If “higher for longer” means rates will remain above zero then this is very likely, unless some as-yet- unknown shock rattles global markets causing rates to dive back to zero (a “black swan” event).

Higher for longer could also mean that rates will drop but will remain high relative to the past decade.

And finally, it could mean that rates will stay where they are now. We think the second option is the most likely outcome.

Central bankers’ recent comments are trying to guide investors that rates could still go higher. Presently, it seems investors are not buying this line. It is entirely possible that central banks’ recent rhetoric is because if they said anything else, bond yields would drop further which would lower borrowing costs for companies and therefore would make the job of getting inflation sustainably down more difficult.

Central banks were also very wrong about inflation being transitory in early 2022 and they do not want to make another major policy mistake again, which would seriously damage market confidence in their ability to predict and control economies.

The probability of another rate rise is presently less than 25%, with investors instead betting on rate cuts in 2024. For Europe this is likely to occur sooner than in the US or the UK, with markets currently pricing in an ECB rate cut in the first two months of 2024.

For the US and the UK, any cuts are more probable towards the middle of 2024. European growth is sluggish, core inflation is falling and unemployment is rising. These three factors make a favourable case for lowering rates sooner. The UK’s growth is slowing but inflation is not as low as in Europe, and until inflation comes down further any rate cuts look unlikely.

US economic growth continues to puzzle investors, coming in strongly at 4.2% year-on-year. Jobs growth and the unemployment rate provided some respite with the data coming in better than investors’ expectations.

Investors should be wary that the path to interest rate and inflation stability is not a straight one – as we have seen this week in Australia, where after a pause in interest rate movements since June, the central bank has increased the interest rate again.

Equities picked up on this recent optimism with markets rallying in the last week of October. Bond yields also fell as debt issuance in the US slowed and jobs data leant in favourably as a sign of a potentially slowing economy.

Corporate earnings recently beat analysts’ expectations, but with financing costs and lower demand starting to eat into profit margins, we will likely see earnings under increased pressure in the new year. In the recent earnings season, any companies that missed their targets were punished heavily. Perhaps this reflects how tight valuations are and is possibly a sign investors have been overly-optimistic.

Chinese economic troubles continue to worry investors, with Chinese equities’ poor performance this year dragging down Emerging Market indexes overall.

Another loser of the strong US economy and the “higher for longer” mantra is Emerging Market debt. Higher rates are making it harder for weaker emerging economies and companies to pay their interest payments, with a greater proportion of government/corporate revenue being spent on debt repayments.

The proportion of countries with government bond yields more than 10% higher than that of US government debt has risen above 20%, much higher than any recent past period. Indications that a sustained period of high rates will cause long-lasting damage to these fragile economies are growing.

Areas of focus

- US equities restart their positive performance, with the NASDAQ gaining over 5% in the last week of October and mega-cap companies leading the way.

- High yield bonds remain a big risk as company defaults continue to rise. The high perceived credit risk is not attracting investors to this sector.

- Government bonds however are looking increasingly attractive with shorter maturities still overweight.

- Longer-term bonds begin to show promise as they are set to capture performance from interest rate decreases.

- UK equities are fairly priced, reflecting slow future economic growth.

- Emerging market government debt may come under pressure amid sustained higher global interest rates, particularly in the US.

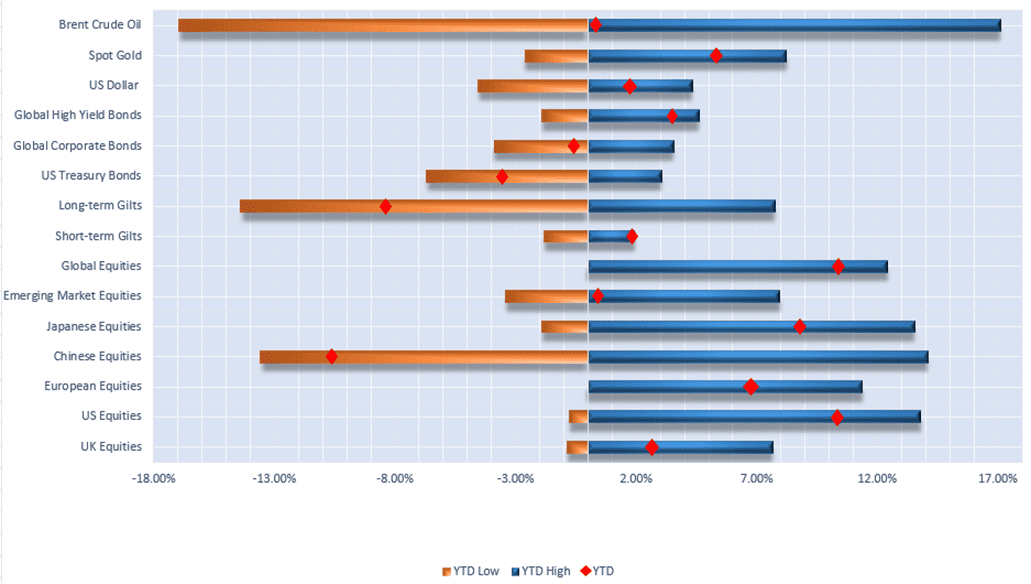

Selection of assets YTD returns and YTD range of returns as at 10.11.2023 (the two ends of the bars represent the range of YTD returns and the red dots represent the current YTD return). Indexes used: FTSE All-Share, Russell 3000, STOXX Europe 600, MSCI China, MSCI Japan, MSCI Emerging Markets, FTSE UK Conventional Up To 5 Years, FTSE UK Conventional Over 15 Years, ICE BOFA US Treasury, ICE BOFA Global High Yield, ICE BOFA Global Corporate, US Dollar Index, S&P GSCI Gold Spot, S&P GSCI Brent Crude Spot. Returns hedged back to GBP with exception of US Dollar which is in US Dollar terms. Data from FE Analytics and MarketWatch. Correct as of 10.11.2023.

UK

In line with the US Federal Reserve, the Bank of England held rates steady at 5.25% for a second time during its latest October meeting. The Bank of England governor, Andrew Bailey, once again reiterated the need for rates to be higher for longer and quickly dispelled any ideas of potential rate cuts anytime soon. Unable to completely rule out further rises, the BoE again highlighted the importance of bringing inflation back to 2%.

Andrew Bailey emphasised the challenges facing the UK over the next few years, with UK GDP growth forecast to underperform relative to international peers in the medium term and remain flat for the remainder of 2023. The latest growth forecasts point to a GDP figure of only 0.4% in 2024, which leaves the Bank of England little room to justify a further interest rate hike. While inflation is expected to remain more persistent than previously thought, it will likely drop next month as the Ofgem energy price cap reduction is accounted for.

Data released in October showed that the annual UK Consumer Price Index (CPI) inflation stayed flat at 6.7% in September. The Bank of England, along with many other central banks, is now facing a balancing act between tackling inflation and keeping an already weakened UK economy out of a deep recession.

It seems like tighter monetary policy is finally having a negative effect on consumption. This can be seen in consumer confidence in the UK, which fell approximately 43% in October – marking the largest drop since December 1994, excluding the COVID pandemic. Retail sales also fell 0.9% month on month in September.

With the festive season just around the corner, it is likely that retail sales will pick back up in the short term. Many households are struggling with heightened mortgage and rental costs, however, some consumers may have to use their remaining savings built up during the pandemic to fund Christmas.

Although the UK energy sector witnessed positive gains during October, the FTSE All-Share fell 4.1% over the month. Higher borrowing costs are now damaging UK-listed companies, and it appears that investors are finally coming to accept the “higher for longer” narrative.

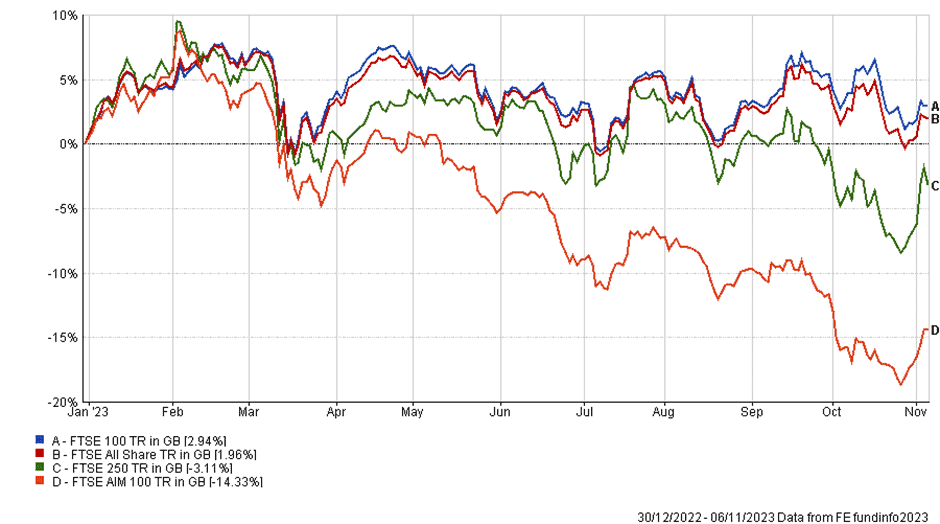

YTD performance of major UK stock market indices

The FTSE 100 has failed to gain traction in 2023 and has stayed roughly flat year-to-date, up 2.94% since the start of the year. It seems investors are unsure where the UK economy is headed, and many of them are waiting patiently for confirmation of its direction of travel. Until there is some clear evidence that points either way, it is likely that UK stock markets will continue to be both volatile and range-bound.

The FTSE AIM 100 fell even further during October and is currently down 14.33% year-to-date. Given the current economic environment and tight monetary policy, it is no surprise that the FTSE AIM is struggling this year. Smaller companies, usually more dependent on debt finance to grow their operations, are more prone to interest rate rises than their large-cap counterparts.

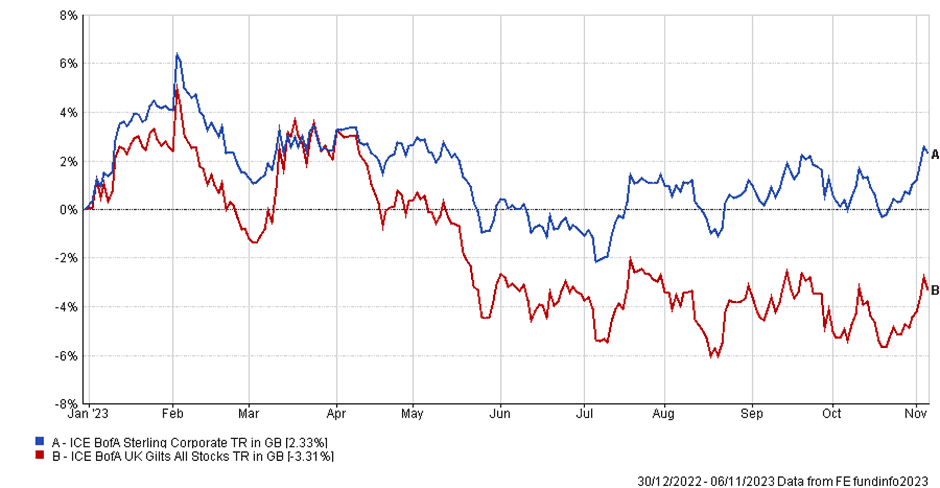

YTD performance of UK bond indices

In the UK, gilts witnessed a positive return in October. With a potential UK recession around the corner, some investors are moving away from risky assets into safer alternatives such as UK government bonds. The ICE BofA Sterling Corporate bond index, shown above, is still positive year to date and shows how corporate bonds are much less sensitive to interest rate rises than government bonds.

| Yield (%) as of 07/11/2023 | 1 month change (%) | YTD change (%) | |

| 2Y Gilt | 4.62 | 0.58 | 29.30 |

| 10Y Gilt | 4.31 | -3.86 | 17.95 |

As demand rose for UK government bonds last month, the yield on 10-year gilts fell by 3.86% in October. The yield curve remains inverted, hinting at economic trouble in the short to medium term. Looking forward, investors will need to keep a watchful eye on both credit and interest rate risk.

Europe

The European economy is on the verge of a technical recession, which is defined as two quarters of negative growth. Quarterly growth so far this year has been 0% in Q1, 0.2% in Q2 and the latest data showed that the eurozone economy shrank by 0.1% in the three months to September. Although Spain and France witnessed GDP growth, Germany offset the overall growth in the region.

After 10 consecutive rate hikes, the European Central Bank (ECB) sat tight during their October meeting and left rates unchanged at 4%. Christine Lagarde, like Andrew Bailey, remained hawkish – reiterating the ECB target of bringing inflation back down, and declining to rule out further increases.

There are signs that interest rates are beginning to have an effect in the Eurozone. Headline inflation fell significantly in October, from 4.3% to 2.9% – with the core rate at 4.2%.

Last month, investors became increasingly concerned about the economic outlook for the region. The latest data from the ECB showed a considerable reduction in the supply of credit to both households and businesses, hinting at lower consumption and lower future growth.

An increase in oil prices has also increased energy costs in the region, which has harmed productivity. In response, the STOXX Europe 600 fell 2.76% in October. Despite this recent drop in confidence however, the index is still up 5.17% year to date.

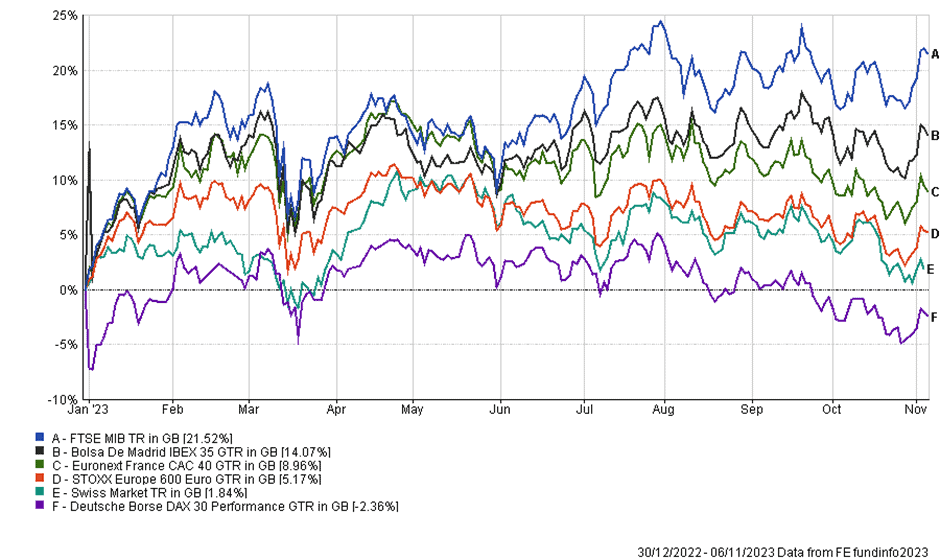

YTD performance of major Eurozone stock market indices

With the main German DAX 30 down 2.36% year to date, the German economy is now causing a drag on the eurozone stock market and is offsetting gains in other countries in the region. A large issue for Germany is its flagship automotive manufacturing industry, which is struggling to compete with an influx of relatively affordable electric imported electric vehicles from China (where manufacturers are being heavily assisted by the Chinese government).

While the German market is struggling, other European stock markets have witnessed significant gains in 2023. The Italian FTSE MIB has gained 21.52% this year while the Spanish Bolsa De Madrid is up 14.07% year to date.

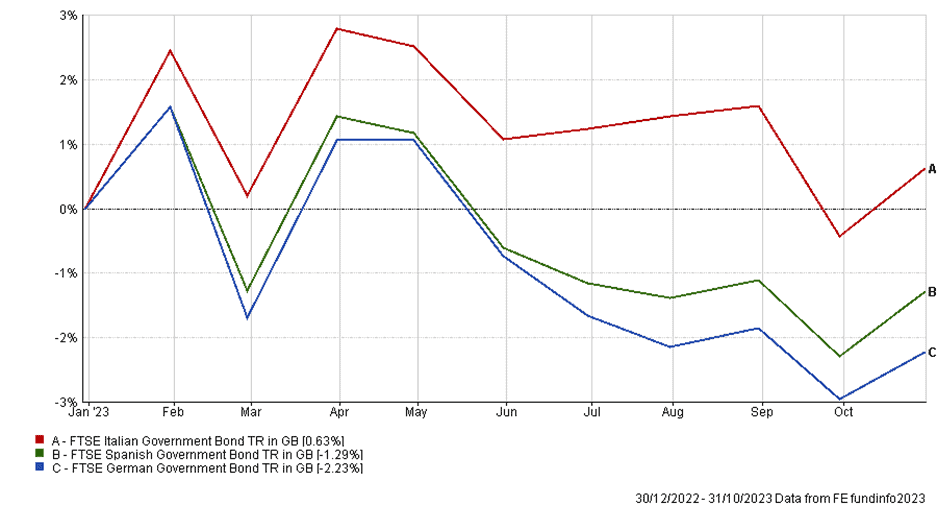

YTD performance of selected European government bond indices

As shown above, the price of European government bonds hit a new low at the start of October before rising again towards the end of the month. The yield on ten-year German Government Bunds crossed 3% for the first time in 10 years while Italian government bonds nearly reached 5% in October – the highest since the Eurozone sovereign debt crisis in 2012.

Given that Italy is one of the most indebted Eurozone member states, rising repayment costs could prove to be an issue for the Italian government. While both Spanish and German government bonds have fallen year to date, the FTSE Italian government bond index remains positive in 2023. With a higher yield, Italian government bonds are much less sensitive to interest rate rises than government bonds with less risk.

US

US markets have had their best week of performance so far in 2023, as the S&P 500 gained nearly 6% and the US 10-year Treasury yield fell over 40 basis points. This comes on the back of robust GDP data, cooling core CPI, and the Federal Reserve deciding to hold its benchmark rate at a 22-year high for the second consecutive meeting. Whispers of the illusive soft landing intensify as some investors believe we can evade the notorious lag effects of higher interest rates.

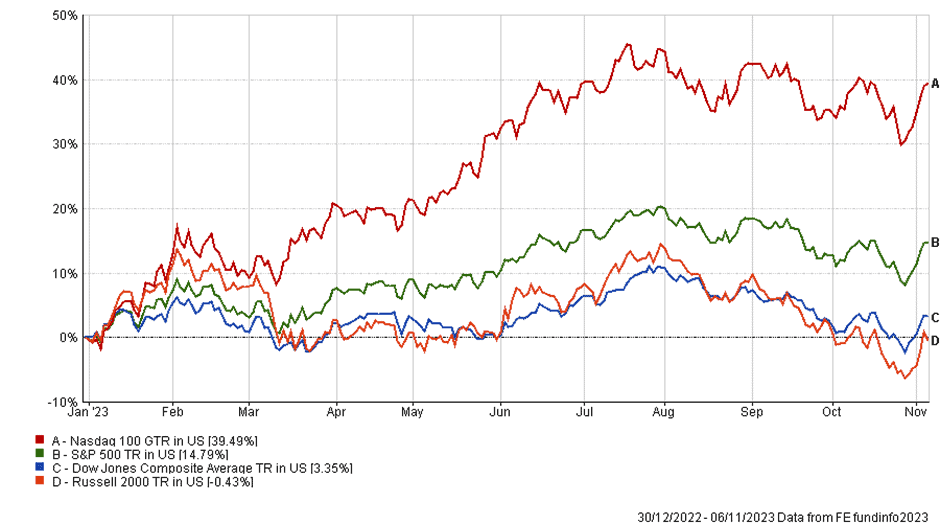

In the month of October however markets retreated slightly, the S&P 500 and Nasdaq 100 losing 2.13% and 2.04% respectively. The Russell 2000, which focuses on smaller US companies, dropped significantly more, giving up 6.84%. These movements highlight the importance of the so-called “magnificent seven” in the technology-heavy indexes. These seven mega-cap stocks make up nearly 30% of the S&P 500 index market capitalisation and over 40% of the Nasdaq 100 market capitalisation.

For comparison, the S&P 500 index is up 14.79% year to date whereas the S&P 500 equal weight index is actually down slightly by 0.32%. If you had held the Nasdaq 100 equally weighted from the start of the year you would have seen your gains shrink by 22.25% as opposed to holding the market cap weighted index.

YTD performance of US stock indices.

The question now is whether we will see these (historically expensive) large cap tech stocks continue to be as highly valued, or whether the comparatively unloved smaller companies will revert to the mean? Although the short term may look challenging, technology stocks may continue to trade at higher multiples in the medium to long term as they are best positioned to take advantage of the emerging global mega trends such as artificial intelligence and robotics, we believe.

Smaller companies have largely underperformed in 2023 as a result of higher interest rates. Smaller companies are generally more sensitive to higher interest rates because of their greater need for debt financing than cash-flush larger companies. As these lag effects filter through and companies with strong balance sheets prevail, a solid base for recovery may have been built for the well-known value stocks.

That said, the fastest interest rate hiking cycle in history has put the economy into uncharted waters and the consequences of this are still largely unknown. It therefore remains vitally important to take a proactive approach in terms of portfolio positioning.

The Federal Reserve decided to not raise rates during the latest monetary policy meeting, keeping the benchmark rate between 5.25% and 5.50%. Investors welcomed this decision – however, Fed Chairman Jerome Powell reiterated that he is not thinking about cutting rates and more work may have to be done to bring inflation back down to below 2%.

US CPI stayed at 3.70% in September, whilst core CPI (CPI excluding more volatile items like food and energy) ticked down to 4.10% from 4.30%. The Federal reserve focuses more on the core measure as it is believed that the price of oil, the main contributor to the energy component of CPI, is mostly out of their control. For our view on oil and other commodities, please see last month’s asset class commentary.

Fed Chair Powell must be cognisant of the fact that inflation may be structurally higher post pandemic as a result of fundamental supply chain changes such as onshoring.

Evidence would suggest that the US consumer is still strong after the third quarter GDP release which saw the US economy grow by 4.90% year over year. This is well above the second quarter growth rate of 2.10% and above analysts’ estimates of 4.30%. Couple this with resilient jobs data and it may seem difficult to argue that a soft landing is not looking very likely.

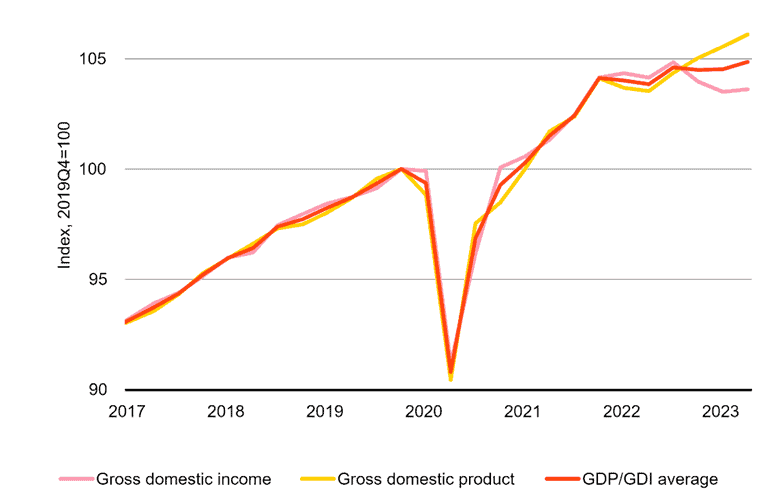

A chart showing US GDP vs GDI. Source: Blackrock Investment Institute

However, when you dig deeper into the data, some cracks appear as shown by the chart above courtesy of Blackrock Investment Institute. As gross domestic product is the sum of government, business, and household spending plus exports, gross domestic income only includes households and firms.

Households are the lifeblood of a healthy economy and can only be propped up by government spending temporarily. This discrepancy also comes at a time when household savings that were build up during the pandemic are starting to dwindle.

The bond market welcomed the news of potential terminal rates, the 10-year yield dropping from 4.93% to 4.52%. A breath of fresh air for bond investors after a sustained period of negative returns.

This perhaps reflects investor sentiment that rates at this level are not sustainable with rate cuts of 25 basis points becoming consensus in the middle of next year. The 2-year yield also came down slightly to around 4.93% but still above the 10 year. The reason for this is because the shorter you go in the yield curve, the closer to the base rate you get, albeit still inverted. Bond prices seem very attractive at current levels, being able to lock in a good return for a fixed period of time.

China

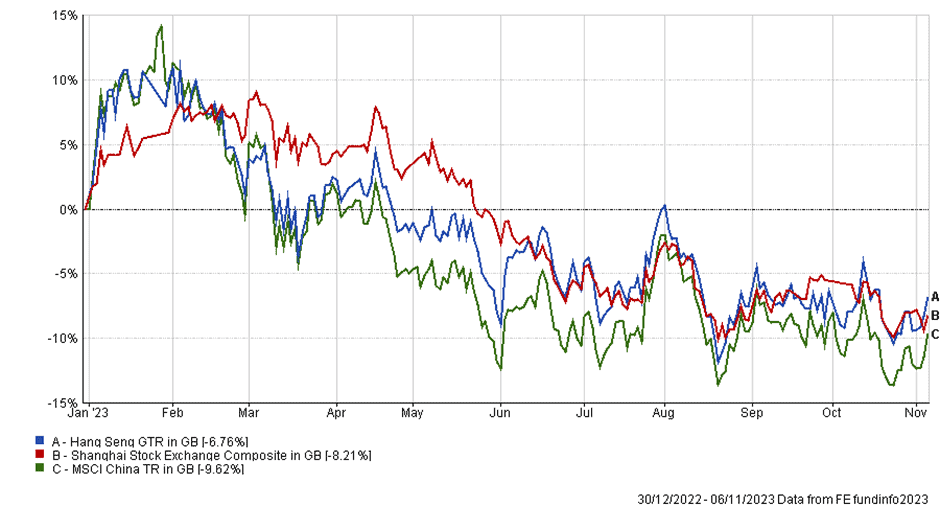

Chinese equities continued their sustained downward trajectory in the month of October, with the Shanghai Stock Exchange Composite Exchange and the Hang Seng losing 2.57% and 3.25% respectively. The MSCI China was down 3.70% as well.

Investors still doubt that China can recapture the same position it attained in the global economy over the last 25 years. During this time the country was able to build itself as a global manufacturer of cheap goods.

However, with post pandemic trends such as onshoring (or even “friend-shoring”) and competition from other developing nations, the Chinese economy may have to adapt and this is almost always a painful process.

YTD Performance of Chinese Stock Markets

This trend is highlighted by China’s most recent factory activity data release in the form of the Purchasing Managers’ Index (PMI). The October year on year PMI reading was 49.5, down from 50.2 in September (readings below 50 indicate contraction and anything above 50 indicates expansion). A slight contraction may not seem too bad, but remember that one year ago China was conducting nationwide lockdowns as part of their zero-Covid policy.

We have outlined China’s ongoing property crisis in our previous Asset Class Commentary, and this was underlined by new home sales data released in October which showed a decline of 27.5% from a year ago. An economy largely built on property will not fare well when population growth starts to level off and whilst new homes are still being built at a rapid pace.

That said, China are still widely expected to achieve their 5% GDP growth target in 2023, much better than other Western economies. However, Standard & Poor’s estimates that this could slow to as low as 2.90% next year.

Unlike many Western economies, China has low inflation. October CPI came in negative 0.20% year over year and the Producer Price Index declined by 2.60% over the same time period. This gives The People’s Bank of China (PBOC) plenty of room to offer monetary support if it deems it necessary. The one-year loan prime rate currently sits at 3.45% and the five-year at 4.20%; if rates were to be reduced it would likely put further strain on the Chinese Yuan, which is already down 5.38% compared to the US Dollar since the start of the year.

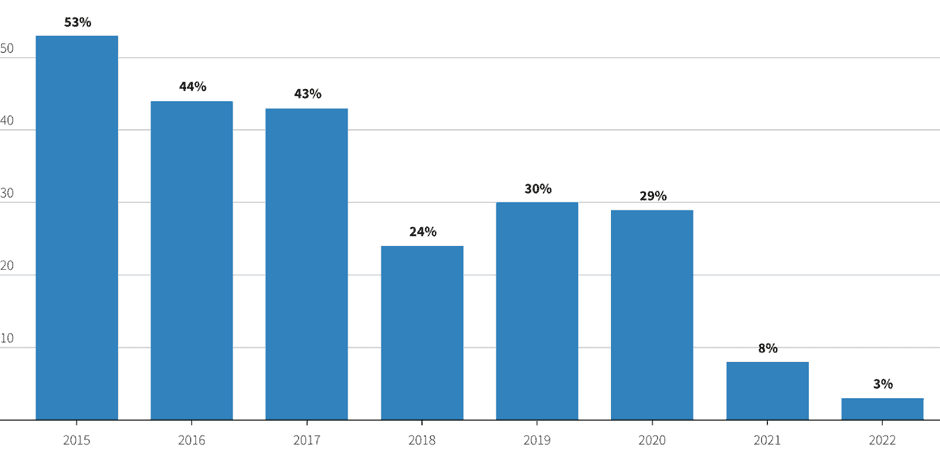

Investors may be hoping for a turn around in Q4 as a result of China’s Singles Day shopping festival, which is set to end this month. Singles Day is a Chinese holiday where unmarried people treat themselves to gifts and presents, and it has become by far the biggest online shopping day in the world. This increased consumption could spark some confidence in the Chinese consumer to go out and spend again. However according to a survey of over 3,000 Chinese consumers, most consumers are not planning to spend as much as usual on this year’s festival.

E-Commerce Singles Day Sales Growth From 2015 to 2022. Source: Reuters

A major talking point around the China and US tensions has been around chip manufacturing. The US has been trying to reduce its reliance on Chinese manufactured chips since the supply chain distribution of recent years. This strategy appears to be in full effect as China’s largest chipmaker, SMIC, reported a decline in third quarter profit by 80%.

On the other hand, one Chinese sector seems to be booming – electronic vehicles. China currently has the worlds largest EV market with over 5.9 million units sold in 2022, which represents 59% of EVs sold globally. Of this, 81% of sales come from domestic manufacturers (still largely unknown in Western countries) such as BYD, Wuling, and Chery. We maintain our neutral stance on Chinese equities as we believe a lot of the negative outlook has already been priced in with no clear catalyst to turn bullish again. In the longer term however, China will likely revert back to being a key component in the global economy – barring any extreme exclusions due to heightened China/US tensions.

Robert Dougherty, Associate IFA

Ryan Carmedy, Graduate Trainee IFA

Harry Downing, Graduate Trainee IFA

November 2023

This article is not a recommendation to invest and should not be construed as advice. The value of an

investment can go down as well as up, and you may get less back than you invested.