Global bond yields have risen from historic lows over the last three years and currently remain elevated despite falling inflation and central banks cutting interest rates. These elevated levels are largely down to sticky inflation and policy uncertainty (which increases the “term premium”, or the additional return demanded by investors for investing in longer-dated bonds, to compensate for the fact that interest rates might change).

Yields had begun to fall from June 2024 onwards but later picked back up in August as inflation remained elevated and Central Bank rhetoric on interest rates moved to “higher for longer”.

UK Gilts

In the UK, we have seen Gilt yields pick up from their lows back in June 2024, driven more by fears of what may happen rather than the fundamentals of the UK economy.

1 year change in 2 & 10 year Uk Gilt yields. Blue line represents 10 year Gilt and black line represents 2 year Gilt (Source – MarketWatch.com)

US government bonds are known as treasuries, and generally when US treasury yields rise, this has an impact on other countries’ bond yields.

UK-specific problems have impacted bond yields here as well, in particular the Labour government approaching its self-imposed borrowing limits before any real investment in the economy has been made. Investors remain cautious and want to see whether government borrowing will increase or whether further tax rises will be implemented.

With the UK economy struggling, the Bank of England may well cut rates by more than the market expects in order to boost the economy (as indicated by two voting members of the Monetary Policy Committee opting for a 0.50% ‘jumbo’ rate cute at their last meeting). While returns cannot be guaranteed, Gilt yields do look attractively priced and in our view the upside risks outweigh the downside risks.

Government bonds are issued with varying terms; some have repayment dates much further into the future (30 years, for example) and some are repaid much sooner, say two years. Bonds with different maturities react differently to interest rate cuts, with the value of longer-dated bonds more sensitive to movements in rates (both up and down).

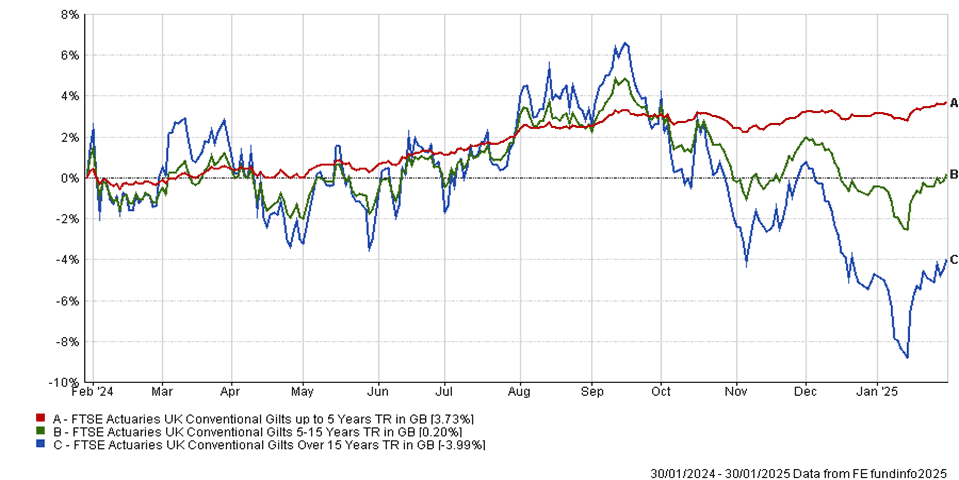

Shorter-duration bonds currently offer a reasonable yield and income, and this is preferred to protect against any increases in the term premium due to further fiscal uncertainty. As we can see in the chart below, shorter maturity bonds have delivered a positive return with less volatility over the last year relative to longer dated bonds.

An uptick in inflation is still a risk and would present the UK economy with the problem of stagflation (low growth and high inflation), where cutting interest rates would not solve the problem. Therefore we remain cautious on the UK economic outlook.

1 year performance of UK Gilts with different maturities (Source – FE Analytics)

US Treasuries

Over the Atlantic, US government bonds are presently held at neutral weightings or are underweight in portfolios. Long-term bonds (which as mentioned, carry a higher interest rate sensitivity) are most susceptible to the ongoing debt problem in the US and political/trade fragmentation.

The term premium, which is the premium investors demand for holding longer dated bonds, has picked up over the last three years. We expect this to increase further in the US further due to the increased uncertainty around the new Trump administration’s economic policies.

Although tariffs are increasing and this may bring in extra revenue, coupled with potential tax cuts, the net result is likely to be a deficit and this will require additional government borrowing. At regular intervals the US approaches its “debt ceiling” (the borrowing limit imposed by law) and a vote is passed to increase this further. Until interest rates are lower than GDP growth, we will keep seeing this deficit widen. Debt cannot keep growing forever and so investors remain vigilant to the impact of President Trump’s policies on the government deficit.

Again, due to their reduced sensitivity to interest rates, shorter dated bonds are preferred in the US. With fewer interest rate cuts expected this year, the uplift in capital values that longer dated bonds would receive from these cuts is not likely to be big enough to offset the risk we see.

High yield bonds

One category of bonds which has performed well over the last two years is the global high yield bond sector. These bonds are loans to companies which have lower credit ratings, and the main factor to consider with high yield bonds is the credit risk.

As high yield bond issuers have lower credit ratings are there is a greater risk that they will default on their payments relative to companies with higher credit ratings and developed government bonds. Risk has to be rewarded, and in return for the greater risk of default these bonds have a higher yield and coupon (interest) payment. High yield bonds typically have shorter maturities and are refinanced more frequently. They also have floating coupon rates – that is, their coupons fluctuate in line with the general level of interest rates.

Global high yield bonds have performed very well in the last two years owing to their lower sensitivity to movements in interest rates. As yields have increased across the board, high yielding bonds have produced attractive returns, with their high coupon payments offsetting any capital losses from interest rate increases. Actual default rates have remained low and so credit risk has helped to drive these returns.

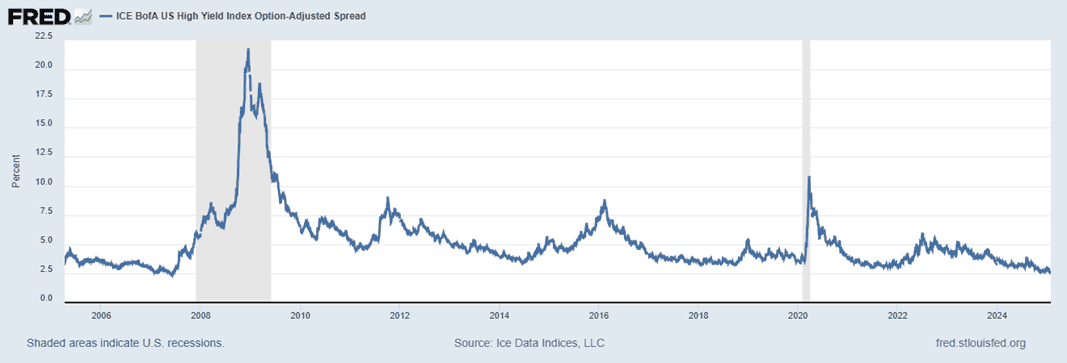

In the US the spread (or difference) between safer Treasury bond yields and riskier high yield bond yields is narrow (highlighting that investors are demanding a smaller premium for holding bonds with higher credit risk), presently sitting just above 2.6% (see chart below).

High yield bond spreads (Source – Federal Reserve Bank of St Louis & ICE BOFA Indices)

Therefore a big risk for US high yield bonds is this spread widening. This would happen when investors’ perceptions of credit risk increases, i.e. the risk of corporate defaults increases and/or economic growth deteriorates.

While the latter looks unlikely in the US (although the probability is increasing with the threat of a trade war) as economic growth remains strong, with the Federal Reserve holding interest rates higher for longer the cumulative effects on more indebted and struggling companies takes a greater toll.

Therefore, we could see spreads widening if rates stay high for too long. The relative attractiveness of the high income and lower interest rate sensitivity available from the high yield sector has continued to attract investors, but we remain cautious over credit risk.

UK high yield bonds could also see an increase in yield with the National Insurance tax hikes increasing the burden on smaller companies and consumer sentiment remaining low. European high yield bonds provide an attractive income but again, with many European economies forecast to struggle this year, defaults may well pick up.

That said, interest rates are lower in the EU and so the financial burden is not as great, resulting in European high yield bonds being preferred by investors at this time.

Investment Grade Bonds

Investment grade credit (bonds issued by companies with the highest credit ratings) is also susceptible to changes in credit risk. With the spread on yields of BBB-rated debt being very tight to US treasuries (approximately 1%) these bonds are also at risk of a spread widening.

In the last month there has not been a large supply of newly issued corporate bonds, but where there were new issues, these were oversubscribed, highlighting high investor demand.

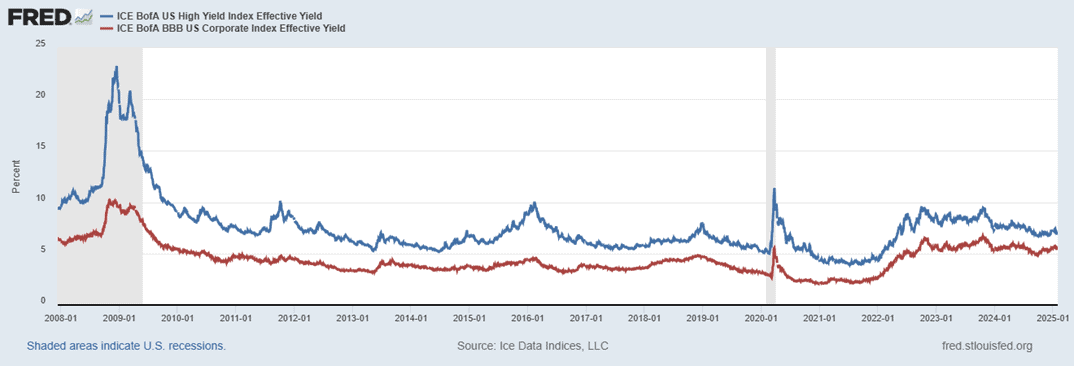

Effective yield of high yield US bonds versus BBB Investment Grade US bonds (Source – Federal Reserve Bank of St Louis & ICE BOFA Indices)

Investors are preferring high yield bonds over investment grade bonds for their greater yield (averaging 6.96% for high yield and 5.49% for investment grade BBB, as at 31/01/2025) but we do not think this anticipates the potential increase in credit risk from weaker economies and rates staying higher for longer.

A large proportion of high yield debt is rated BB, which is the highest rating assigned to high yield debt. Investors just do not see much risk in this category as balance sheets are strong and the interest coverage (how many times earnings covers interest payable) is acceptable.

Although there are many more bond sectors (Emerging market local and hard currency, convertibles, asset back securities) which we could discuss for hours, hopefully this article has highlighted how different bonds perform in different environments and reinforced the message that staying nimble, active and diversified is the best approach in a volatile macro environment.

We also see a risk from bonds in the form of private credit, which is expected to take a greater proportion of lending as governments debt burdens are stretched further.

Data from Vanguard shows that in 2021 the probability of a positive return on global fixed interest was 43%. That figure is now 88%, highlighting how bonds are expected to generate positive returns going forward. The income they generate is certainly higher than in 2021 and any increases in interest rates will result in a lower capital loss, as rates would be starting from a much higher base.

Robert Dougherty, Investment Specialist

February 2025

This article is not a recommendation to invest and should not be construed as advice. The value of an investment can go down as well as up, and you may get less back than you invested.