US administration. Whilst the consensus is that US equities are very likely to recover in the long term, tariff threats, political uncertainty, and a protectionist approach have damaged US equities in the short term – meanwhile, European equities have benefited from a more collaborative approach to trade and defence.

Combined with the resolution of some of the political uncertainty in France (at least until the recent arrest of Marine Le Pen) and Germany at the start of the year, the EU’s new plans for collective defence purchasing and the relaxation of specific regulatory policies could support a more optimistic view of economic growth in Europe in coming years.

In particular, Germany has been of interest so far this year – starting from a position of instability following the collapse of the coalition government last November, to undergoing large-scale economic reforms and the promise of new infrastructure and defence spending.

These changes are likely to benefit growth and this has been reflected in the DAX 40 (an index of the country’s 40 largest companies) which has risen by over 10% since the start of the year.

However, this surge in spending will affect holders of government debt, with the ten-year Bund yields increasing to almost 3 percent in March. This will impact borrowing costs throughout Europe due to the role that German debt plays as a benchmark, which may cause issues for more heavily indebted countries. While higher yields result in decreasing bond prices, they may eventually attract both domestic and foreign capital into the region in the longer term and reflect an expectation for greater growth in the future.

Another obstacle to long-term European optimism is US trade tariffs. Investors won’t have to wait any longer to see how the European stock market responds to the realisation of US tariffs, including a 20% blanket tariff on European goods and services.

One immediate effect was felt by the luxury goods sector, which depends on the US for 30% of sales, and predictably there was an immediate drop in stocks such as LVMH (-6%), Pandora (-14%) and Kering (-11%). Other sectors thought to be most affected include industrials and healthcare.

Fixed and permanent 20% tariffs would potentially have a significant impact on European stocks, although Trump has indicated that a reprieve may be possible through negotiation. However, the immediate short-term impact is largely inevitable, with tariffs starting on 5th April.

The European Commission’s Ursula von der Leyen has indicated the EU’s willingness to negotiate, whilst warning of a “strong plan to retaliate” should negations fail. A potential measure could include targeting the EU’s surplus in service exports to the US, which could significantly impact major US-based tech firms in their European operations. The path to resolution of these trade tensions remains unclear, but Europe’s response will be pivotal to maintaining the recent uptick in investor optimism for Eurozone equities.

Europe’s economic recovery, strategic policy shifts and a more supportive ECB stance, offers a promising outlook for European equities in the medium term. However, it remains unclear how European equities will fare once the new policy changes in the US take full effect and US equities recover. The exchange of tariff measures between the EU and the US will likely be reflected in the equity markets leading to significant short-term volatility as negotiations progress or tensions escalate. The coming months will be essential in determining whether the Eurozone’s current positive momentum can be sustained.

Robert Dougherty, Investment Specialist

Ryan Carmedy, Associate IFA

Harry Downing, Associate IFA

Fiona Chegwidden, Graduate Trainee IFA

April 2025

This article is not a recommendation to invest and should not be construed as advice. The value of an investment can go down as well as up, and you may get less back than you invested.