Accelerating UK consumer and business confidence points towards stronger economic growth, but retail spending, high wage growth and the more technical “composite leading indicator” (a combined set of economic measures which, when it reaches a trough, tends to point to an approaching recession within around 12 months) say otherwise.

Accordingly, UK equity markets have dropped again over the last month along with bond yields, as a stronger UK Pound weighs on overseas profits.

US equities also slowed this month after this year’s upward surge, with recent labour data showing that unemployment rose and inflation came down again. However, the rhetoric from top Federal Reserve officials remains that if economic growth is strong, rate rises are still on the table.

Many investors see US rates as having reached their peak, while Fed officials indicate there could be one more increase to come (bringing the headline US interest rate between 5.50 and 5.75%).

Whether we will see recessionary environments is very much a “crystal ball” question. While many professional guessers (sorry – economists!) believe we will see a recession of deeper magnitude than expected, an International Monetary Fund paper pointed out that economists are not very good at predicting the timing nor the magnitude of a recession. This is likely not news to many.

There are arguments for and against recessions based on current data, but the main issue is whether markets have priced in a slide in the business cycle. Even if we do not see a recession we are likely to see a continuation of the high volatility that has characterised the last two years.

Elsewhere in the world, the Chinese economy continues to disappoint investors as the expected rebound in growth from its economic reopening misses targets. The economic data coming out of China is also becoming harder to analyse as certain data is not being released, likely because it doesn’t paint a positive picture.

Although a difficult reality (note the demise of Wilko, for example) higher interest rates and recessions do act as a mechanism for eliminating badly-managed, highly indebted companies and those businesses which have failed to evolve. In turn, this will create room for new competition and growth, ultimately driving equity markets over the long-term. We are seeing in US high yield bond markets that the value of defaults for this year has already surpassed that of last year and company defaults are starting to increase.

While some industries and companies become redundant, other companies develop to fill the space left (think of Netflix replacing Blockbuster). Therefore, while a difficult time, the investment space is always evolving and as we said in our last commentary there remain plenty of exciting investment opportunities.

Areas of focus

- US equities move sideways after their positive performance. We may see investors engage in profit taking on the back of higher unemployment data, slowing this momentum.

- Chinese equities have had the biggest swing in performance this year, and their downward trajectory continues amid missed economic targets.

- Short-term government debt continues to offer yield advantages. With interest rates possibly staying higher for longer, any missed capital gains from decreases in rates is not likely.

- High yield bonds have seen increasing default rates in the US, and with credit costs high, companies have looked to secure their debt on company assets in an effort to refinance affordably.

- Higher credit costs also dim the medium-term outlook for smaller-cap stocks. A bottom-up selection here is key. US equities look more attractive than UK and performance continues to reflect this.

- Although lower than its year-to-date high, Emerging Market debt continues to look attractive as EM central banks are closer to unwinding their monetary policy. Soft currency debt (debt denominated in a local currency) faces pressure from possible devaluations in local currency from falling rates.

- Japanese equities have had a strong year with loose monetary policy and corporate reforms in the making. Risks of tighter monetary policy now weigh on investors’ minds and stock market valuations.

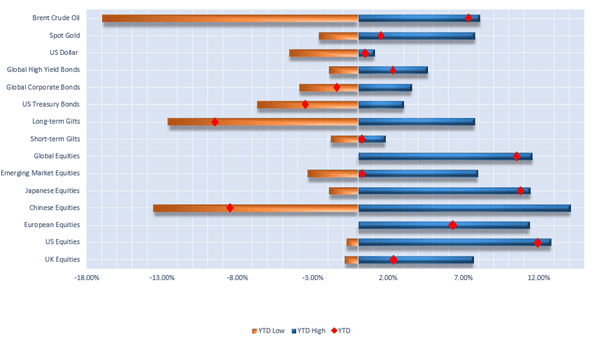

Selection of assets YTD returns and YTD range of returns as at 08.08.2023 (the two ends of the bars represent the range of YTD returns and the red dots represent the current YTD return). Indexes used: FTSE All-Share, Russell 3000, STOXX Europe 600, MSCI China, MSCI Japan, MSCI Emerging Markets, FTSE UK Conventional Up To 5 Years, FTSE UK Conventional Over 15 Years, ICE BOFA US Treasury, ICE BOFA Global High Yield, ICE BOFA Global Corporate, US Dollar Index, S&P GSCI Gold Spot, S&P GSCI Brent Crude Spot. Returns hedged back to GBP with exception of US Dollar which is in US Dollar terms. Data from FE Analytics and MarketWatch. Correct as of 08.09.2023.

UK

Driven by lower fuel costs, UK inflation continued its descent in August, falling from 7.9% to 6.8%. Whilst this reduction in CPI shows that recent monetary policy is working, the figure is still much higher than the Bank of England’s target rate of 2%. Although the latest figures suggested that UK unemployment increased marginally, wages remain elevated – increasing by a record 7.8% in the second quarter of this year.

Last month, the Bank of England decided to carry on with the interest rate hike cycle, raising interest rates by 0.25% to the highest rate in 15 years – 5.25%. Investors widely expected a rise last month, but a large majority of investors were pricing in a larger increase of 0.5%. News of a smaller 0.25% rate hike caused further volatility in the yields on UK gilts, with yields initially falling before rising sharply again.

Most investors now forecast a peak Bank of England base rate of 5.75%, which is expected to occur in the last quarter of 2023. How the Bank of England positions itself next year is still up for debate. Andrew Bailey, the Bank of England governor, has recently warned investors that he expects rates to remain high for some time (in keeping with investors’ predictions that rates will stay “higher for longer”).

Another source of major domestic economic news last month stemmed from research by mortgage lender Nationwide. After a reduction in house prices of 0.8% between July and August, Nationwide’s analysis suggested that UK house prices fell at the fastest annual pace since 2009 in August.

The research also indicated that the average house price in the UK is now £259,153, down from a peak of £274,000 in August 2022, marking a fall of 5.3%. This reduction can largely be explained by the effects of increased interest rates, which have been passed onto homeowners in the form of increased mortgage rates and tougher mortgage affordability.

Although house prices have fallen significantly, it is important to consider how inflated house prices were during the COVID pandemic – especially in areas such as here in Cornwall. House prices have now returned to more sustainable pre-pandemic levels. Although increased borrowing costs have led to a major decrease in mortgage approvals, Nationwide remain optimistic of a soft landing for the housing market. They believe that low UK unemployment and the relatively high proportion of borrowers on fixed rate mortgages will mitigate some of the downside risk in the market.

The reduction in house prices, for the most part, is being led by rising borrowing costs. However, increasing interest repayments also influences the macroeconomy – especially in the UK, which is traditionally led by consumption. Homeowners on a variable rate mortgage have less disposable income which is having a knock-on effect on other sectors, such as the retail sector.

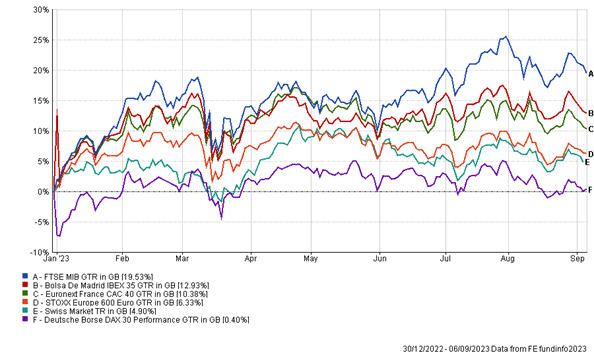

YTD performance of UK stock market indices

Like the weather, the performance of UK equities has been rather lacklustre this summer. The prospect of continued interest rate hikes by the Bank of England damaged the performance of all the top UK indices last month, which widely underperformed their international peers. While last year the FTSE 100 outperformed, the lack of growth industries in the index (such as the technology sector) has hampered the UK stock market and resulted in other markets catching up in their performance.

The FTSE 100 had a difficult month in August, losing most of the gains made throughout the year to date, before regaining some value towards the end of the month. Rolls-Royce was one of the indices’ best performers during the month, as air travel continues to grow post-COVID.

In contrast, asset manager abrdn fell 25% over the month. This drastic fall in share price can be attributed to poor financial results earlier this year.

After years of negative outflows, abrdn have chosen to close their Global Absolute Return Strategies fund, which was once the largest investment fund in the UK. This led to the company being dropped from the FTSE 100 during the index’s quarterly reshuffle at the end of August. Being demoted from a major index such as the FTSE 100 often causes a further downward trend in pricing as funds which track or invest in FTSE 100 companies are forced to sell the stock.

The FTSE 100 AIM index also continued to decline last month, down almost 10% year-to-date. This is somewhat expected as smaller companies tend to fare worse than large cap stocks in a high interest rate environment. US smaller companies, while having a volatile month, have however experienced positive performance this year. This again highlights the tough environment UK companies are having to work in.

| Yield (%) as of 07/09/2023 | 1 month change (%) | YTD change (%) | |

| 2Y Gilt | 4.907 | 0.00 | 37.42 |

| 10Y Gilt | 4.476 | 2.45 | 22.44 |

The yield on 2-year gilts remained unchanged over the month and currently sits at 4.907%, while the 10-year gilt yield rose by 2.5% over the month up to 4.476%. This was due to rising interest rate expectations on the back of record wage growth data, as mentioned earlier. This means that the yield curve remains inverted in the UK, a feature which has historically predicted recessions. Investors will also be pricing in a higher “term premium” as expectations for inflation settling at higher levels are reinforced.

Europe

Like many other developed economies, European economies are still battling inflation. Although it has decreased significantly from its peak in October last year, headline inflation remains well above the ECB’s target at 5.3%. For this reason, markets continue to price in at least one further ECB rate hike before the end of 2023.

Growing evidence that the Chinese economy is stalling and struggling to return to pre-COVID prosperity is also causing investors to be concerned about European equities, which rely heavily on export-driven demand from China.

In response, Europe’s Stoxx 600 index shed about 5% of its value in the first three weeks of August, before regaining some of this lost value in the final week of the month. Nonetheless, Morgan Stanley expects European stocks to fall by 10% during the summer due to high interest rates, a worsening Chinese outlook and tightened credit conditions.

YTD performance of European stock market indices

While countries such as France and Spain have been enjoying positive returns led by increased exports and tourism so far this year, the largest economy in Europe, Germany, is in recession. The chart above shows this divergence clearly. The Spanish IBEX 35 and French CAC 40 have both increased by over 10% year-to-date while the German DAX 30 has remained relatively flat, increasing by only 0.4% over the same period.

Germany’s automotive industry, a big contributor to the country’s economic growth, has been struggling in recent months. German car production fell by 9% between August and July, exceeding economists’ expectations. Whilst the automobile industry seems to be the hardest hit, all manufacturing groups have been affected – production is down 0.8% over the month. High energy costs are thought to be causing a retraction in growth, with energy intensive industrial branches down 11.4% annually. Germany’s cost of energy remains much higher than that of the US, which is a major manufacturing export competitor.

Another factor that is restricting output in Germany is the lack of available labour. A recent survey of 9000 companies discovered that 43.1% reported a shortage of qualified workers. This adds to rising fears that German industrial groups could shift most (if not all) of their production abroad, where labour is cheaper and more readily available.

Looking forward to Q4 in the region, economists will once again have to become meteorologists (who typically are better are forecasting, at least over the next week!). Last winter turned out to be milder than anticipated, which stopped energy shortages materialising. While gas storage is at peak levels, a colder than expected winter could lead to volatility in energy prices and a further decline in the European economy.

Turning to the banking sector, last month UBS reported a record quarterly profit of £29bn – which can be almost entirely explained by the accounting boost linked to taking over rival Credit Suisse. UBS were able to acquire Credit Suisse’s assets at a large discount, albeit they took on a lot of risk at the time. Fears of an international banking crisis have now been tamed almost entirely, but UBS still has some hurdles to jump. Political tensions are high at present, as UBS have recently announced that they plan to cut around 3,000 jobs over the next couple of years.

Eurozone bond yields were heavily influenced by Bundesbank President Joachim Nagal last month, who, in keeping with fellow central bankers internationally, hinted that interest rates would be “higher for longer” across the region. This led to an increase in yields across the Eurozone, especially in Germany. The yield curve remains inverted, indicating a deeper recession for the economy. The yield on 2-year German government bonds currently sits around 3.09%, while the 10-year yield sits lower at 2.62%.

US

US markets took a step back in August after an explosive first half of 2023 – the Russell 2000 and Dow Jones Composite Average gave back 3.94% and 2.62%, respectively. The S&P 500 and Nasdaq 100 continue to outperform the other US indices, even in negative months, with the S&P down 0.69% and the Nasdaq down 0.56%.

Since the start of the year, investors have been pricing in a goldilocks scenario with inflation coming down rapidly, unemployment near historic lows (although ticking up), and better than expected economic data, all despite the Federal Reserve’s fastest rate hike cycle in history. These increases have brought the Fed’s funds rates from near zero to between 5.25%-5.50%.

This halt in performance signifies investors bringing expectations back to reality after an earnings season that showed signs of stagnation. Profit margins grew as a result of lower input costs; however, this will likely normalise due to inflation bottoming (or even rising) and labour shortages putting upward pressure on wages.

Energy and consumer discretionary were the best performing sectors in the month as oil continues to rise and the US consumer looks as resilient as ever. Consumer spending grew 4.20% in Q1, 1.70% in Q2, and is tracking to rise to 3.20% in Q3. Although this may give markets relief in the short term, we believe it may be unsustainable owing to the time-lagged effects of interest rate hikes, which are still to feed through to the real economy. Consumers are always more positive in the summer with spending typically higher, leading to inflated economic readings

YTD performance of major US stock market indices

One of the reasons interest rate hikes slow inflation is by disincentivising spending and making it more attractive to save money. Now that we are starting to see high yielding interest rate accounts becoming available to the consumer, they may decide to top up their savings rather than purchase the latest iPhone.

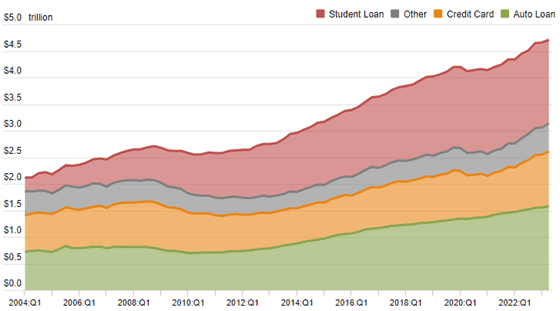

Pair this with record levels of debt (now $17.06 trillion) falling due at a new, much higher interest rate and consumer spending may run into trouble (see chart below).

Housing US Consumer Debt. Source: Federal Reserve Bank of New York

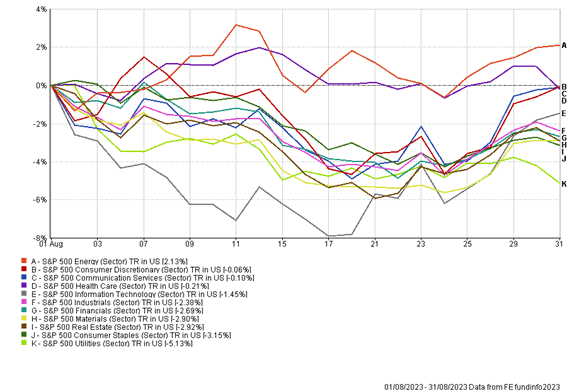

Some sectors (such as consumer staples) may be responding to these signs of future weakness, being one of the worst performing sectors in August, down 3.15%. The worst performer is the Utilities sector, which down 5.13%. It is important not to mis-read the causes, however, since the utilities sector is also likely reacting to future legislation on carbon emissions imposed by the government. The consumer staples sector mostly comprises large retailers such as Walmart and Costco, both of which have stated that they are surprised by the resilience of consumer spending in their latest earnings calls.

YTD performance of selected US stock market sectors

Jay Powell and the Federal Reserve have been relatively quiet since our last commentary, not wanting to spook markets at their annual Jackson Hole economic symposium.

The main takeaways from this event were that economic growth is running hot, inflation is still above their 2% target, and the tight labour market is not showing signs of weakening (not exactly breaking news!). In line with market expectations, there were indications that policymakers do see further interest rate hikes as being necessary to achieve their inflation target.

Although the Fed officials may say otherwise, markets are pricing in a 58% chance of no more rate hikes for the rest of the year, with a 35% chance of another 25 basis points. When looking at the longer-term data on the CME FedWatch Tool, the consensus suggests that current rates will likely remain until the middle of next year, then 1% lower by the end of 2024.

The US yield curve steepened in August, with 10-year yields rising from 4.03% to a peak of 4.34%, whilst the 2-year yield remained flat at around 4.97%. This move is referred to as a “bear steepening”, where investors extend their time horizon and take a bet that higher rates will no longer hurt the economy. This is backed up by the trend of hedge funds becoming bearish on US Treasuries. Short positions on 10-year bonds are at the highest level since the beginning of July. By predicting that bond prices will fall, these investors believe that yields will rise further (as prices and yields move inversely).

For anyone unfamiliar with short-selling, or “shorting”, an investor who believes a certain investment will fall will borrow those investments from another investor at a given price, and then immediately sell them into the market. If they are correct, they can then buy the assets back at a lower price in the future and give them back to the original owner, pocketing a return on the difference.

The main risk in selling short is that the price moves in the opposite direction, forcing the investor to buy back at a higher price to “cover” their short and return the asset to the original owner. Upward momentum can then build, causing the asset price to go even higher. This is known as a “short squeeze”. Given that prices can rise indefinitely, potential losses on a short position can be unlimited – making this position extremely risky.

One factor that we believe is being ignored by investors is the increasing default rates in US high yield bonds. As the cost of credit rises, companies are increasingly looking to secure their debt on company assets in order to make financing more affordable. Over $70 billion worth of junk bonds issued in 2023 have been secured on various company assets, with rates averaging 8.50%, compared to 4.50% in 2021. This could spell trouble as we have already seen $26 billion worth of defaulted debt this year, well over the $18 billion that was defaulted on in 2022.

US markets may continue their excellent performance into the second half of 2023, but the challenges we have outlined above should not be overlooked. Whether or not there will be a US recession has been the question of the year for investors – in our opinion, the lag effects of higher rates mean a recession is likely. A more important question then becomes how deep or long lasting a recession will be.

China

China has taken centre stage in August as a numerous pieces of worrying news surface. Deflation, weak exports, lower than expected GDP growth, higher than expected unemployment, and gloomy updates from the property sector (to name a few!) have all contributed to unfavourable investor sentiment surrounding the largest emerging country.

Is this the start of a global slowdown as contagion spreads from the world’s largest exporter? Or has the Chinese economy put in a bottom from which it can bounce upwards? Reversion to the mean is a common feature of financial markets, which would lend itself to the worst already being behind us. We have however seen many “perfect entry points” for investing in China over the past two years, none of which have resulted in good medium-term performance.

YTD performance of Chinese indices

In the month of August, the Shanghai Stock Exchange Composite dropped 6.15%, whilst the Hang Seng lost 7.83%. In a year when most major markets are performing well, China has struggled to participate. From their January peak, on the back of optimism surrounding the abandonment of their “zero-Covid” lockdowns, markets are now over 20% lower.

Value investors may be sniffing out a contrarian opportunity. However, a large measure of caution must be applied when investing in China. As always, Chinese markets are unpredictable, especially from the West, where access to information is a lot less restricted. Not to mention the potential downside we could see if any conflict materialised in Taiwan.

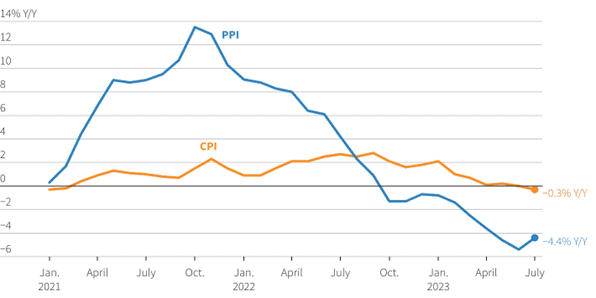

The most notable development that came out of China in August was the monthly inflation data, which currently indicates deflation. The Consumer Price Index fell 0.3% from a year ago in July and the more forward looking Producer Price Index fell by 4.4%.

Chinese Consumer Price Index and Producer Price Index from January 2021. Source: Reuters

Whilst the rest of the world is battling the severe consequences of inflation, you may wonder “why is deflation such a bad thing?” It may be argued that if prices rising is bad, then prices falling must be good. Not exactly, and some economists would insist that it is a lot worse. It all comes down to the time value of money.

The time value of money suggests that £100 in your hand now is worth more than £100 in your hand in a years’ time because of the opportunity for it to earn interest in the interim. This principle incentivises you to go out and spend this money or lend it out in return for interest, both of which contribute to positive economic activity. However, if you knew that that same £100 would be able to buy more in a years’ time than it does now, you would be incentivised to put it in a shoe box until then, not contributing any economic activity.

China’s economic miracle of the last few decades has been based on high exports and low unemployment, providing cheap goods for the rest of the world. However, even these two crucial components look worrisome. July exports declined a whopping 14.5% from a year ago, albeit there will be some distortions because of Covid restrictions in 2022. As a result, GDP expanded just 0.8% in Q2, well short of Beijing’s annual target of 5%.

The Chinese government also announced that the overall unemployment rate had risen to 5.3% in July. The main takeaway from this release was actually that they stopped publishing the youth (16-24 year olds) unemployment rate after it hit a record high of over 20% in June. This poses the question, what other information may investors not have access to?

The final development that we will cover in this section involves the ongoing real estate crisis. Chinese property giants, Evergrande and Country Garden, have been facing huge financial difficulties this year, which has been spilling over into the wider economy. Evergrande filed for Chapter 15 bankruptcy in August after defaulting on its debt obligations in 2021. Country Garden narrowly avoided this fate after paying $22.5 million in bond coupon payments.

In response to all the problems outlined above, the Chinese government has taken multiple steps in order to provide help. To support the property market, the Peoples’s Bank of China has eased borrowing rules and cut the reserve requirement ratio for foreign exchange deposits from 6% to 4%. And to support the wider economy, it has lowered the one-year loan prime rate 10 basis points to 3.45%. Most household and business loans are attached to this rate, so this should help to improve the troubles they are facing. Whether this will be enough remains to be seen, but investors are currently not convinced.

Again, this highlights the short-term volatility in any investment in China and the long-term time horizon (and patience!) needed. Last year we spoke about long-term potential growth drivers for China, with one of those being a shift in income equality as more consumers move from the lower income bracket into the middle-income bracket. The effect of this will be borne out over years and decades, however, because it is a long-term process – presently, investors are having to focus much more on the short-term news.

Robert Dougherty, Associate IFA

Ryan Carmedy, Graduate Trainee IFA

Harry Downing, Graduate Trainee IFA

September 2023

This article is not a recommendation to invest and should not be construed as advice. The value of an

investment can go down as well as up, and you may get less back than you invested.