Investors are expressing concern over Trump’s plans to cut government spending while reducing taxes and delivering 3% real growth in GDP. Taken together, it will be very improbable he will achieve these goals all together and focus will be on his first few days in office next month to gauge the impact he will have.

US equity markets continued to move higher despite these concerns, with investors again questioning whether the big technology companies are overvalued. Google recently showcased the development of its new quantum computer chip, highlighting that future technology developments do not rest on AI alone.

The UK continues to see companies re-listing overseas to gain valuation advantages in the deeper and more liquid US markets.

Furthermore, the recent Budget’s increases in employer National Insurance Contributions may threaten company profits and drive inflation up as well. Investors have become more attracted to the UK again owing partly to lower equity valuations relative to the US.

Europe experienced more volatility, which came from political disputes in France and Germany. Investors have reduced allocations to the bloc in recent weeks amid a flurry of potential headwinds: political uncertainty, potential tariffs and weak economic growth. Long-term there are still attractive investment opportunities built on clean energy and AI, but short-term political risk may deter investors in 2025 from increasing allocations.

China has again been in focus with disappointing economic data and a brush with potential deflation. The government has announced intervention policies in the form of fiscal stimulus and a move away from Prudent monetary control towards a moderately loose strategy.

This has been positive for equity markets as it shows the government is taking the economic situation seriously. However, one would question why it has taken the government this long to change its thinking, as China has been battling a struggling property market for the last two years. Understandably investors are cautious and most agree that the Chinese government’s present intervention is not enough.

Areas of focus

Emerging market equities continue to have potential difficulties arising from a stronger US Dollar and higher US interest rates. Equities from India and Taiwan may face setbacks over valuation concerns but the long term outlook is still positive.

High yield credit spreads remain tight, but high yield bonds continue to yield around 7% and default rates remain low, showing strong fundamentals for the sector. However, as spreads are so tight, there is a risk asymmetry on the downside, i.e. returns will likely not improve but they could easily get worse.

Global smaller-company stocks look attractive amid potentially falling interest rates. They presently trade at a large discount relative to large cap stocks and offer potential diversification in light of strong large cap stock performance.

Short dated bonds are still more attractive than longer dated bonds. Short dated bonds offer an attractive yield and more protection should interest rates move less than expected (or more on the upside).

Thematic equities (AI, decarbonisation, infrastructure etc.) offer diversification from broad based asset classes in light of higher market volatility and short-term, more unpredictable market cycles.

European equities are cautiously underweight as difficult economic conditions, potential tariff impacts and cheap supply from China pose headwinds for equity markets.

Japanese equities continue to show strong performance and increasing corporate earnings are providing tailwinds for the asset class.

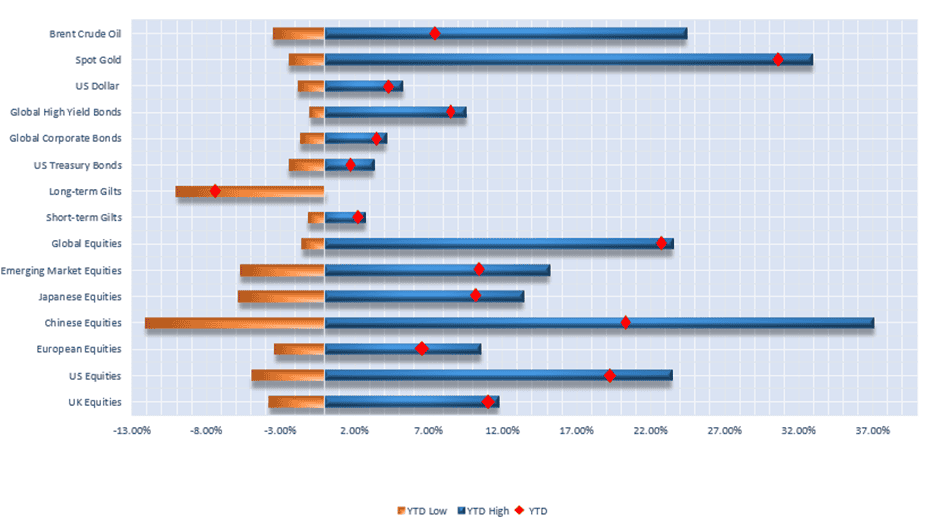

Selection of assets 2024 YTD returns and range of returns as at 12/12/2024 (the two ends of the bars represent the range of YTD returns and the red dots represent the current YTD return). Indexes used: FTSE All-Share, Russell 2000, STOXX Europe 600, MSCI China, MSCI Japan, MSCI Emerging Markets, FTSE UK Conventional Up To 5 Years, FTSE UK Conventional Over 15 Years, ICE BOFA US Treasury, ICE BOFA Global High Yield, ICE BOFA Global Corporate, US Dollar Index, S&P GSCI Gold Spot, S&P GSCI Brent Crude Spot. Returns hedged back to GBP with exception of US Dollar which is in US Dollar terms. Data from FE Analytics and MarketWatch.

UK

There are concerns about the knock-on effects of October’s budget, especially regarding the large increase in employers’ National Insurance contributions. Trade bodies have warned that this extra cost will will either be passed onto consumers, in the form of higher prices, or workers – through lower wage increases or lower employment. Ultimately, both of these are negative outcomes for the UK economy.

The recent budget has also caused investors to dampen their expectations of rate cuts next year, after Rachel Reeves announced £70bn in spending policies. Although promoted as a plan to boost investment, concerns have been raised about the inflationary impact of such spending – especially at a time when the economy appears to be operating close to capacity.

Since the budget, economists have adjusted their inflation expectations upwards by 0.2% from 2.6% to 2.8% in 2025.

In addtion to this, the unwillingness of the Bank of England to cut interest rates until service-sector inflation has fallen is restricting the growth in UK equties, espeically in smaller and mid-cap companies.

The Monetary Policy Committee of the Bank of England is due to meet next on 19th December for the final time this year, and almost two thirds of economists are expecting base rates to be kept on hold at 4.75%. Investment markets are also pricing in similar probablities.

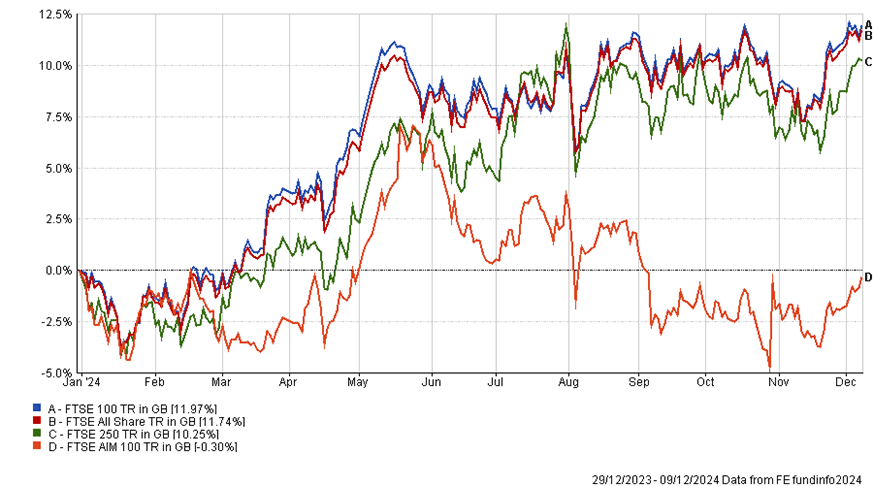

YTD returns of major UK stock market indicies

Large cap UK equties rose in Novemeber, with the FTSE 100 gaining 1.76% – boosted by strong returns in the financial sector. Smaller UK companies failed to gain traction over the month, and the FTSE AIM 100 is still negative year-to-date. This is despite a significant uplift after the Budget on 30th October, as investors had priced in harsher reforms to the Inheritance Tax treatment of AIM shares than was actually announced.

Construction equipment rental giant Ashted announced in early December that it plans to move its main listing from London to New York, dealing a fresh blow to the London Stock Exchange.

The FTSE 100 consistutent, and one of London’s most valuable listed companies, cited improvements in liquidity in the group’s shares given deeper US capital markets as the main reason for the move.

Ashted are not the first company, and will not be the last, that is seeking higher valuations across the Atlantic, putting further pressure on London’s status as a global financial hub.

Ashted’s decision comes as no surprise, however – the New York Stock Exchange (NYSE) and Nasdaq provide access to vast amounts of capital, and cater to high growth industries such as technology and AI. Higher trading volumes and a culture of innovation also makes US market listings more attractive for such companies.

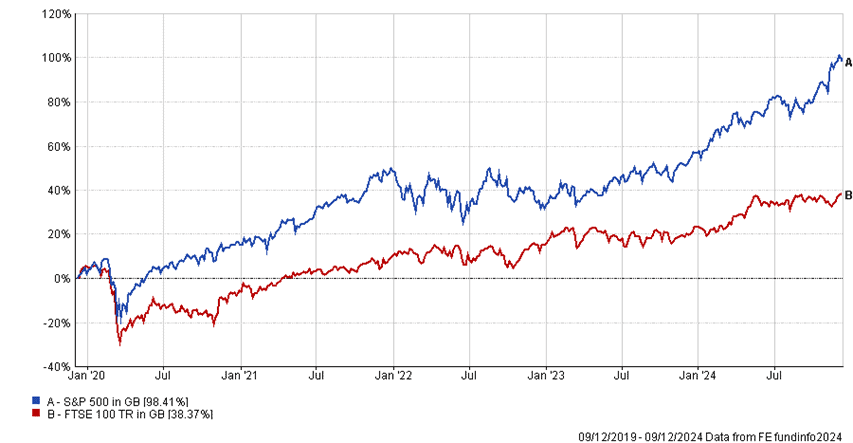

On the contrary, the preference for longer-term investment strategies in the UK, such as those used by domestic pension funds, can lead to lower investment returns. These trends are plainly evident in a comparison between the S&P 500 and the FTSE 100.

5 year performance of FTSE 100 and S&P500, showing the UK markets long term underperformance.

In the bond markets, UK gilts continued to sell off in early Novemeber in response to Trump’s election victory and the UK budget, both of which are expected to be inflationary. Despite this, bond yields failed to test last year’s all time highs. Although yields have fallen slightly over the past month, they remain higher year-to-date.

As further interest rate cuts loom, investors appear willing to lock in 4.5% returns in both US and UK bonds.

| Yields as of 10/12/2024 | Monthly change | YTD Change | |

| 2Y Gilt | 4.26% | -6.34% | 6.57% |

| 10Y Gilt | 4.30% | -4.91% | 17.67% |

UK bonds yields, monthly change and YTD change

USA

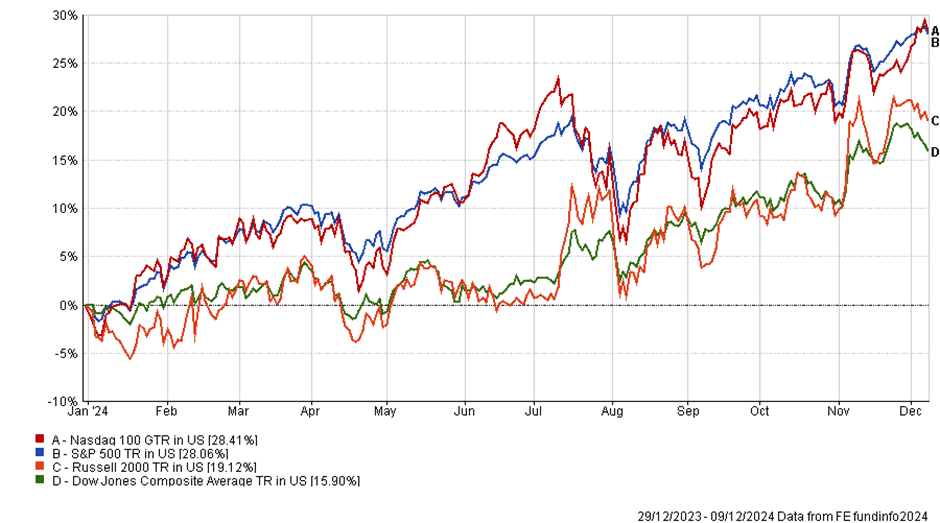

With the dust having settled from the US Presidential Election, we can clearly see how equity markets have interpreted the results. The S&P 500 is up 4.79% since November 5th with other equity indices posting similar gains.

The rise in prices can partly be attributed to the prospect of a Republican administration which tends to be positive for investments markets as opposed to a Democrat government, albeit the S&P 500 has returned 63.81% for equity holders over the course of the Biden administration. The other, and in our view more important reason, is the fact that markets prefer certainty.

The end of the year tends to be a strong period in terms of seasonality based on a phenomenon called the “Santa Clause rally”, however this tends to happen closer to the end of the year. The generally accepted period for this to occur is the final five trading days of the year and the first two trading days of the following year. There is some evidence to suggest that this phenomenon exists and is explained by reduced volume and optimism due to the festive period. Perhaps it has become a self-fulfilling prophecy.

Even if Santa Clause does not give the gift of even higher investment markets this Christmas, and barring any unforeseen catastrophise between now and year end, investors can celebrate 2024 as a successful year for market returns. As at the time of writing, the tech heavy NASDAQ 100 has returned a staggering 28.41%, whilst the blue-chip orientated Dow Jones Composite Average returned a very respectable 15.90%.

Since the S&P 500’s inception in 1957, the average annualised nominal return has been 10.26%. Whilst we remain optimistic about investment markets going into 2025, these types of returns are not to be expected every year. We will delve further into our 2025 outlook in a separate article.

| 22nd November 2024 | 10th December 2024 | Change | |

| US 2 Year Treasury Yield | 4.38% | 4.17% | -0.21% |

| US 10 Year Treasury Yield | 4.41% | 4.24% | -0.17% |

Change in US Treasury Bond Yields

Bond markets too have seen capital appreciation in the last couple weeks as investors price in an 88% chance of another 25-basis point rate cut at the Federal Reserve’s final meeting of the year.

That rate cut would put the Fed’s target rate at 4.25% to 4.50%. For reference, this time a year ago consensus (67.94%) was that rates would be below 4.00% after the December 18th meeting. Based on this, market projections for 2025 should be taken with a pinch of salt. As Powell continues to reiterate, future interest rate will be dictated by inflation and employment data.

The US CPI report showed that progress in bringing down inflation has slowed in November. This report showed a 2.70% gain over the year, which represents a 0.10% gain from the year over year figure in October.

Markets do not expect this to prevent the widely expected rate cut in December, but it will certainly induce caution for further meetings. The confirmation of a heating US economy was further supported by the jobs data, which showed a 227,000 increase in payrolls in November. This is up significantly from the upwardly revised 36,000 in October. Looking under the bonnet of October’s data shows that it is an anomaly caused by hurricanes Helene and Milton that swept the East coast through the month.

Other big news that will affect the US economy going forward is Donald Trump’s pick for key government positions. So far Trump has elected Paul Atkins to lead the Securities and Exchange Commission after Gary Gensler steps down.

Gensler was selected by President Biden in 2021 and his term was not scheduled to end until 2026. Gensler likely had no choice as Trump has publicly stated that he plans to sack the SEC chair in favour of a more “crypto friendly” chairman. Cryptocurrency markets duly rallied to all-time highs on the news. Trump has also selected David Sacks, a Silicon Valley venture capitalist and former Chief Operating Officer at Paypal, to become his AI and crypto czar.

Three other nominees that markets have interpreted as bullish for investments are Scott Bessent for the U.S. Treasury Secretary (who is widely respected by investors and policymakers alike), Peter Navarro as senior economic adviser, and Billy Long as IRS Commissioner.

Nominations must be confirmed by the Senate, but this is more of a formality with the Republican majority. Jerome Powell’s term as Chairman of the Federal Reserve is also set to end in 2026 and Trump has expressed that he does not plan to replace him before this. This is helpful given the concerns some investors hold about Trump eroding the independence of the Fed.

In summary, a government administration can only do so much and markets will continue to be dictated by company earnings and economic factors. Government policy can certainly act as wind in the markets’ sails. Company earnings look strong and the economy remains resilient, and there is further optimism arising from a favourable government and easing monetary policy. In the longer term, we are focused on larger thematic trends such as artificial intelligence and the energy transition, sectors in which US companies will likely be leaders.

Europe

Europe has faced numerous challenges in the last few months with political instability causing increased volatility in markets, the ongoing war in Ukraine still looming over the region and sluggish but improving growth all contributing to a difficult investment landscape.

The Eurozone’s two largest economies, Germany and France, have both experienced significant political difficulties.

The collapse of the German coalition government and the resignation of French Prime Minister Michel Barnier following a vote of no confidence in response to his proposed budget have caused much uncertainty and are arguably the biggest headwinds going into the new year.

Whilst the political climate remains in flux, the fiscal outlook for Europe in 2025 will also remain uncertain.

In France, Barnier’s proposed budget aimed to reverse the growing public deficit, which is projected to exceed 6% of GDP in 2024. This is a common problem among developed governments and one which the US will also have to consider when Trump enters office.

Passing an alternative budget before the end of the year seems unlikely, which will lead to the implementation of provisional measures mirroring the 2024 budget. The reprieve from increased corporate taxation, a key feature of Barnier’s budget, appears to have encouraged equity investors for now, although does little to address the underlying debt burden.

Long term, an increasing debt burden will put pressure on bond yields driving the overall cost of borrowing up as a potential oversupply will lower prices and investors will question the financial stability of the issuing government. This has wider implications as bond yields dictate the cost of borrowing for companies, which further feeds through to the prices consumers pay for goods.

The European Central Bank (ECB) cut interest rates by 25 basis points to 3% on Thursday at its final policy meeting of 2024.

This marks the fourth consecutive rate cut of the year. Inflation (CPI) sat at 2.3% in November, slightly increased from 2.0% in October. Whilst inflation has fallen significantly from a peak of 10.6% in October 2022 to within the ECB’s target range, economic growth remains sluggish. The ECB now faces a delicate balancing act as it attempts to stimulate growth and maintain the current inflation rate.

European equities have shown some resilience despite the challenging conditions following the volatility post-US election, with the STOXX 600 index appearing to show signs of recovery in the first week of December, up 1.48% in the past month.

The potential for Chinese stimulus through consumer demand could mean increased future demand for European luxury goods bolstering equities. However, Europe also faces competition from an oversupply of Chinese goods, lowering prices and causing European business earnings to drop.

European stocks have underperformed relative to the UK and the US (though mostly still positive this year), due to ongoing concerns about the impact of potential US tariffs and uncertainty over ongoing economic issues. Europe is expected to feel the brunt of any US tariffs with some economists suspecting that US Tarriff plans, if implemented, could knock 1% off GDP growth in Germany next year.

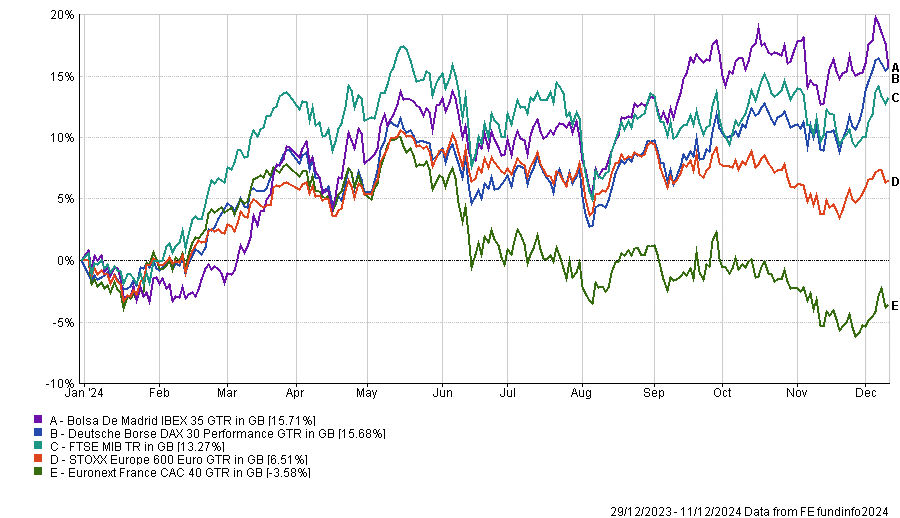

YTD Performance of EU Equity Markets

One notable exception has been the German DAX 40 index, which seems to have benefited in the post-US election period despite the country’s persistent economic challenges, reaching a milestone of 20,000 points for the first time in November (an increase of 21.80% YTD). This is in part thanks to the strong performance of certain sectors such as energy, AI and defense.

Long term Germany stands to benefit particularly well from future AI investment and the transition to clean energy, being a manufacturing-heavy country.

In November, most Eurozone countries saw a fall in 10-year government bond yields as investors favoured safer assets amid the political and economic uncertainties of the region weighing on growth expectations. Investors also expect interest rates to fall again, leading to a drop in bond yields across the board.

| Yields as of 14/11/2024 (%) | Change over one month (%) | YTD Change (%) | |

| Germany 2 Year Government Bond | 2.093 | – 6.74 | -18.71 |

| Germany 10 Year Government Bond | 2.341 | – 8.92 | 6.12 |

| France 2 Year Government Bond | 2.331 | -9.14 | -29.38 |

| France 10 Year Government Bond | 3.093 | -6.24 | 14.26 |

German and French Government Bond Yields

However, the spread between French government bonds and German Bunds reached 90 basis points (0.9%) in November, its widest in 12 years, before narrowing to 76.20 basis points (0.762%) in December.

This reflects increasing concern over how the future government will handle France’s growing debt problem. German bonds tend to be a proxy for the strength of the Eurozone economy and so any yield changes between German bonds and other European countries can reflect investor sentiment around that country.

The outlook for 2025 remains uncertain. As new governments take power in both France and Germany, fiscal policies are likely to shift, which could have significant implications for the Eurozone’s economy. The strategy that the ECB adopts in the coming months will be crucial in determining whether the region can regain stability and benefit from stronger growth in 2025.

Emerging Markets

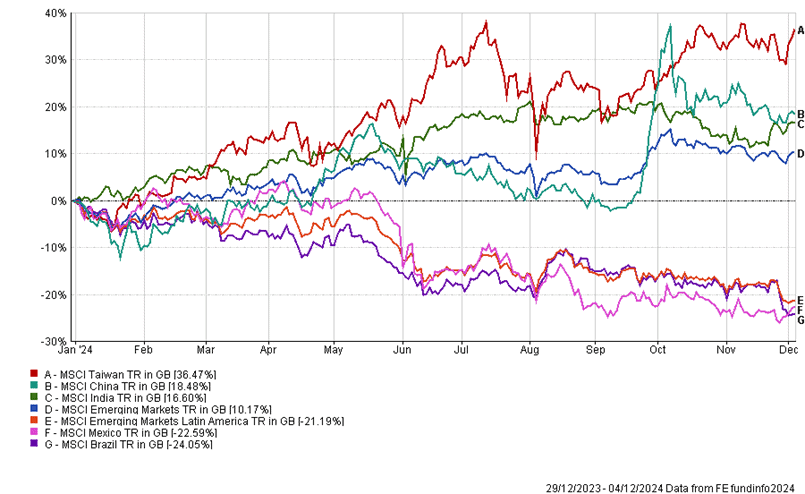

There has been considerable disparity in performance among individual emerging markets this year (see Latin America in the chart below), but as a whole emerging market equity markets have remained mostly in positive territory since January (returns hedged to GBP).

YTD performance of a selection of emerging market equity indices

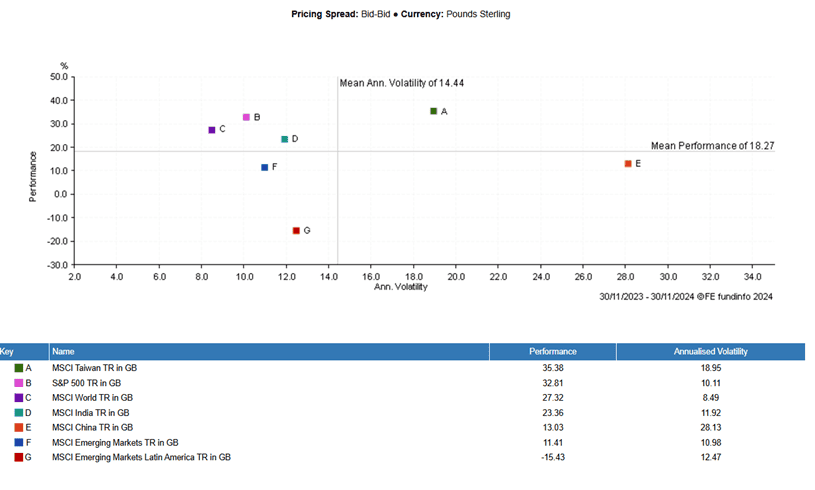

However, when we adjust the returns achieved for the level of volatility (i.e. looking at the return per “unit” of risk taken), emerging markets are still risk inefficient and have been for some time, that is the returns they generate do not compensate for the risk taken on (see scatter chart below).

One year scatter chart plotting risk and return profiles of emerging market equity indices

The MSCI World and S&P 500, for example, took on less risk over the past year but generated better returns (excluding MSCI Taiwan, which showed nearly 9% more volatility but only for just under 3% higher return).

If we look back even further (15 years) the broad indices of the MSCI Emerging Markets and the MSCI Latin America returned 109% and 9% respectively compared to 466% for the MSCI World (returns hedged to GBP). When returns are hedged to USD, the MSCI Latin America returned -13% over this period.

Therefore, it is fair to say that emerging markets as a whole have had a difficult time of it in recent years and one big factor involved in when investing in EM is currency movements.

With such strong equity performance in the US, investors have not wanted to take on the extra risk involved with investing in emerging markets, and this has been reflected by a falling allocation to emerging markets in portfolios. A strong US Dollar has also weighed heavily on returns as seen previously.

More recently, high US interest rates have held the dollar strong versus local currencies, making interest payments on emerging debt denominated in US Dollars expensive. This forced local governments to hold their interest rates higher than they otherwise may have in order to avoid further depreciation in their respective currencies. As high interest rates tend to negatively impact equity values and company profits, we have seen weak stock market returns and subdued economic growth.

Although China, Latin America and broad emerging market indices have struggled, individual countries such as India and Taiwan have flourished, delivering absolute returns (not adjusted for risk) above that of the MSCI World over the past five years. Taiwan has benefited from the drive in technology stocks and India has many technological, social and economic tailwinds behind it.

But with US rates starting to fall and oil prices lower, are we seeing a change in fortune for emerging markets?

Possibly, is the answer! But Tarriff man (Donald Trump) may cause further headaches for emerging markets.

As discussed in our last asset commentary Trump’s potential tariffs and tax cuts (more commonly referred to as protectionist policies) are likely to be inflationary which will keep US interest rates at otherwise higher levels and therefore strengthen the value of the dollar relative to other currencies.

Higher tariffs on imports could move US consumer demand away from imported goods, putting more pressure on local emerging market currencies. This will impact emerging market returns as in dollar terms, any returns will be removed by the appreciation of the dollar.

Many emerging countries such as Mexico rely heavily on exports to the US and with Trump threatening to impose tariffs on imports coming into the US, this will dampen demand for their products.

While the threats of tariffs could be a negotiating tactic (one which Trump liked to use last time he was in office), this will still create uncertainty in global markets. More so in emerging markets where liquidity is lower and volatility is higher.

With global inflation still at the forefront of investors’ minds, higher inflation still an ever present risk and global growth potentially fragile, any interest rate increases in emerging economies to reattract capital threaten to stamp out any growth.

Although as mentioned, India and Taiwan have delivered very strong returns both this year and over the past several years, investors are re-evaluating valuations in the sector. Taiwan in particular has benefited from the focus on AI and technology companies, but we continue to see real political risk in Taiwan due to an escalating trade tit for tat between China and the US.

If US interest rates continue to slowly decline and with oil prices much lower than they were one year ago, reduced inflationary pressures and the possibly of lower local interest rates mean investors can place more focus on emerging countries current account balances, foreign exchange reserves and overall lower finance costs, which tends to be a bigger focus for investors when looking at emerging markets.

Latin American countries in particular have had a poor time of it this year. Their performance is closely related to the performance of commodities (as they are heavy exporters) such as copper. Copper for example is down nearly 30% over the past year, and this is clearly reflected in the returns from Latin American equity markets.

Long-term the outlook for metals like copper is positive (think electrification, data centres and clean energy), but over the past year a struggling Chinese economy and declines in European manufacturing have caused an oversupply of copper. Therefore, the outlook for Latin America is far from clear, and certainly risky.

Returns in Chinese equity markets picked up from their lows in October amid the government’s announcement to step in with fiscal and monetary stimulation. Investors expect this to help the still struggling property market, but this intervention will likely fall somewhat short.

The Chinese property market, which has long been a driver of growth in China, has continued to pull down the economy with an excess supply over demand. On average it takes up to 28 months to sell a property in the largest Chinese cities, tying up consumer capital for over two years.

This over supply of property has pulled down prices nearly 12% this year, which is particularly painful for the average Chinese consumer, who typically has well over half of their net worth in property. Therefore without foreign investors placing capital in the stock markets, Chinese consumers are unable to.

Local governments have a huge debt load which is proving difficult to contend with. The central government could remove this from their balance sheets to encourage further support, but this would likely be a moral hazard as it can encourage local governments to essentially do what they want with minimal responsibility.

Long term structural issues within China threaten the Chinese economy with Japan style deflation, which would be hugely damaging for the economy. Falling birth rates are a major long-term issue for China as well, with 25% more people turning 60 than there are births each year.

With the US restricting exports of semiconductor manufacturing technologies, China has retaliated by restricting the export of metals such as Gallium to the US. This tit for tat trade war will only add fuel to the fire and likely deter investors from investing in the Chinese stock market.

While there are clearly headwinds for emerging markets, they still play a vital role in portfolio construction. Emerging market debt and equities provide important diversification and as we have seen, certain countries have managed to provide superior returns. Emerging market companies are also trading at an average 35% discount relative to their developed peers, offering pockets of opportunity in the broad sector.

Japan

Shareholder reforms have been the key theme for Japanese equities this year. Despite high market volatility, shareholder reforms combined with an uptick in inflation have contributed to renewed sentiment and positive performance in Japanese equities.

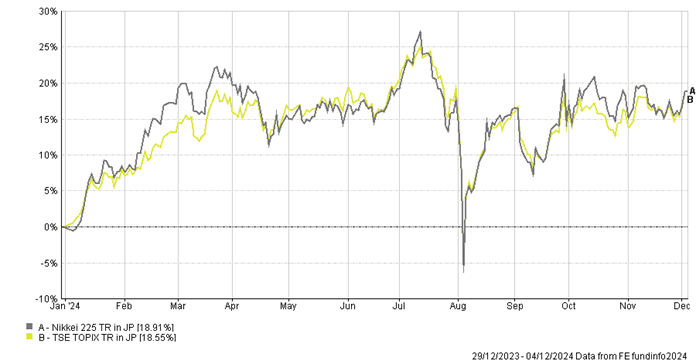

YTD performance of Japanese equity markets

Inflation has continued to rise in Japan with CPI reaching 2.2% on an annualised basis, increasing from 1.8% in October. This is positive news for the Japanese economy as price increases have continued to broaden out after years of deflation. Positive wage growth has prompted firms to increase the cost of their goods, and with further expected wage gains of 5% next year, we should continue to see this trend.

Investors are increasingly expecting the Bank of Japan to increase interest rates to ensure inflation does not become too hot. The debate is mainly around when this rate increase will happen, with investors split between a December or January increase. The BoJ want to focus on incoming data, in particular any potential wage growth in 2025. Expectations of higher interest rates have also increased the value of the Yen relative to the US Dollar.

As a country reliant on exports, a stronger Yen makes exporting more expensive and may act as a drag on corporate earnings. The economy has long hoped for inflation but if it becomes too hot and interest rates rise more than expected, a strong Yen will cause damage to the export demand. Couple this with potential import tariffs from the US and a decline in trade due to competition from China and we may again see the Japanese economy struggle.

Robert Dougherty, Independent Financial Adviser

Ryan Carmedy, Associate IFA

Harry Downing, Associate IFA

Fiona Chegwidden, Graduate Trainee IFA

December 2024

This article is not a recommendation to invest and should not be construed as advice. The value of an investment can go down as well as up, and you may get less back than you invested.