On 30th October, Rachel Reeves delivered Labour’s first UK budget in 14 years. This marked a significant change in approach to the UK’s public finances from the last government (and some say a departure from Labour’s own rhetoric before the election), with higher borrowing, higher taxes and higher spending on public services. Billed as a “Budget for growth”, the reaction from both markets and media commentators has been decidedly mixed.

The Bank of England also implemented its second interest rate cut of the year, reducing base rates to 4.75%.

If the Budget in the UK did little to inspire confidence in markets, the result of the US election has had the opposite effect.

After a globally significant year of elections, Donald Trump secured a second term as President, an outcome with substantial implications for US and international markets.

Optimism about the US economy’s near-term prospects remains strong, bolstered by expectations of business-friendly policies under Trump. Investors are particularly focused on the potential benefits of his more lenient approach to taxation (both for individuals and companies) corporate and regulation.

However, rising geopolitical tensions, especially regarding the Ukraine conflict, have tempered some of this enthusiasm. Ukraine’s use of Western-supplied weapons in attacks on Russian territory has provoked an aggressive response from Vladimir Putin, driving up oil and commodity prices.

President Trump’s return to office is likely to boost the US economy in the short term but could present challenges in the longer term, particularly around inflation and fiscal deficits. While these risks have not yet undermined investor confidence, the first half of 2025 will be crucial in determining how his campaign promises translate into policy and whether they could destabilize markets.

For now, US markets are reacting positively to expectations of Trump’s pro-business agenda, though the situation remains fluid. Investors remain cautious about the potential for negative consequences should his more controversial proposals take effect. Much will depend on how his administration navigates domestic policy and international challenges.

As markets digest these political and economic developments, both the UK and US face different but interlinked challenges. While the UK grapples with low productivity and growth, the US must balance short-term economic gains with long-term structural risks.

Areas of focus:

- Rachel Reeves’ first budget as Labour Chancellor increased borrowing, taxes, and public spending. Market reactions were mixed, with gilt yields rising and concerns about long-term growth and inflation remaining.

- Donald Trump’s re-election boosted US market optimism with expectations of business-friendly policies. Major indices gained, but concerns about inflation, fiscal deficits, and potential protectionist measures persist.

- The Ukraine conflict continues to impact global markets, driving up oil and commodity prices. Ukraine’s use of Western-supplied weapons and Russia’s aggressive response contribute to market volatility.

- Germany faces a second year of recession and political instability. European stock markets declined, and rising energy prices fuelled inflation concerns. The ECB’s recent rate cuts aim to manage inflation and support recovery.

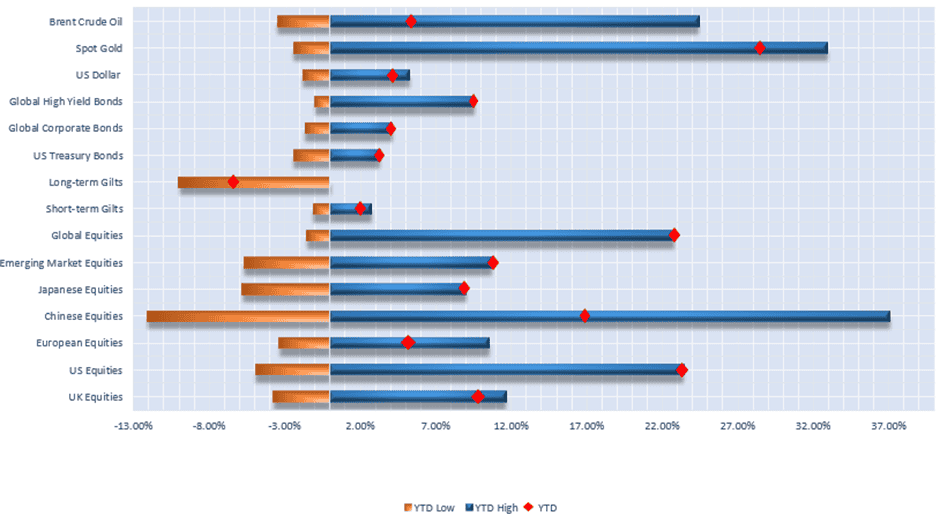

Selection of assets 2024 YTD returns and range of returns as at 26/11/2024 (the two ends of the bars represent the range of YTD returns and the red dots represent the current YTD return). Indexes used: FTSE All-Share, Russell 2000, STOXX Europe 600, MSCI China, MSCI Japan, MSCI Emerging Markets, FTSE UK Conventional Up To 5 Years, FTSE UK Conventional Over 15 Years, ICE BOFA US Treasury, ICE BOFA Global High Yield, ICE BOFA Global Corporate, US Dollar Index, S&P GSCI Gold Spot, S&P GSCI Brent Crude Spot. Returns hedged back to GBP with exception of US Dollar which is in US Dollar terms. Data from FE Analytics and MarketWatch.

UK

In the UK, Rachel Reeves’ first budget as Labour Chancellor has drawn attention for both significant increases in taxes and rising borrowing levels.

The immediate market response to Reeves’ budget was relatively calm. The independent Office for Budget Responsibility (OBR) forecasts significantly increased borrowing, but the reaction has been more measured than the volatility seen in 2022 under Liz Truss. UK 10-year gilt yields, however, climbed from 3.7% in late September to over 4.5%, their highest in more than a year, reflecting investors’ concerns.

Other than the rise in yields, the pound remained relatively unchanged and only the AIM market showed a significant uptick as a sign of investors’ relief that the changes to Inheritance Tax on these shares were less severe than had been expected.

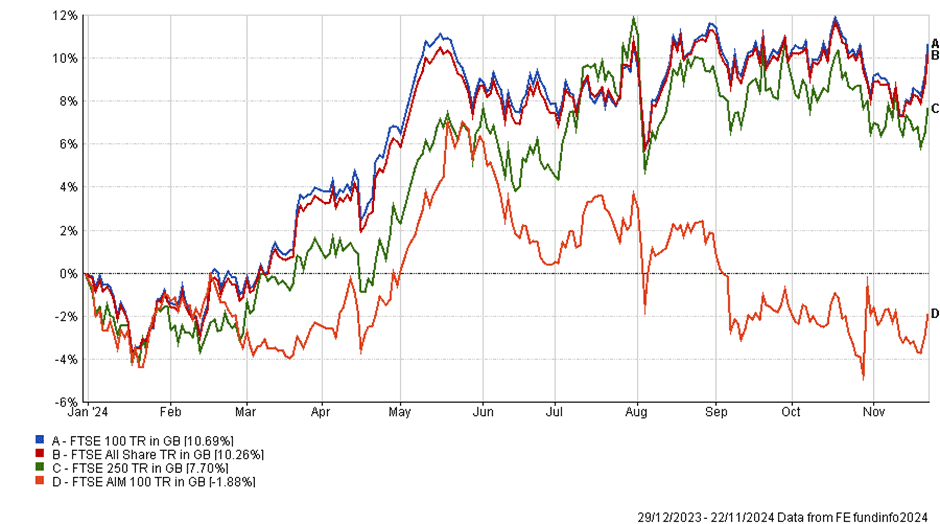

YTD Performance of UK Equity Markets

In stock markets, the FTSE All Share index saw a 1.20% decline over the month. The index is currently up 10.26% year to date, while the more domestically focused FTSE 250 is up 7.70% since the start of the year.

The muted response suggests that markets view the new Government’s economic approach as benign in the short term, although the long-term effects remain under scrutiny. A central question is whether the policy measures announced can stimulate UK economic growth.

Partly this will depend on how the additional government borrowing and tax revenues are spent. Success hinges on ensuring that the benefits of government investment in areas like technology and infrastructure outweigh the costs, including increased debt servicing and higher interest rates.

Other policy measures such as planning reform and improved trade relations will also play an important role in determining if (and how) the Budget announcements translate into economic growth.

Against that, business groups are already voicing their disappointment that the Chancellor has chosen to load them with significantly higher costs (in the form of increases to National Living Wage) and higher employer National Insurance Contributions. Added to this is the perception that taxing business sales more heavily and applying IHT to shares in businesses left on death is disincentivising the very companies and entrepreneurs which will drive economic growth going forward.

Economic indicators reflect this dichotomy and paint a mixed picture. Wage growth in the UK reached 4.3% in October, which, while outpacing inflation, raises concerns about inflationary persistence.

GDP growth was low at 0.1% for the quarter, underscoring the challenges the government faces in addressing the UK’s stagnating economy. Critics argue that the Budget and the Chancellor’s recent Mansion House speech lack the ambition needed to break free from the country’s current stagflationary malaise.

In bond markets, higher public borrowing levels and inflation forecasts are contributing to rising government borrowing costs and keeping downward pressure on longer-dated gilts.

Energy prices contributed to a rise in inflation from 1.7% in September to 2.3% in October and hopes for a further base rate cut in December appear to have receded.

The Bank of England’s base rate is currently projected to reach a “landing rate” of 3.5% from 2027 onwards, slightly higher than the 3.25% projection before the Budget. This anticipated slowdown in rate cuts suggests inflationary pressures may take longer to ease, impacting bond values.

Overall, while Reeves’ Budget has avoided any immediate market turmoil, it has not done much to alleviate longer-term concerns – the balance between boosting growth and managing inflation and borrowing costs remains difficult.

US

The re-election of Donald Trump as US President is expected to deliver positive outcomes for the economy and financial markets, and stocks have performed strongly since the result was announced.

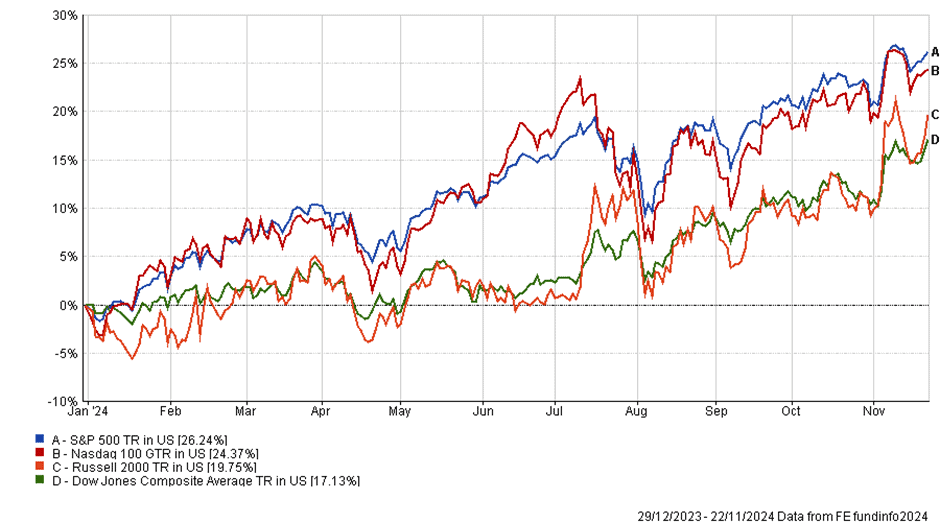

YTD Performance of US Equity Markets

The S&P 500 increased by 0.41% last month, while the tech-heavy Nasdaq grew by 1.35% and the Russell 2000 smaller companies index also grew by 0.63%. Since the beginning of the year, all major US stock indices have increased significantly.

It is important to note that our central view remains that the US Federal Reserve seems to have brought inflation back under control and that the US economy (arguably the most important driver of global growth) is ticking along nicely.

In the short term, Trump 2.0 has the potential to boost returns by way of lower corporate tax rates (a rate of 15% was proposed in the campaign) and cutting regulation. Corporate and individual tax cuts increase disposable income and profits, encouraging investment and consumer spending. Deregulation could also make companies more dynamic and competitive.

This prospect has certainly inspired investor confidence, but we think that investors will do well to consider the possible downsides of other aspects of Donald Trump’s policy agenda. These include a tough stance on both tariffs and immigration, both of which have the potential to push up inflation and decrease economic growth.

Tariffs may lead to increased consumer prices, potentially reviving inflationary pressures, while restrictive immigration policies could shrink the labour force, undermining long-term growth and exacerbating wage-driven inflation.

Trump’s decisive electoral win, including capturing the popular vote and swing states, has at least provided political certainty, a key factor valued by markets. With Republican control of both Congressional houses, the government is positioned to pass legislation more efficiently, alleviating the usual US political gridlock. This has initially buoyed markets, with US small-cap and large-growth stocks rallying and the dollar strengthening against major currencies such as the euro, yen, and sterling.

However, the victory has also amplified concerns about protectionist policies and rising deficits. Gold, which is priced in US dollars, has also seen downward pressure due to the dollar’s strength, and there is even concern that Trump will try to interfere with the independence of the Fed.

The inflationary outlook under Trump is therefore a key concern. Inflation expectations have already driven up US bond yields, making borrowing more expensive and eroding trust in the US as a global lender. National debt, currently nearing $36 trillion, could increase by up to $7.5 trillion under Trump’s policies, further straining fiscal stability.

The potential for a trade war remains a significant risk. Trump’s belief that tariffs will be paid by foreign exporters is widely disputed by economists, who warn of higher costs for US consumers and lower demand globally. A retaliatory cycle of tariffs could lead to a recessionary spiral, reversing progress made in stabilizing inflation and sustaining economic growth under previous administrations.

Health policy under Trump also raises questions. The nomination of Robert F. Kennedy Jr. as Health and Human Services Secretary caused turbulence in healthcare markets, with listed companies losing nearly 5% in value over a week. Kennedy’s controversial views on vaccines and public health could introduce unpredictability to the sector, further affecting investor confidence.

In broader economic news, inflation in the US has edged higher, rising from 2.4% to 2.6% annually, while core inflation remains elevated at 3.3%. Market expectations for Federal Reserve rate cuts have moderated, with only three additional 25-basis-point reductions anticipated next year, bringing the Fed funds rate to 3.75%. This shift reflects a recalibration of views on the trajectory of monetary policy amid the inflationary environment.

The immediate aftermath of Trump’s election has been characterized by volatility and mixed signals across asset classes. While small- and medium-sized US companies have seen gains, rising interest rates and inflationary concerns weigh on bond markets. Investors face a balancing act: embracing the near-term benefits of growth-oriented policies while grappling with the potential long-term costs of inflation and debt.

Financial markets have reacted to the election outcome with a mix of optimism and caution. Ultimately, Trump’s second term brings us back to the dynamic but uncertain economic period which characterised his first four years as president. While his policies may deliver short-term growth and market gains, the longer-term risks of inflation, deficits, and protectionism loom large.

The challenge for investors and policymakers will be navigating these competing forces in a politically-polarised environment, but we are reasonably confident that Trump will want strong stock market performance as his legacy and will steer clear of anything likely to derail markets.

Europe

Europe faces a challenging economic outlook as Germany, its largest economy, is projected to enter a second consecutive year of recession in 2024. Political instability has further complicated the situation, with Germany’s “traffic light” coalition collapsing, adding to the economic uncertainty.

The region also remains vulnerable to external risks, such as potential tariffs of up to 20% proposed by former U.S. President Donald Trump and weakening demand for its luxury goods from China, both of which have the potential to exacerbate economic stagnation.

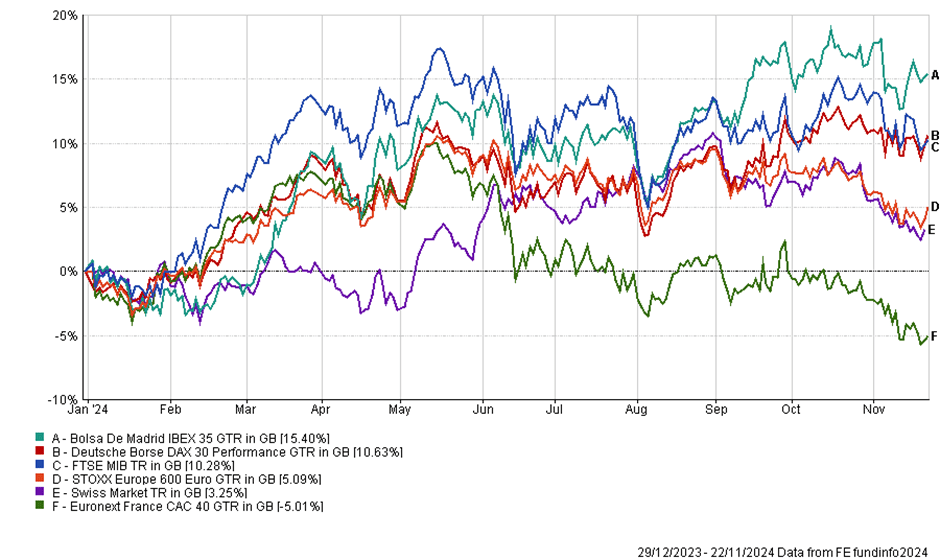

YTD Performance of European Equity Markets

European stock markets have reflected this uncertainty – the pan-European STOXX 600 index experienced its worst monthly performance in a year, dropping 3.4% in October.

Rising geopolitical tensions, particularly the ongoing and escalating conflict between Russia and Ukraine, have further pressured markets and driven up energy prices across Europe, stoking fears of inflation as we approach the colder winter months. Additionally, central bankers in Germany have expressed concerns over increasing corporate insolvencies and risks in the commercial property sector.

In light of these significant headwinds, investors could be forgiven for writing off Europe entirely. However, despite the challenges posed by the economic and political environment, recent data showed some resilience in the German economy, with GDP growing by 0.2% in Q3 (albeit after a 0.3% contraction in Q2). This contributed to better-than-expected growth in the eurozone, which expanded by 0.4% in Q3, outperforming economists’ forecasts of 0.2%.

In other good news, inflation trends in the eurozone have shown signs of improvement. Headline inflation (HICP) fell below the European Central Bank’s target of 2% for the first time in three years, reaching 1.8% in September before ticking back up to 2% in October. This decline has allowed the ECB to continue easing monetary policy, with base rates cut by 25 basis points in both September and October, bringing the rate to 3.25%. Further improvements in core inflation and a weakening demand outlook have heightened expectations for additional rate cuts in 2024.

The ECB’s policy moves have also influenced bond markets, with the yield on German 10-year government bonds falling from around 2.5% in June to 2.2%-2.3% in October. This reflects growing market confidence that inflation is under control and that interest rates will continue to decline, potentially supporting an economic recovery over the medium term.

Looking ahead, one further challenge on the horizon is the reinstatement of EU fiscal rules in 2025 and 2026 which constrain the size of countries’ budget deficits. These rules were relaxed in 2020 to help deal with the financial consequences of the Covid pandemic and will represent a fiscal tightening at a time when most other large economies are being more expansive.

In summary, Europe is navigating a complex mix of economic and geopolitical challenges. While there is some good news, such as improving inflation and higher than expected growth over the past three months, significant risks and structural weaknesses remain in key sectors and countries like Germany.

Robert Dougherty, Independent Financial Adviser

Ryan Carmedy, Associate IFA

Harry Downing, Associate IFA

November 2024

This article is not a recommendation to invest and should not be construed as advice. The value of an investment can go down as well as up, and you may get less back than you invested.