In the UK both equities and bonds produced positive returns over the month and the quarter, as investors gain confidence that UK companies can remain competitive in the global economy. Inflation falling below the Bank of England’s 2% target has given Andrew Bailey scope to signal more rate cuts before year end.

The European Central Bank cut its base rate for the second consecutive month for the first time in thirteen years. This helped to boost equity prices in the region, but low future growth prospects have restrained European investor optimism. Low Chinese demand has also taken its toll on the German economy (with its heavy manufacturing base), although the recent China stimulus and accompanying uptick has provided some relief.

In China, this government intervention has reassured investors that the state is willing to step in to prop up its struggling economy. However, analysts question whether the policies announced will be enough to support the woeful property market. A huge initial bounce followed by a significant retracement was experienced by Chinese equity investors.

US investors are gearing up for the November 5th presidential election and positioning themselves for the volatility that this could induce. Equity markets are marching on owing to strong corporate earnings and technological advancements, although bond yields have risen slightly as investors reprice the future path of interest rates.

Japanese equities also rebounded to finish the quarter mostly flat after the yen carry trade unwound spectacularly in August. Central bank comments and reasonable economic data provided some respite, but we still see issues around the yen. The outcomes of the ongoing elections should provide investors with some insights.

Finally, gold and other precious metals have risen further because of the prospect of lower rates and increased central bank purchasing. Oil remains weak due to concerns around stagnant global demand; however, OPEC supply cuts and geopolitical tensions could put upward pressure on prices.

Areas of Focus

Beijing steps up the stimulatory policy to support China’s struggling property sector, but questions are raised whether it will be enough.

Bank of England Governor, Andrew Bailey, signals more “aggressive” interest rate cuts as inflation falls below its 2% target.

US equities continue to outperform despite the uncertainty around the upcoming presidential election. Bond yields tick up slightly due to the release of economic data points.

European investors weigh up future growth prospects in an environment of lower interest rates.

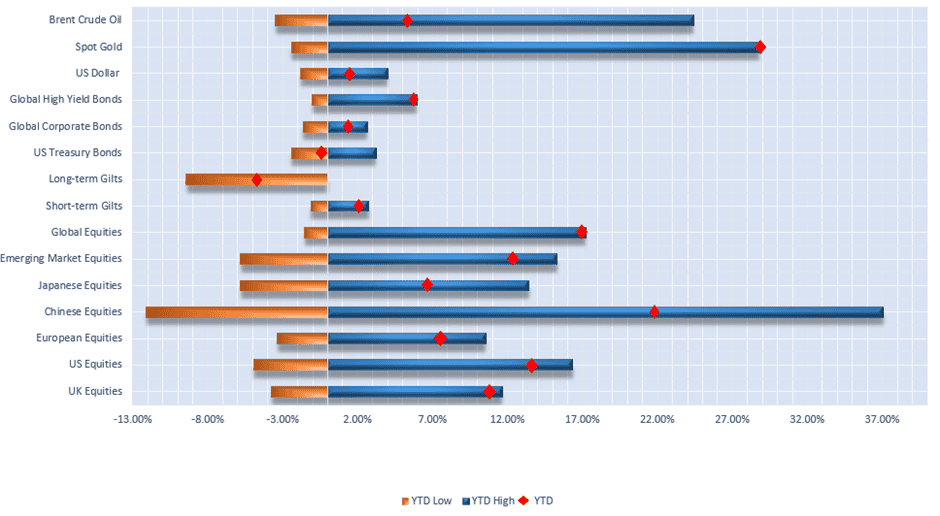

Selection of assets 2024 YTD returns and range of returns as at 19/09/2024 (the two ends of the bars represent the range of YTD returns and the red dots represent the current YTD return). Indexes used: FTSE All-Share, Russell 2000, STOXX Europe 600, MSCI China, MSCI Japan, MSCI Emerging Markets, FTSE UK Conventional Up To 5 Years, FTSE UK Conventional Over 15 Years, ICE BOFA US Treasury, ICE BOFA Global High Yield, ICE BOFA Global Corporate, US Dollar Index, S&P GSCI Gold Spot, S&P GSCI Brent Crude Spot. Returns hedged back to GBP with exception of US Dollar which is in US Dollar terms. Data from FE Analytics and MarketWatch.

UK

UK inflation slowed more than anticipated last month with the Consumer Price Index (CPI) falling to 1.7%, largely due to lower energy costs and a slowdown in services inflation. Core inflation, which excludes energy prices, also eased but remained elevated at 3.2%.

Additionally, average shop prices declined in September as many UK retailers introduced discounts to attract customers after weak summer sales.

The British Retail Consortium reported that average prices dropped by 0.6%, with non-food items seeing a more significant decline of over 2%.

GDP growth for the month was 0.2%, and the combination of slower growth and easing inflation has heightened the likelihood of the Bank of England reducing interest rates again next month.

Meanwhile, the UK housing market is showing signs of recovery. Zoopla reports that residential sales are up 25% compared to the same period last year. Nationwide also indicated that average house prices have risen by 3.2% over the past year, marking the fastest growth in over two years.

Consumer confidence fell in September ahead of October’s UK budget announcement, which is expected to outline harsh measures to help address the £22bn “black hole” labour claim to have discovered in the public finances.

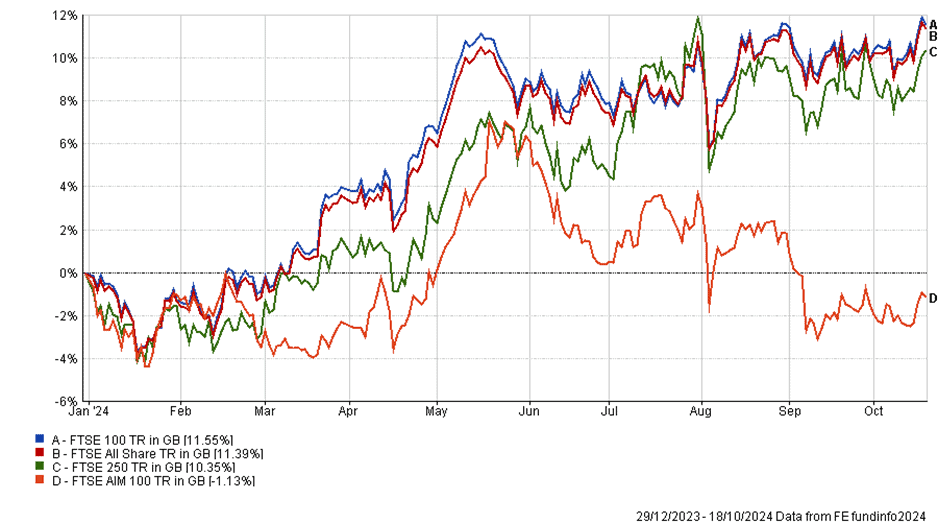

YTD Performance of UK Equity Markets

Although the UK experienced slow GDP growth, the FTSE 100 index outperformed other developed markets over the last quarter.

Falling oil prices restrained performance in the larger UK companies, with small- to mid-cap stocks outperforming. At the sector level, consumer staples and utilities were the best performers within the UK, with energy stocks underperforming given global growth concerns.

Within fixed income markets, the prospect of greater interest rate cuts helped to reverse some of the recent decline in gilt markets.

| Yields as of 14/10/2024 | Monthly change | YTD Change | |

| 2Y Gilt | 4.17% | 8.87% | 4.56% |

| 10Y Gilt | 4.24% | 10.85% | 16.51% |

UK Bond Yields as at 02/09/2024, monthly change and YTD change

Shown above, gilts are now positive year-to-date. Longer dated bonds (which are typically more sensitive to interest rate movements) gained more traction over the month, although the performance of this asset class is still negative since the beginning of the year.

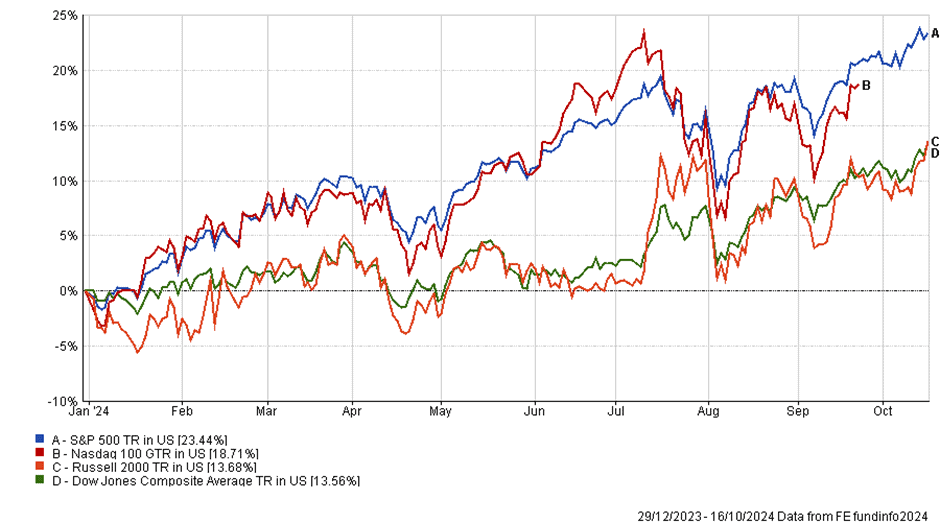

YTD Performance of US Equity Markets

All major US equity indices rose again in October with the S&P 500, Nasdaq 100, and Dow Jones Composite Average all at, or around, all-time highs.

The Russell 2000 index remains just shy of its November 2021 peak despite smaller companies mostly outperforming larger companies during the third quarter. That said, US large caps have still had their best first three quarters of a year since 1997.

This rally has mostly been concentrated on the largest stocks (the “magnificent seven” technology companies) but there are signs that it may be broadening, which presents opportunities for diversified, valuation driven investors. However, valuations can stay stretched longer than most investors can tolerate, and technologies such as artificial intelligence and robotics could continue to grow almost exponentially.

On robotics, Tesla held an event showcasing its latest updates on the infamous “Tesla Bot”. The event was named “We, Robot” (in reference to the 2004 science fiction film starring Will Smith “I, Robot”). Tesla’s CEO, Elon Musk, took to the stage to present humanoid robots and he claimed that for $20,000 to $30,000 you can have a robot do “basically anything you want”, from mowing the lawn to walking your dog.

Although the event may have provided some insight to what could soon be possible, Tesla shareholders were not impressed. Shares fell 8.78% as investors seemed to prefer the immediate gratification from improvements in Tesla’s unsupervised self-driving cars.

Equity markets may be choppy in the coming weeks, not only due to the presidential election (which we will discuss later) but because the third-quarter earnings season is well under way. Companies like JP Morgan and Netflix have all already reported – both companies beat analysts’ expectations and rallied after the release.

FactSet report that so far 79% of S&P 500 companies have reported an earnings per share positive surprise. Year-on-year earnings growth for is projected to be 3.4%, which is actually a downward revision from September (when a 4.3% growth rate was predicted). These downward revisions have certainly aided the “earnings beats” and boosted investor confidence.

With the Federal Reserve not meeting now until two days after the election, markets are pricing in a 90.4% probability of a 25-basis point cut to a target rate of 4.50% to 4.75% on November 7th and a 76.8% probability of another 25-basis point cut before year end. This is subject to change and as Jerome Powell insists, they remain data dependant.

The September CPI release showed that inflation was 2.4% over the past year. Core CPI came in above this at 3.3% (as this measure excludes food and energy, which are generally more volatile). The price of energy dropped 6.8% over the period, but both inflation readings were slightly above estimates.

Similarly, the unemployment rate fell to 4.1% and 254,000 jobs were added in September, which was well above estimates of 140,000 and the upwardly revised 159,000 in August. These data points put the Federal Reserve in a tricky spot – inflation is falling towards its 2% target, but the labour market appears strong, the risk being that premature cuts would stoke a resurgence of inflation.

| Yield at 15/08/2024 | Yield at 15/09/2024 | Yield at 15/10/2024 | |

| 2Y Treasury Yield | 4.10% | 3.60% | 3.96% |

| 10Y Treasury Yield | 3.92% | 3.66% | 4.04% |

Monthly Change in US Bond Yields

The chart above provides an update to last month’s chart where we discussed the “bull steepening” yield curve movement that has been playing out in recent months.

Although there has been a slight reversal in September, we believe the short end of the yield curve is still where rates have the most potential to reduce. Both ends rising together can simply be attributed to short term volatility around the data mentioned above and markets pricing in the risk that rates may stay higher for longer than they were initially anticipating.

Finally, this time next month the results of the much-anticipated US election will be in, and the new president will be settling into office. Polls currently have Harris as favourite at 48.4% to 46.4%; however, betting markets currently have it at 58.06% to 41.67% in favour of Trump.

There are pros and cons of both polls and betting markets in predicting the future outcome but by looking at both, investors can formulate a well-rounded view. For instance, polls offer a binary response and betting markets allow for betters to assess probabilities; equally, betting markets may express a bias towards longer odds whilst polls are a direct measure of voter intent.

Either way, in our view it makes sense to remain positioned for either outcome and not to try to make predictions – the election will be decided in the voting booths on November 5th.

Europe

Eurozone inflation fell below its 2% target last month. Combined with weak economic data, the European Central Bank (ECB) performed its first back-to-back rate cut in over 13 years. The ECB has now carried out three interest rate cuts so far this year, with its headline interest rate now 3.25%.

The Eurozone’s growth was minimal over the third quarter, with a stream of weak economic data and political uncertainty causing concern among investors.

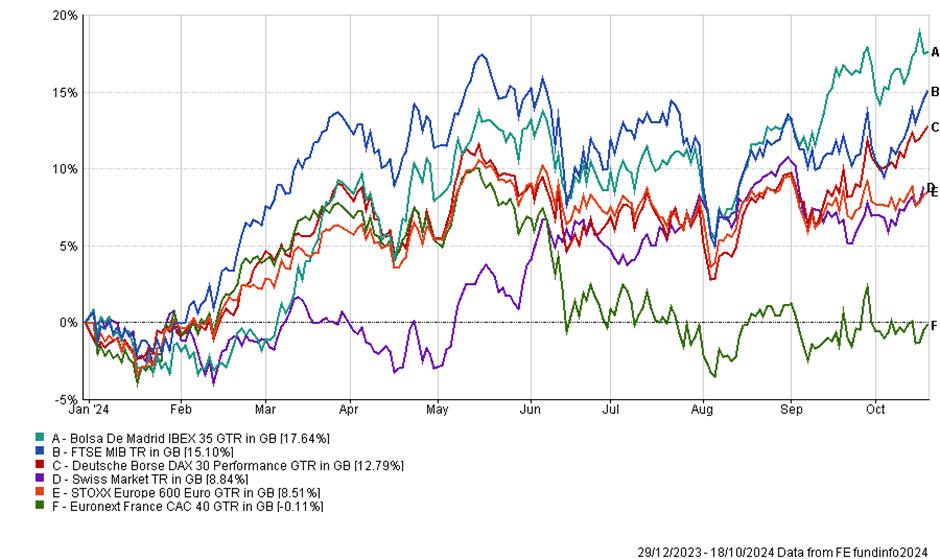

YTD Performance of European Equity Markets

Shown above, most European stock markets have witnessed positive returns since the beginning of the year. The French CAC 40 index is the exception to the rule, which is has returned -0.11% year-to-date.

Luxury goods manufacturers are facing challenges because of reduced demand from China and declining consumer confidence in Europe. LVMH, the world’s largest luxury conglomerate, reported a drop in sales, pushing its stock to its lowest point in over two years and negatively impacting the entire sector.

With an overreliance on China, reduced demand from the region also caused a further drag on the German manufacturing sector. It is too soon to determine whether the stimulus injected into the Chinese economy will resolve these issues, but volatility is likely in the short term.

Finally, European government bonds gained slightly over the month, as the ECB continue their rate cutting cycle as expected.

China

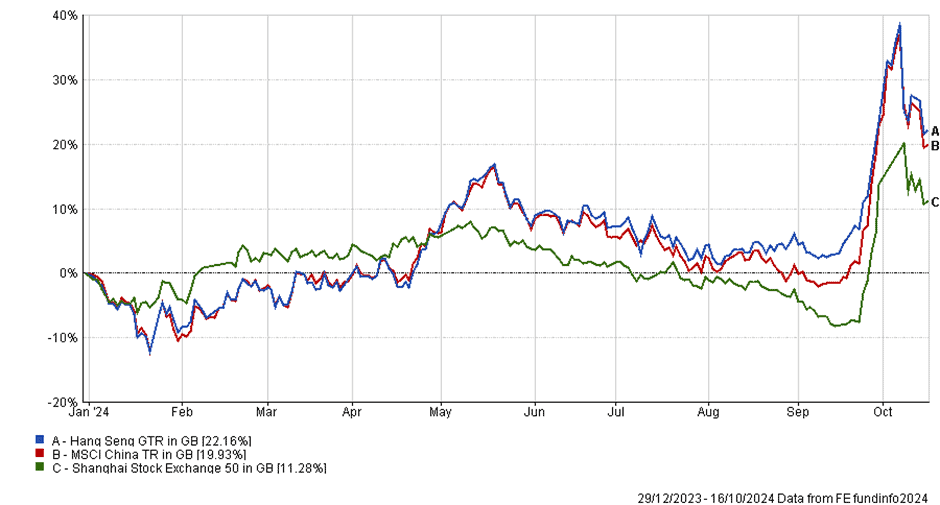

YTD Performance of Chinese Equity Markets

Since last month’s commentary, where we called for a bottom in Chinese equity markets, the major indices have risen extraordinarily in response to various policy changes announced by the government and various economic data points. The Shanghai Stock Exchange Composite and Hang Seng rallied 30.40% and 34.37% from the middle of September to the start of October before retracing 8.86% and 13.00% of those gains.

This initial bounce was driven by the wide, sweeping stimulus measures from the People’s Bank of China in an attempt to alleviate the widely covered crisis in the property market. The short-term reverse repo rate was cut from 1.70% to 1.50%. Another important policy decision taken was to cut the reserve requirement ratio (a ratio that determines the amount of assets a lender must hold relative to its loans).

The PBoC also signalled that further cuts could come by the end of the year, having only indicated tighter monetary policy two weeks before.

Both of these measures aim to support loan activity, but consumers and businesses likely need more reassurance before they begin to gear up again, high leverage being one of the main culprits which caused the problems in the first place.

Funding will be provided to the Chinese companies to conduct share buy backs and furthermore, officials announced a $71 billion fund to help brokers, insurance companies and funds buy Chinese stocks. It is anticipated that these two measures will help to inflate share prices with no real change in fundamentals.

Ultimately, in our view we must see a pickup in consumer confidence before the economic fundamentals and the investment case for China becomes positive again. The consumer confidence index still sits below 90 (a reading below 100 indicating pessimism). For reference, prior to the Covid pandemic the index was above 120.

After such an explosive rally in recent weeks, the Hang Seng had its worst trading day since October 2008, falling 9.40%. This was a case of investor expectation getting out of hand and the expectation that the stimulus efforts will not be sufficient to revive the world’s second largest economy. The yield on China’s 30-year government bonds also fell to 2.35%, whilst the renminbi weakened against the dollar.

Beijing has faced increasing scrutiny over its 5% annual growth target, which most economists view as extremely optimistic. The official third quarter GDP report showed growth of 4.60%, exceeding estimates of 4.50%. Along with this, retail sales and industrial production also managed to beat expectations, showing signs of recovery.

This month, Chinese investors will be keeping a keen eye across the Pacific at the US presidential election as the outcome may affect them more than other foreign economies. Most notably with Trump’s suggested trade tariffs (an attempt to protect US manufacturing). Tariffs effectively make Chinese imports relatively more expensive to US consumers, which will hurt the Chinese manufacturing sector seeing as the US is one of their largest buyers.

Given its size, the health of the Chinese economy has huge influence on global markets – especially commodities and the European luxury goods sectors. Both of these markets have been aided by the recent uplift in China, but how long this effect will last is up for debate.

Robert Dougherty, Independent Financial Adviser

Harry Downing, Associate IFA

Ryan Carmedy, Associate IFA

October 2024

This article is not a recommendation to invest and should not be construed as advice. The value of an investment can go down as well as up, and you may get less back than you invested.