Trump seems to be accepting of this, as shown by his recent post on social media ‘Will there be some pain? Yes, maybe (and maybe not!)’, and we have already seen some of this short-term pain in markets.

I have rewritten this opening introduction more times than I can count due to the constant barrage of policy changes from the US administration. This constant flux and change of political direction reflects exactly what we are seeing in markets, with very high short-term volatility being the reaction to uncertainty – a feature rather than a flaw of markets.

Rather than finishing this introduction with the summarising conclusion, starting with it will help to keep all of the recent volatility and market movements in context. This is that periods of uncertainty like the present require investment discipline, and sticking to a long-term investment strategy remains key.

Attempting to predict what Trump may do next and therefore what how markets will react is a futile exercise. Timing the market has never worked and this remains true today. Macro and political movements and motives are a short-term veil over what matters for investments, and that is which companies will grow their earnings and generate value over the long-term. Our view of this has not changed.

Over the weekend we saw Trump using his powers under the International Emergency Economic Powers Act to impose emergency tariffs on Canada and Mexico, with the EU and other countries also under threat. Come Monday evening these tariffs had been put on hold.

While it may seem like all is done, we would not be surprised if in a months’ time tariffs are back on the table. Trump is playing a game of chicken with trade and markets are not happy.

The US implementing tariffs will be the first part of the tit-for-tat investors have been focusing on in the trade battles. Arguably, the more important part of this trade war will be the “tat”, i.e. how other countries will respond to the US. Canada has already imposed its own tariffs on US exports to the country, with Mexico also planning retaliation.

Stocks dropped on this news and the US Dollar rose to one-year highs. Prior to this move the US Dollar was already 10% over-valued relative to fundamentals.

The UK may well avoid the threat of tariffs as the US has a trade surplus with the UK (the UK imports more from the US than it exports to them). Trump has already said trade issues are out of line with the UK, but can be worked out.

Another big focus of Trump so far has been deportation of immigrants. While this will likely not have an immediate impact on markets, the longer-term effects may have some material impact on US economic growth (given that over the past 5 years immigration accounted for 88% of the growth in the US labour force). It is also highly unlikely Trump will be able to deport the number of people he wishes due to the cost and logistics of this operation.

Research has shown that combined with Trump’s potential tax cuts, the revenue raised from tariffs will not compensate for the reduced tax revenue and will create a wider budget deficit in the US.

Threats to China have also started to materialise, with Trump imposing 10% tariffs on top of existing Chinese tariffs. China have responded in kind with its own tariffs and restrictions on the export of critical minerals.

US economic growth was strong for 2024, if slightly below expectations. We continue to monitor Trump’s policy actions and how these may affect US growth for the rest of the year.

In other news we saw a big and rather overblown shake up in the technology and AI sector with the news that the Chinese start-up DeepSeek had developed an AI model comparable with US models for a fraction of the cost.

This caused ripples throughout markets and especially anything AI-related, be it energy companies, tech companies or infrastructure companies. We have seen some recoveries in many of these companies and believe that this volatility was largely an overreaction.

Investors react to bad news with a significantly greater magnitude than they react to good news, and lots of investors used this brief downturn as a good opportunity for profit-taking. That said, the common question as to whether US equities are overvalued is again up for debate.

Closer to home, the UK government has realised how big a task it has on its hands with economic growth and consumer confidence dwindling at low levels. Relative to the US, UK productivity is much lower and with the Labour government already near its self-imposed borrowing limits, it remains to be seen how the proposed growth will be generated. Economists have forecast positive GDP growth for the UK this year, above that of Europe but below that of the US.

European growth remained positive but sluggish in 2024 and we continue to see major headwinds for the bloc. Equities had mostly remained positive as Trump has not yet imposed any tariffs on European exports to the US, but since this weekend the threat of tariffs has caused markets to fall.

Areas of focus

We remain vigilant on high yield bonds due to slowly increasing defaults and the longer-term pressure of higher rates on balance sheets.

AI-related companies remain at elevated volatility levels and this is likely to continue throughout the year.

The Magnificent Seven valuations are very high, but much of this price growth is explained by their earnings growth (excluding Tesla).

Deregulation in the US looks to provide a tailwind for financial companies to increase their operations and dealmaking.

Carmakers, capital goods and consumer discretionary stocks will feel the brunt of the US trade war.

UK smaller companies remain underweight until a catalyst for change reenergises the sector. US smaller companies on the other hand look to continue their positive performance as returns in the US broaden out.

Indian equities have had a difficult few months with short term concerns over valuations. The long-term outlook remains positive with the defence sector in particular well placed for returns.

Bonds are forecast to deliver good returns this year as their yield remains attractive and any increases in yield (falls in price) will be offset by the higher coupon interest they are paying.

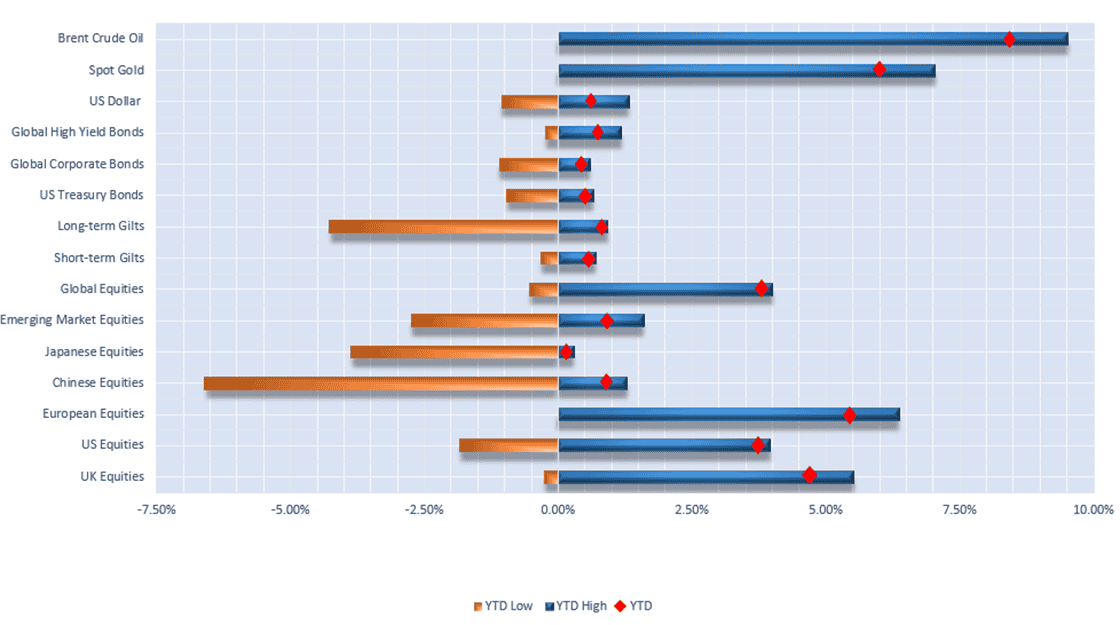

Selection of assets 2025 YTD returns and range of returns as at 03/02/2025 (the two ends of the bars represent the range of YTD returns and the red dots represent the current YTD return). Indexes used: FTSE All-Share, Russell 2000, STOXX Europe 600, MSCI China, MSCI Japan, MSCI Emerging Markets, FTSE UK Conventional Up To 5 Years, FTSE UK Conventional Over 15 Years, ICE BOFA US Treasury, ICE BOFA Global High Yield, ICE BOFA Global Corporate, US Dollar Index, S&P GSCI Gold Spot, S&P GSCI Brent Crude Spot. Returns hedged back to GBP with exception of US Dollar which is in US Dollar terms. Data from FE Analytics and MarketWatch.

US

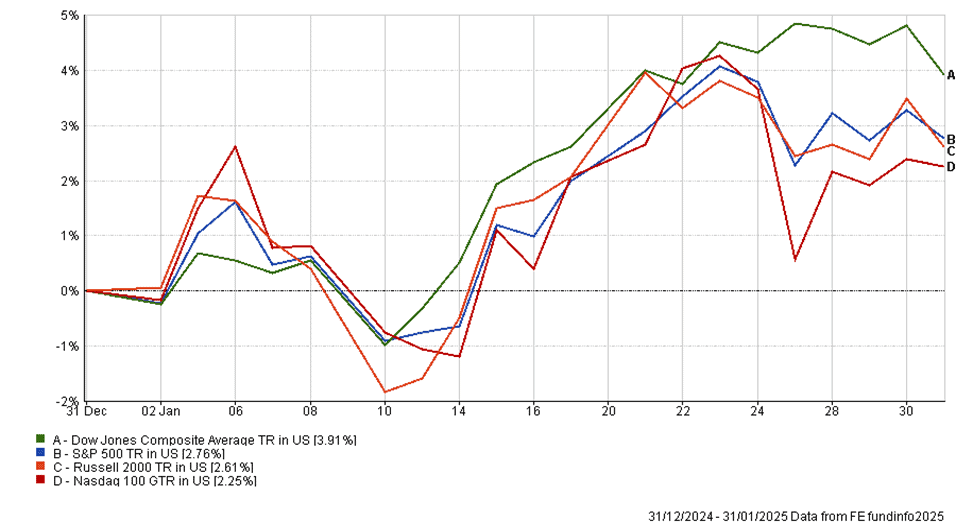

US equity markets started 2025 positively but not without some bumps along the way. The four most well-known stock market indices rose between 2% and 4% in January, with the more traditional Dow Jones Composite Average posting the largest gain (3.91%) and the tech-heavy Nasdaq 100 posting the smallest increase (2.25%).

Two such “bumps” came in the form of a new Chinese Artificial Intelligence (AI) model, DeepSeek, that is claimed to have been developed at a fraction of the cost of its US rivals, and tariff announcements from the newly inaugurated President Trump.

Equity markets are also in the process of digesting Q4 2024 earnings reports. According to Factset, S&P 500 companies are reporting mixed results relative to expectations.

About a third companies have reported so far, and 77% of those companies reported Earnings per Share (EPS) above estimates. This is marginally above the 10-year average of 75%. In aggregate, these companies are reporting earnings that are 5% above expectations, which is below the 10-year average of 6.7%.

Of the four Magnificent Seven companies that have reported, Microsoft, Meta, and Apple have beaten the consensus expectations, whereas Tesla missed. However, there are concerns in certain areas of these businesses, with Microsoft having missed expectations in its cloud computing division due to an inability to meet the huge demand.

Alphabet, Amazon, and Nvidia are yet to report.

YTD performance of US equity indices (Source – FE Analytics)

Nvidia has experienced significant volatility this month even before its much-anticipated earnings release due to the development of a new AI model in China (DeepSeek). Although Nvidia does not directly compete with DeepSeek when it comes to developing artificial intelligence models, which is more the arena of Alphabet and Meta, they were the biggest loser on the news. In fact, they were the biggest loser in stock market history, shedding nearly $600 billion in company value in just one trading day.

The reason for the decline was that DeepSeek claimed that it developed its “R1” AI model for less than $6 million, which is a fraction of the $540 million OpenAI spent to develop its first ChatGPT model in 2022.

This means that demand for Nvidia’s specialised chips may be reduced significantly, with Graphics Processing Units (GPUs) being a major input for AI training. There has been some speculation that the Chinese may be underreporting the actual cost of training or copying a more developed US model during development, however. The rise of AI has been the key driver of US equity market returns in the last couple of years so this will be a topic investors will be watching closely – however, it is worth noting that in the longer term, access to cheaper and more readily-available AI technology could increase profitability across a much wider range of businesses and sectors in the economy.

Trump also announced his long-anticipated tariffs on the last day of January with a 10% tariff being placed on Chinese imports and a 25% tariff being placed on imports from Canada and Mexico.

These tariffs came into effect from February 1st and markets dropped slightly on the news. Demonstrating the unpredictability of this administration, the tariffs for Mexico and Canada were then suspended for a month after Mexican President Claudia Sheinbaum and Canadian Prime Minister Justin Trudeau both agreed to send 10,000 troops to their borders to combat drug trafficking. Given such a constructive conversation is less likely between the US and China, its President Xi Jinping instead retaliated with tariffs of his own on US imports.

Whilst Trump insists that these tariffs are to shift the tax burden from US taxpayers onto foreign countries, the above is further evidence that Trump uses them as a bargaining tool to negotiate favourable deals. We have also seen him use this tactic against Colombia as it refused to take in his first wave of deportations, but swiftly accepted once threatened with a tariff of 50% if they did not comply within a week.

Investors have interpreted this as meaning higher inflation and therefore higher-for-longer interest rates. The rationale is that the cost of tariffs will be passed onto US consumers in the form of higher prices and/or more goods will be made and sold domestically, with the idea that if offshoring is deflationary, onshoring must be inflationary.

That said, research indicates that tariffs act to increase prices rather than inflation. This is because the application of a tariff is a one-off price rise, which increases inflation at that time – but if the price does not increase further, the inflationary effect eventually falls back to zero.

If inflation is higher, the Fed will be forced to keep rates higher to combat it. Inflation rose to 2.90% in December in line with expectations but up from the 2.70% print from the prior month. This is still above the Federal Reserve’s 2% inflation target.

Jerome Powell left rates unchanged at between 4.25% and 4.50% during the January Federal Open Markets Committee (FOMC) meeting, citing that inflation remains somewhat elevated.

The CME FedWatch tool now expects the first cut of the year to come in June and the two-year treasury yield now also sits at 4.25% with the ten-year yielding 4.52%. This marks a stark difference from the rates investors were pricing in six months ago, when both the two and ten-year yields were below 4%.

The dollar is also trading at levels not seen since 2022 for similar reasons. A stronger dollar can have severe consequences including a higher debt burden on dollar-denominated debt (common in emerging markets), lower commodity demand (as most commodities are priced in dollars), and foreign earnings for US companies being worth less in dollar terms.

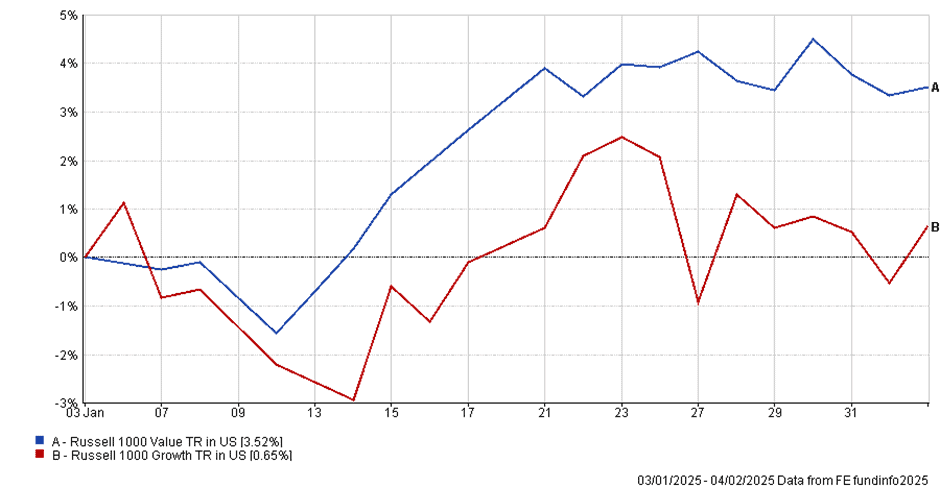

While growth stocks have outperformed value stocks over 2024, so far this year we have seen value stocks outperforming. As mentioned, the elevated values of growth companies and the potential future impact on their earnings from Trump policy actions has caused them to suffer this month.

It is worth remembering however that over the last ten years value stocks have returned just 122% relative to 363% for growth-focussed companies, and so this may not be a change in which types of companies will benefit going forward. One caveat is that for most of the 20th century value had outperformed growth, so whether we see a reversion to the normal or not remains to be seen.

YTD performance of growth & value US equity indices (Source – FE Analytics)

Europe

The Eurozone has had a relatively optimistic start to 2025, despite ongoing political instability, trade uncertainty and an ongoing conflict in Ukraine. Investors had originally anticipated Trump would impose tariffs on the EU immediately upon entering office, but this has not yet transpired.

Investors pre-emptively took this as a sign that tariffs would not impact the EU and we saw a swift rise in European equity markets. Combined with a depreciating exchange rate with the US Dollar (as interest rates in the US are forecast to stay higher while the ECB deposit rate continues to fall) this led European markets to outperform the S&P 500 in January.

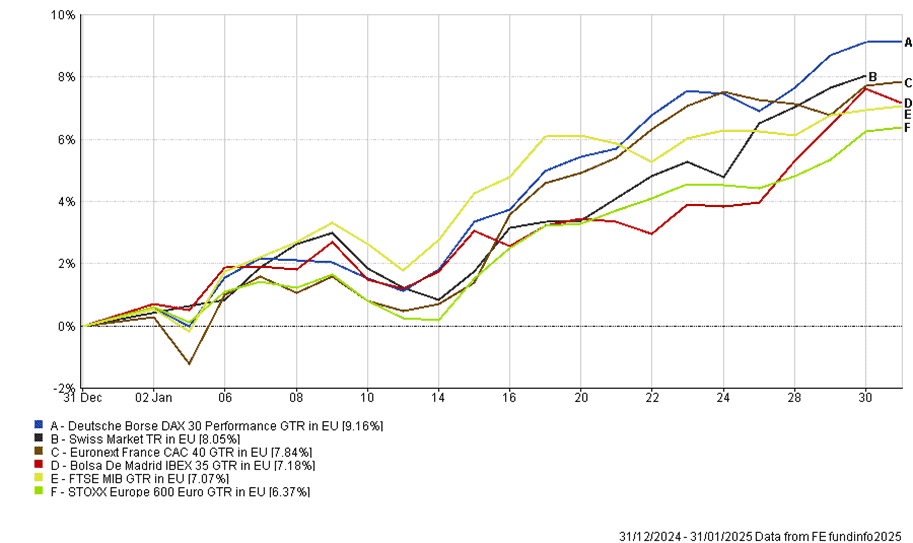

YTD return of major European stock market indices, returns denominated in EUR (Source – FE Analytics)

The STOXX 600 rose 5.65% and this represents its best monthly performance in over a year. The German DAX 40 index also initially performed well, increasing 8.53% in the last month.

Another tailwind for European stocks was the sell-off in US technology companies and other AI-related companies (following the announcement of Chinese start-up DeepSeek AI), with investors looking elsewhere to diversify their holdings.

This particularly benefited the EU as its AI technology companies have fallen behind their US counterparts in terms of development and capital expenditure. DeepSeek showed that AI does not need billions of dollars of capital to develop (although this is much debated) and as the EU’s companies have fallen behind, this should give them a boost to improve their offerings.

To gain investor’s confidence once again the Eurozone will need to combat the ongoing challenge of faltering growth. GDP figures released for the fourth quarter of 2024 showed static growth across the Euro area since the previous quarter, exacerbated by contractions in both Germany, France and Ireland (although Spain did grow by 0.8%).

The European Commission revealed its Competitiveness Compass on 29 January 2025 – a new framework which proposes developments in Artificial Intelligence and technology as a route to a more competitive European Union, whilst noting the importance of EU single market consolidation in ‘a world of giants,’ as well as maintaining open trade relationships with other countries.

Christine Lagarde (President of the ECB) and Ursula von der Leyen (President of the European Commission) are pushing for the EU to remain competitive by making the EU better for innovative companies to grow, making Europe a better place to invest and making it cheaper to do business in Europe.

The advent of cheaper AI along with these proposals could help to achieve these aims. As European companies trade at a big discount to the US in the longer term this could attract investors to the region if the EU can deliver on its goals.

One area in which Europe can develop a technological advantage is clean energy. Europe has been working hard to wean itself off of Russian energy since the start of the Ukraine conflict and to become 100% reliant on clean energy. With Trump pulling back tax credits and making the US less attractive for renewable energy (illustrated by another Trump quote, sorry – “drill, baby, drill”!), Europe has the opportunity to thrive in this area.

Speculation on tariffs has been a hot topic of conversation for many countries in recent months. Despite repeated warnings, Trump has not yet confirmed new tariffs on goods exported to the US from the Eurozone, which had initially helped the confidence of investors. From recent announcements it is very likely the EU may see a 10% tariff placed on its exports to the US.

Many European companies including the region’s second most valuable company, LVMH, have already started to move operations over to the US to appease President Trump and ensure they remain competitive. The biggest losers from potential tariffs will likely be car manufacturers and other discretionary consumer goods companies.

Combine these potential tariffs with the threat of competition from China and a struggling manufacturing sector in Germany and we see large headwinds ahead for the EU.

30th January saw the European Central Bank (ECB) cut interest rates by a further 0.25% to 2.75% in keeping with the general market expectation that interest rates will reach 2% by September. Inflation, as measure by the Harmonised Index of Consumer Price (HCIP) ended December 2024 at 2.4%, with the rate ticking up to 2.5% in January.

There is debate over whether the ECB has reached a critical period in which a shift in strategy is necessary. Some believe that the reactive, data-driven strategy has not yet successfully curbed the peak in inflation of 2022, and any further cuts may cause inflation to remain above the ECB’s 2% target. However, with economic growth weak it may be necessary to cut further. This will also be beneficial in helping government debt burdens and will make investment in the bloc cheaper for companies.

In terms of fixed income, if the ECB can sustain the predicted interest rate cuts this year this should provide a tailwind for bond prices. Ongoing geopolitical issues, regional fiscal problems and poor growth remain a challenge. This has not discouraged investors as although yields rose and prices fell early in the month, perhaps reflecting anxiety with regards to funding requirements approaching Trump’s inauguration, demand for bond sales in January exceeded supply by at least ten-fold.

Unlike other major economies, the EU’s debt load is not as high as the US or the UK, giving it more room to use debt to invest in the infrastructure and investment needed to remain competitive.

Provided the EU can make it an easier place to do business, over the long term we may see increased investment opportunities here. Presently though, struggling economies and political uncertainty are deterring investors from increasing their allocations.

UK

The main measure for inflation in the UK, CPI, fell by 10 basis points in December to 2.5%. Core CPI and the CPI services annual rate also fell month-on-month, with core CPI now at its lowest rate since March 2022.

All measures of inflation fell below consensus expectations, and provided investors with hope that interest rates will fall in the short term.

The Bank of England’s Monetary Policy Committee met on Thursday 6th February. Markets were pricing in a 90% probability of an interest rate cut, so the decision to reduce rates from 4.75% to 4.5% came as no surprise. On this news, the pound depreciated against the dollar and pushed the FTSE 100 to new all-time highs (as the majority of FTSE 100 company earnings come from overseas, so any weakening in the pound increases their earnings when they convert back from foreign currency to pound sterling).

This 25 basis point cut marks the third reduction in rates since the peak in the summer of 2023. The cut to base rates was not unnaimously decided, with two of the nine voting members opting to reduce rates by 50 basis points – and interestingly, one of the two advocates for a larger cut was an MPC member who had previously been considered hawkish on rates.

The majority of investors now see at least three quarter-point reductions by the end of this year, but lower UK GDP growth may increase the amount to cuts to five or six.

On that point, the outlook for UK economic growth in 2025 has (once again) been downgraded. The country’s spending watchdog, the Office for Budget Resposibility, now expects GDP growth to be around 1.3% this year, down from its previous forecast of 2%.

The key source of uncertainty in the UK still remains Labour’s recent Budget, especially the decision to raise employers’ NI contributions by £25 billion overall. Economists believe that this decision will increase unemployment, dent business confidence and ultimately limit growth.

To counter this malaise, the UK government are contemplating different options to spur on growth in the economy. One option that Rachel Reeves is considering is to scale back tax breaks for cash ISAs. There is approximately £300bn in cash ISAs and it is thought that UK equities would benefit if this capital was instead invested.

According to Nationwide, house price growth slowed more than expected in January, rising only 0.1% month-on-month. This recent increase means that the average home in the UK now costs £268,213.

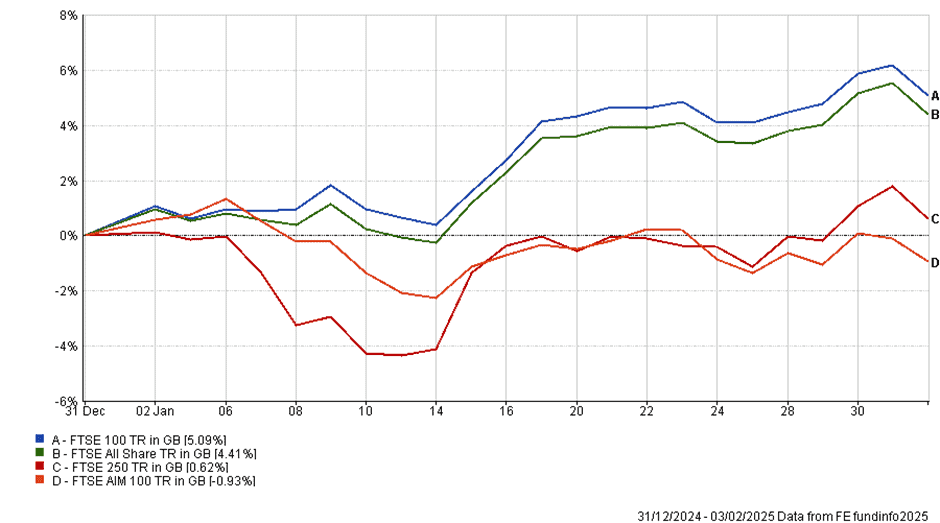

YTD performance of major UK stock market indices (source – FE Analytics)

In the equity markets, the FTSE 100 index reached all-time highs in January as it has the best month in more than two years – climbing over 6% in the month.

Whilst not having technology companies has hindered the performance of UK stock markets over the longer term, the recent move away from US AI stocks into more traditional stocks pushed the FTSE 100 higher in January, after DeepSeek raised questions about the costs involved in the creation of AI models. If this trend continues, relatively undervalued companies in the UK and Europe may start to outperform.

Smaller companies, represented by the FTSE AIM 100, did not witness the same increase in price and fell by almost 1% over the month. With interest rates still high, there are concerns over the ability of smaller companies to pass on the heightened costs of increasing minimum wage and employer NIC payments.

The gains last month can also be largely explained by Donald Trump’s decision to delay the implementation of his aggressive tariffs.

Towards the end of the month, UK markets experienced heightened volatility due to escalating trade tensions between the US, Mexico, Canada and China. This led to the FTSE 100 reducing by over 1% that a day, with more trade sensitive sectors falling further.

Movements in the gilt market also made the news in early January, with UK government bonds experiencing a significant selloff and 10-year gilt yields reaching 4.9% – the highest level since 2008. Yields on longer dated 30-year gilts increased to the highest levels since 1998. Although ten-year gilt yields have dropped slightly to 4.5%, they are still significantly higher than pre-Budget levels.

There are several reasons for this recent increase in gilt yields. Inflation remains higher than the Bank of England’s 2% target, economic growth is lagging, and the additional cost of employer NI contribution is raising questions on UK businesses’ ability to employ and reinvest. However, it is worth noting that much of the rise was actually a reaction to higher yields on US government bonds and as such, had little to do with the UK’s public finances.

Nonetheless, this recent increase in gilt yields has placed increased pressure on Rachel Reeves, with increased borrowing costs eroding her £9.9bn of fiscal headroom down to just £3 billion by the end of this parliament, the smallest on record for any Chancellor.

Falling interest rates may provide Reeves with some relief in the short term. However, growing fiscal worries has increased speculation that further tax rises and/or spending cuts may be unavoidable.

Robert Dougherty, Investment Specialist

Ryan Carmedy, Associate IFA

Harry Downing, Associate IFA

Fiona Chegwidden, Graduate Trainee IFA

February 2025

This article is not a recommendation to invest and should not be construed as advice. The value of an investment can go down as well as up, and you may get less back than you invested.