This momentum carried through to other markets and we saw a broadening-out of positive returns as investors leaned into riskier assets once again.

Towards the end of 2024, we saw former and now President-elect Trump voted in as US president and for the majority of the remaining two months of the year this resulted in positive performance, as his stance on deregulation and tax cuts gave investors optimism for 2025.

We did see a setback towards the end of December, with bond yields rising and stocks prices drifting lower as inflation expectations became anchored at higher levels in response to Trump’s tariff threats.

Despite the positives of AI and deregulation, all of this took place behind the veil of the interest rate dilemma which is likely to continue to play out over the next few years.

Unfortunately this meant we did not see the “Santa Claus” rally discussed in our last asset commentary.

Throughout a volatile 2024, interest rates have begun to decrease and inflation fell back towards central bank targets. However, there are signs that inflation is again picking back up, prompting the US Federal Reserve to rethink how many interest rate cuts there may be next year.

The main features of 2024 were:

- Central banks cut interest rates, with the Bank of England base rate ending the year at 4.75%, the European Central Bank deposit rate ending at 3.00% and the US Federal Reserve funds target rate ending at 4.25 – 4.5%.

- Global inflation rates trended back towards central bank targets but showed signs of potentially sticking at higher levels towards the end of the year.

- UK CPI was recorded at 2.6% in November (with CPIH, including housing costs, being 3.5%). US inflation came in at 2.7% (core inflation, the Fed’s preferred measure, being 3.3%) and the Euro area inflation rate was 2.4% for December, all above central banks’ 2% targets.

- Equities fell and bond yields rose towards their one-year highs at the end of December as inflation had picked up in November and the US Fed suggested fewer rate cuts are likely in 2025 than investors had priced in.

- President Trump was elected as the next US president and promised a barrage of tariffs on other countries, as well as tax cuts, deregulation, mass deportation of immigrants and a clean-up of the US government. Certain areas of his agenda such as deregulation pushed markets higher, with cryptocurrencies being a big winner for a short period (before falling back again), but the potential for large tariffs on imports may well be inflationary.

- AI continued to propel equity markets higher, with the big tech companies returning huge numbers (Nvidia shares returned 176% in 2024). Similar to 2023, the S&P 500 outperformed the equally-weighted version of the index by 12.35% in USD terms, highlighting how the biggest companies continued to have an outsized influence on the index.

- The Israel and Ukraine conflicts continued throughout the year but did not have much effect on equity markets or investor sentiment.

- Chinese equities had a very volatile year. The Chinese government has stepped up its intervention measures, but investors are doubting whether this will be enough to prop up the struggling economy. The biggest risk faced by China is a Japan-style period of prolonged deflation.

- Japanese equities continued to perform well and aside from the US, in local currency terms were the best performing developed market equity as at November 2024. The unwinding of the Japanese Yen carry trade (where investors borrow money in Japanese Yen where interest rates are much lower, in order to invest in higher yielding assets elsewhere) rocked the market in August but was followed by a swift recovery.

- Annualised UK economic growth is expected to be sluggish for 2024 and the new Chancellor’s budget has done little to help this. The UK continued to face an exodus of equity listings, with many companies choosing to re-list overseas in order to benefit from a higher valuation. The UK has lacked the depth of the US market, certainly in terms of technology companies.

- European equities picked up a little in 2024 but political uncertainty added volatility to the markets, with France being the notable recipient. Investors also questioned whether the ECB has fallen behind the inflation curve and amid a time of struggling economic growth, the outlook has not been bright for the bloc.

Gold continued to see strong returns in 2024 with several factors providing strong tailwinds. Falling interest rates lowers the opportunity cost of holding gold (as gold is a non-yielding asset, higher interest rates make it less attractive to hold). Global central banks have also increased their reserves of gold in response to the US sanctions on Russia.

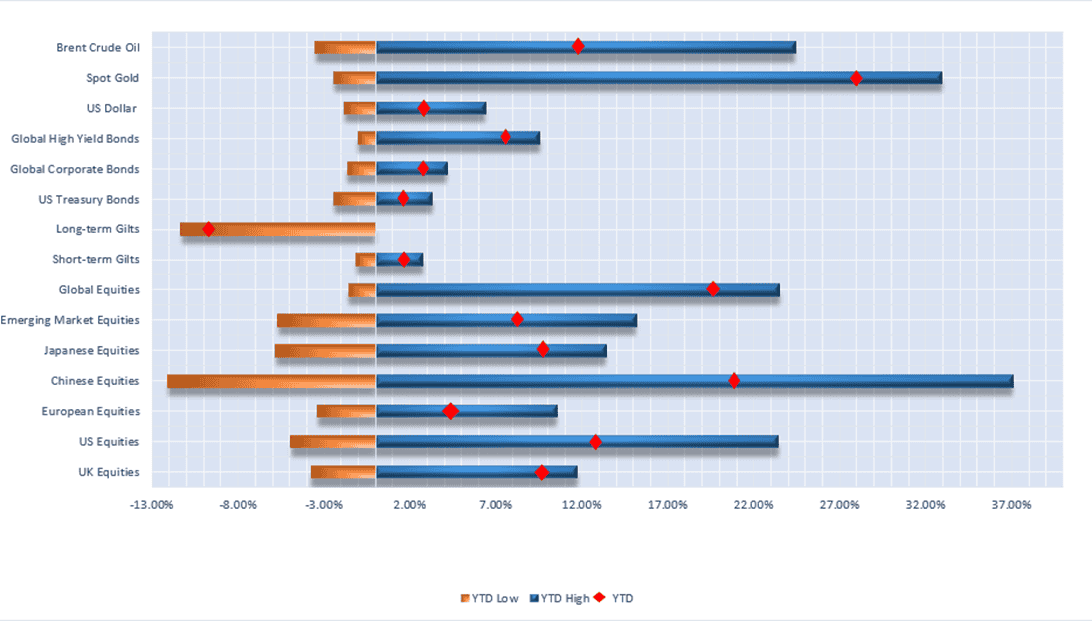

Selection of assets 2024 YTD returns and range of returns as at 31/12/2024 (the two ends of the bars represent the range of YTD returns and the red dots represent the final YTD return). Indexes used: FTSE All-Share, Russell 2000, STOXX Europe 600, MSCI China, MSCI Japan, MSCI Emerging Markets, FTSE UK Conventional Up To 5 Years, FTSE UK Conventional Over 15 Years, ICE BOFA US Treasury, ICE BOFA Global High Yield, ICE BOFA Global Corporate, US Dollar Index, S&P GSCI Gold Spot, S&P GSCI Brent Crude Spot. Returns hedged back to GBP with exception of US Dollar which is in US Dollar terms. Data from FE Analytics and MarketWatch.

2025 outlook

Once again, the start of the year Investment Outlook requires us all to dust off our crystal balls and look to the year ahead.

Firstly, it is important to distinguish between short-term and long-term drivers of investment returns.

Some factors (President Trump’s policy agenda, interest rate expectations and AI) are likely to weigh more heavily on markets in the short term and other factors have more influence over the longer term (ageing populations, shrinking workforces, and the energy transition as examples).

Two factors remain key though: a diversified portfolio is needed (although how this diversification is achieved is evolving) and regular rebalancing back to the intended asset allocation will help to improve returns relative to buying and holding. This is likely to prove as true in 2025 as it has always been.

Similar to 2024, the start of 2025 will be driven by central bank actions on interest rates and the path of inflation rates coupled with economic growth expectations (i.e. a lot of macroeconomics again). However, a differing factor and a potential iceberg to capsize the proverbial boat is the re-introduction of Donald Trump as US president on 20th January.

Trump and his policies will be a big driver of markets this year and he will have a big effect not just on US economic growth, but also global economic growth. Investors are very uncertain as to how this will play out as he has said a lot of things over the past few months, but no one yet knows what his actual plan is and what will be implemented. Portfolios therefore have to be nimble to prepare for all potential market outcomes as well as possible.

Trump is focusing his second term as president on US protectionist policies, and a big policy is the use of tariffs on US imports. The threat of these tariffs has loomed over every country, and this will make it more expensive for the rest of the world to export to the US.

This presents several challenges both for the US and for the exporting country and will likely add to inflation over the next year if the tariffs are fully (or even partially) implemented. The US accounts for approximately 13% of global import trade and so countries may well look to other areas to export their goods in an attempt to reduce the impact of any potential tariffs.

There is a variance between investor expectations and economist expectations, with the latter forecasting a more negative outlook. Economists seem to be taking Trump’s threats at face value. Although aware of the risks, the lesson from Trump 1.0 was to take him seriously but not literally. We therefore see the potential for positive performance in US equities once again this year on the back of increasing company earnings (which is the long term driver of stock markets).

The debate will continue over whether AI companies are over-valued, but whether this is the case or not, we will likely see a further broadening-out of the AI theme into other companies less directly involved in the development of AI itself. Think infrastructure and industrial companies building the data centres needed for AI.

In past periods ‘overvalued companies’ have eventually become a weakness in markets when the bubble bursts. With an evolving investment dynamic these mega-cap companies may be just a feature of the markets. The winners may not always stay the winners but with solid cashflows and huge future potential, they may stay at the top for a lot longer than companies have in the past.

An arguably more interesting point to consider with AI and technological developments is how it is changing the typical business cycle as we presently know it. The use of AI in improving productivity and reducing the labour need in certain areas will mean that the business cycle will not be as we have seen it in the past. One could argue we have seen this already, with many commentators expecting the US to enter recession at some point over the past two years whereas (so far, at least) growth has remained consistently strong.

Yield curve inversion (when shorter dated bonds yield more than longer dated bonds, the opposite of a normal yield curve) has nearly always foreshadowed a recession but again, we have not seen one yet.

The main theme coming into 2025 is again interest rates. Investors are expecting they will fall by a much smaller amount this year, with potentially just the one cut in the US. This presents an opportunity in the bond sector, as bonds already yield an attractive return and if there are interest rate cuts there is scope for some bond to deliver some capital growth as well. Further to this, with inflation now much lower and closer to 2% targets, bonds are yielding a positive real return (the return after adjusting for inflation).

A big risk to the bond sector is the resurgence of inflation and a rise in interest rates again. Although this is a less likely scenario, it is one we are watching out for.

Corporate credit spreads (the difference between the interest rate at which companies borrow and the government’s borrowing rate) are tight but companies are surprisingly robust and have much stronger balance sheets then they have previously had. Therefore, corporate bonds still offer an attractive return.

In our view, for the highest-yielding and riskiest company debt the downside risks do outweigh the upside risks and any increase in interest rates or further deterioration in economic growth will push spreads wider, leading to capital losses on some bonds.

In the US corporate sector defaults are on the rise. Private equity firms have been buying up distressed companies and this has hidden some of the defaults we would otherwise have expected.

If interest rates do fall gold should continue to benefit and some commentators are predicting that the precious metal will reach $2,795 per troy ounce, which would be an increase of around 7% from current levels. Although this is much lower than the 27% return in 2024, gold may offer some safety and help to diversify away from volatile stocks and bonds this year. The demand for gold from central banks looks unlikely to waiver, with China once again resuming its gold purchasing program.

The outlook for Europe is not as bright as the US, with major headwinds making the bloc look more unattractive this year. Political instability is certainly one factor, with French government bonds looking more risky than other regions (at one point in 2024, the French government had to pay more to borrow than Greece).

One problem is that the German manufacturing sector, a powerhouse in European growth, remains sluggish. Any tariffs imposed by Trump will weigh heavily on the exporting ability of the bloc and will likely mean cheaper goods from China will flood the market in its place.

In the UK, the outlook remains uncertain in light of flat economic growth and concerns over the borrowing capacity of the new Labour government. The big question this year will be whether the UK can avoid a year of stagflation (characterised by zero growth and inflation above the central bank’s target).

Recent data showed the Labour government have nearly reached their self-imposed borrowing limit before any of the extra borrowing has been used for actual investment. Investors will be closely watching the UK economy and whether the government will stick to its borrowing limits and whether tax increases or drastic spending cuts are looking likely.

Higher employer national insurance burdens from the first Labour budget in 14 years have not created the desired spending power and this could mean an uptick in inflation for consumers as well, further weighing on growth prospects.

UK investors continue to be more downbeat on the UK relative to international investors and this negativity is clearly becoming entrenched in a struggling economy.

In keeping with previous years, UK equities will likely not benefit from recent tailwinds as much as the US or Japan and long-term, the UK needs to attract investment and innovation to generate higher long term returns.

The environment is not favourable for smaller UK companies, with low economic growth, high interest rates and low investment. If we do see interest rates fall faster than expected, small cap equities may outperform though, especially given their underperformance relative to large cap stocks over the past few years.

All in all, interest rates will still play a key role in markets over the next year. Positive stock market performance does not rely on economic growth alone and longer-term themes such as AI and decarbonisation should still provide a tailwind to stock markets and company earnings. Overall we are positive for equity markets and bond markets offer attractive yields, though volatility will remain high as the investment landscape evolves with technology and social changes.

2025 Key Drivers

- President Trump’s policy decisions – deregulation, lower taxes, higher tariffs, mass deportation and threats of invasion.

- Valuation and earnings growth of big tech companies.

- Chinese economic growth and government interventions.

- The path of interest rates and the degree to which inflation is kept under control.

- Global political instability and geopolitical tensions.

UK

As expected, the Bank of England left interest rates unchanged at 4.75% on 19th December, its final meeting of 2024.

Three out of nine members of the Monetary Policy Committee voted for a rate cut, but more persistent inflation persuaded the majority of MPC members that rates should remain higher for longer.

Inflation accelerated to 2.6% in November and despite a decline in job creation, wage inflation remained high, increasing by 5.2% year-on-year. The Bank of England has also revised down its growth forecast for the final three months of 2024 to zero.

Looking towards the year ahead, the Chancellor’s recent Budget is having a large impact on forecasts for 2025.

Some economists believe that the planned increase in employer’s National Insurance Contributions will make UK companies more hesitant to hire, lowering economic growth over the year.

Others believe that the £40 billion of fiscal stimulus announced will feed through into the economy in 2025 and provide growth opportunities.

The consensus view is that the UK economy will grow between 1.0% and 1.5% in 2025. Owing to rising gas prices, inflation is expected to rise in the first half of 2025 to around 3% before falling back to the Bank of England’s 2% target towards the end of the year as service sector inflation eases.

The Monetary Policy Committee looks set to continue to reduce interest rates steadily. With the current rate at 4.75%, the consensus view is that the MPC will reduce rates by between 75 and 100 basis points (i.e. to 3.75% to 4% by the end of 2025), depending on inflation and the strength of the domestic labour market.

When it comes to Trump, the impact of any US tariffs placed on UK is likely to have a limited impact on the UK economy.

As a service-led nation, goods account for 45% of total UK exports and only 15% of these goods are exported to the US. The anticipated 10% tariff on goods imported to the US is thus unlikely to have a large impact on the UK economy, although some specific companies/sectors may be more affected.

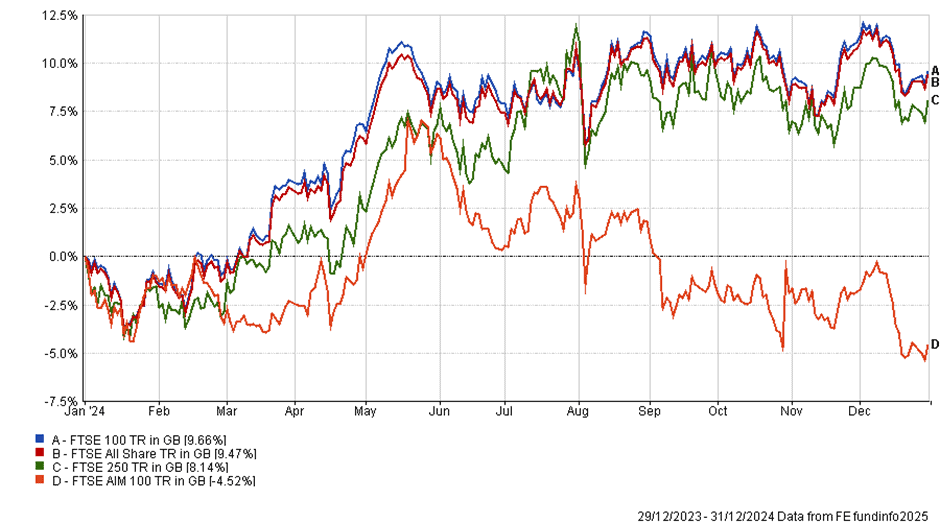

YTD performance of major UK stock market indices

Broadly, UK equities performed well in 2024. The FTSE 100 increased by 9.66% over the past year, with the FTSE 250 increasing by 8.14%. Smaller UK companies, represented by the FTSE AIM index, had another difficult year and ended 2024 negative 4.52%.

Although large cap UK equites therefore performed well in 2024, they are still relatively undervalued when compared with their international peers – especially the US. With markets expected to broaden, there may be opportunities for further growth in UK equities this year.

US

2024 performance of major US stock market Indices (returns in USD, not hedged)

2024 turned out to be another extremely positive year for US stock markets, with the tech-focused Nasdaq 100 index returning 25.88%. The S&P 500 also returned a staggering 24.50%, whilst the Russell 2000 and Dow Jones Composite Average returned a respectful 11.11% and 10.82% respectively. These large gains were almost entirely driven by the “Magnificent Seven” (Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA, and Tesla) as investors got extremely excited about revolutionary technology, such as artificial intelligence, that these companies look likely to be leaders in.

Another factor that supported equity market returns was the prospect of lower interest rates. The Federal Reserve’s base rate started the year at 5.50% and was reduced by 1.00% throughout 2024 with the first (long anticipated) rate cut coming in September. Bond market investors also welcomed the news initially as the US 10 Year Treasury yield reduced to 3.62%, giving investors a much-needed rally after a 2023 high in yields of 4.93%. This trend soon reversed as markets priced in the likely consequences of a second Presidential term for Donald Trump.

The biggest surprise to many investors in 2024 was the resiliency of the US economy. GDP growth is expected to be in the region of 2.6% for 2024, defying the “certain” recession many analysts forecast at the beginning of the year. Inflation continued to decline but failed to reach the Fed’s 2% target, the low being Septembers 2.4% print. CPI has since risen to 2.7%, suggesting that the economy may still be a little too hot.

To cap off an eventful year, Donald Trump won the 2024 Presidential Election and will serve an inconsecutive second term. Even before his inauguration on 20th January, he has been able to move markets with his plans, most notable the infamous “Trump Tariffs”. Whether this is true or just a bargaining chip, sound advice would be to take him seriously but not literally going into 2025.

Our view heading into 2025 it best described as “cautiously optimistic”. Transformative trends will continue to progress at a rapid rate, consumers and companies appear to be in a strong position, and easing financial conditions will act as a tailwind. The main risks at present would appear to be rising debt levels, equity valuations becoming stretched and geopolitical uncertainty.

As mentioned, the so-called Magnificent Seven stocks dominated markets in 2024 and we see this continuing throughout 2025. The aggregated market capitalisation of these seven stocks makes up approximately 31% of the S&P 500 index and this is the most concentrated the index has been for 60 years.

The reason is that these companies were able to grow their yearly earnings by 18.1% (as at Q3 2024), whereas the rest of the index only managed 0.1%. Artificial intelligence looks set to stay and these companies are in the best position to benefit from the revolutionary trend.

These mega-cap technology stocks also have strong balance sheets and are flush with cash. In this sector, they can use this to reap two main benefits: Research and Development (R&D) and Mergers and Acquisitions (M&A).

Extensive (and expensive) R&D is vital to excel in this area as the greatest technology wins, and because the rewards are not immediately paid, lower margin companies cannot afford to compete if it means incurring heavy losses for an extended period of time.

Those smaller companies which do manage to create cutting-edge technology will, sooner or later, be faced with an offer they cannot refuse and be snapped up by one of the giants. It is worth noting that Lina Khan, Chair of the Federal Trade Commission (FTC), is stepping down from her position under Trump – she has been notoriously restrictive for M&A deals in the name of anti-trust legislation.

The worry here is in terms of valuations. The Magnificent Seven’s price to earnings (P/E) ratio is currently 32, whereas the ratio for other 493 stocks in the S&P is roughly half of that.

We may see a broadening, where lower market cap companies catch up, but with approximately 26% of investment into S&P 500 companies coming from passive investment funds, large caps getting larger has become somewhat self-fulfilling. And as long as the economy continues to grow, flows will continue to flow into these passive index funds.

In the bond market, investors will be firmly focused on where the economy is heading and how the central bank will react. The United Nations predicts US GDP growth will decline to 1.9% in 2025, although other estimates are mixed with Goldman Sachs forecasting a 2.5% increase. Admittedly, this will mostly be driven (positively or negatively) by the incoming Trump administration’s trade policies.

In terms of inflation and employment (the Federal Reserve’s “dual mandate”), the Fed expect Personal Consumption Expenditures (PCE) inflation to be approximately 2.5% and unemployment to be around 4.3% in 2025. The latest Fed “dot plot” projects two 25 basis point cuts in 2025 with this also being the market consensus.

We think this is likely to prove accurate but do see a slight upside risk to inflation in the short term, again owing to Trump’s trade policies and onshoring. Over the longer term however, we do see inflation being kept largely at bay as a result of technology’s deflationary effects.

In the bond market, investors will not only have to watch the short end of the yield curve in 2025 (which is mostly dictated by central bank policy), but also the long end (which is dictated by supply, demand, and other economic factors).

The Treasury Department, newly led by Scott Bessent, is expected to increase issuance of long-term debt during his term in an attempt to address the US’s reliance on short term debt.

The US national debt currently sits above $35 trillion and is over 120% of GDP, which most would deem unsustainable. We will also have the “debt ceiling” political theatre again in 2025, which we expect to get resolved swiftly this time around. Increased debt issuance will put upward pressure on yields, most of which we believe is already reflected in the price. Since September, the 30-year Treasury yield has increased from 3.96% to 4.95%.

Finally, a word on Trump. The uncertainty around his policies (and social media posts!) will probably induce some short-term volatility for investment markets. The proposed wide-stretching tariffs on all imports, with significant increases for imports from selected nations (including China), will give the market a short-term inflation spike risk but in the longer term, once manufacturing has been brought back to the States, it could be a catalyst for higher GDP growth.

Whether the Department of Government Efficiently (DOGE), led by Elon Musk and Vivek Ramaswamy, or the new Artificial Intelligence and Technology and Crypto Czar, David Sacks, will bring about increased productivity is yet to be seen. However, we believe that these “America first” policy changes will ultimately be good for the nation and its long-term growth prospects.

Europe

The Eurozone economy showed signs of modest recovery in 2024, despite a flurry of headwinds: slow economic growth, political instability, global trade uncertainty, and ongoing conflicts. These are likely to continue to be the ongoing themes for Europe heading into 2025, impacting both the region’s economy and its stock markets.

The Euro area’s annual inflation rate ended 2024 at 2.4%, down from the 2.9% recorded a year earlier. During this year the ECB implemented four consecutive interest rate cuts, bringing the interest rate down to 3% by the year’s end. This easing of restrictive rates reflects the need to stimulate economic growth, whilst maintaining stable inflation as we move into 2025. Investors have however questioned whether the ECB has been behind the inflation curve and whether more cuts should have been implemented.

The Eurozone experienced a modest pick-up in growth, with GDP increasing by 0.8% in 2024. This recovery is expected to continue with the European Commission projecting GDP growth of 1.4% for 2025; this would seem to be an optimistic forecast given the difficulties the region faces and there is much scepticism as to whether these forecasts are realistic.

The bloc has major issues in key sectors such as manufacturing, which continues to struggle with reduced demand and high energy costs. Any continuation of the war in Ukraine will likely continue to weigh on the region, but if a ceasefire or negotiated settlement between Russia and Ukraine can be agreed the reduction in uncertainty and potential for energy prices to ease may result in an uplift in markets.

Economists at Goldman Sachs predict a conservative 0.8% growth in the bloc, with a 30% chance of a significant recession in 2025. Growth is expected to be dampened further by the expected restrictive fiscal policies in France and Italy, which are aimed at curbing rising debt levels, as well as external pressure from a renewed Trump US presidency and the impact of his trade policies.

Internal political problems will also influence the investment landscape this year. Germany’s elections in February 2025 are unlikely to yield significant changes to its current restrictive fiscal policy.

Meanwhile, fragile coalitions in France and Spain are likely to result in more political turmoil and a failure to address the economic and geopolitical challenges facing the region. A renewed Trump presidency further complicates the environment for Europe, with uncertainty over global trade and geopolitical relations in general.

Any tariffs imposed by Trump on European goods will hurt the earnings of European companies and may even push inflation higher in the area. If this is combined with weak economic growth, this would be damaging for the investment outlook for the bloc.

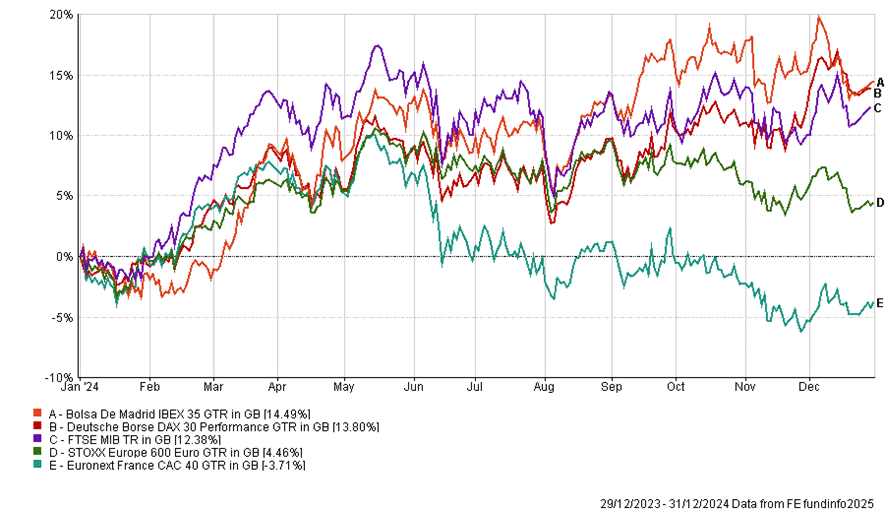

European equity markets again underperformed relative to their US counterparts in 2024, with the STOXX 600 benchmark index gaining 6%, compared to a 23.3% boost for the S&P 500.

Citigroup forecasts the STOXX 600 to reach 570 points by the end of 2025, representing an 11% upside from its December 2024 closing value. Despite this optimistic outlook, European equities still face significant risks and investors are generally preferring other markets such as the US and Japan, which are viewed as having a greater potential upside.

The fiscal stability of France and Italy remains uncertain, with weak economic data, particularly in manufacturing, continuing to impact Germany. Additionally, competition from an oversupply of Chinese goods, which is driving prices down, and concerns over US trade tariffs create further pressure on European corporate earnings.

The automotive industry is one area which is projected to see negative growth in 2025 and is likely to experience the worst of any Trump tariffs. More widely, Europe’s discretionary goods sector is another potential loser. Bernard Arnault, the CEO of the European luxury goods company LVMH has recently been one of the handful of CEOs trying to build relationships with the incoming president in an effort to protect the exports of their companies.

Any tariffs imposed on luxury goods coming into the US will hurt company earnings and coupled with a decrease in Chinese consumer confidence, could see this sector experience a large valuation de-rating.

Nonetheless, if the ECB can stabilise inflation close to its target level it will be able to continue to cut interest rates to supportive levels. This will benefit consumer-facing sectors such as retail, which are expected to perform well as they cater to domestic consumers within Europe, limiting the impact of potential changes to external trade policy.

Markets remain neutral on European fixed interest (bond) markets for 2025, again the biggest risks being political. If the ECB can continue to cut interest rates this should be good for bond prices – however, political risk and budget deficits will present headwinds to the markets, France especially. Being selective in European fixed interest and identifying those countries with the potential to outperform relative to the broad market will be key.

Corporate bond spreads over government bonds in Europe are not as tight as in the US and these valuations make corporate and high yield debt more attractive in Europe. The higher yields offered on debt from companies with lower credit ratings means yields should not move too much should the economic situation deteriorate and default rates pick up.

While opportunities exist in Europe within certain sectors, the outlook remains difficult and volatile. Despite valuations being reasonably priced, significant issues remain for Europe including domestic economic challenges, political instability and external pressures.

YTD performance of major European stock market indices (returns hedged to GBP)

Japan

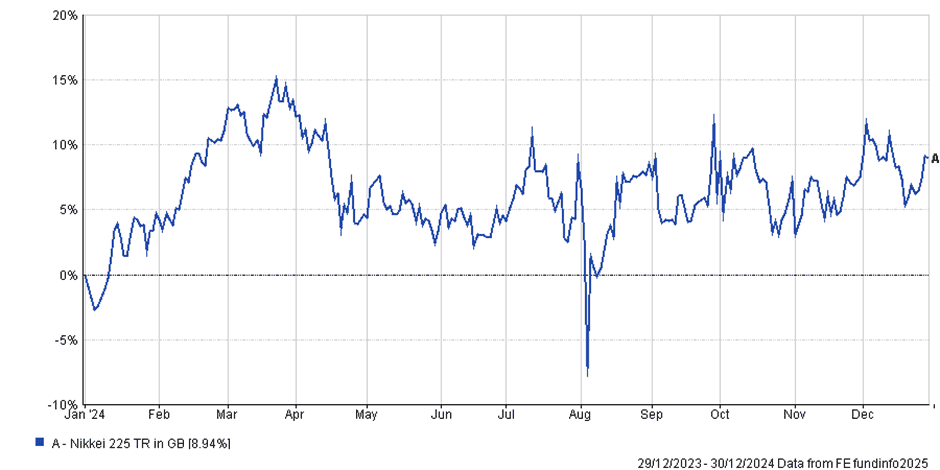

Despite heightened volatility over 2024, Japanese equities (in local currency) were one of the best performing assets, increasing by 20.90%. However, due to a depreciating Yen, UK investors witnessed a lower annual gain of 8.94%.

The outlook for Japanese equities is largely positive. Domestic reflation combined with wage growth, accelerated share buybacks and continued corporate reforms will all likely benefit Japanese equities.

Unlike western economies, inflation is seen as a positive and signals that the Japanese economy is becoming more normal after decades of very low inflation and deflation.

In response, the Bank of Japan is expected to continue to raise interest rates into 2025. It is expected that rate rises will help to strengthen the Yen and increase returns for international investors.

Japan’s role in global technology, particularly in robotics, semiconductors, and green technology is seen as a growth area for the region and should provide opportunities over the coming year.

Despite demographic challenges, there are potential opportunities in sectors catering to an aging population, like healthcare.

Overall, investors are cautiously optimistic for Japanese equities. The region could provide value for investors looking outside of ‘overvalued’ western markets.

YTD performance of the Nikkei 225 Japanese stock market index (returns hedged to GBP)

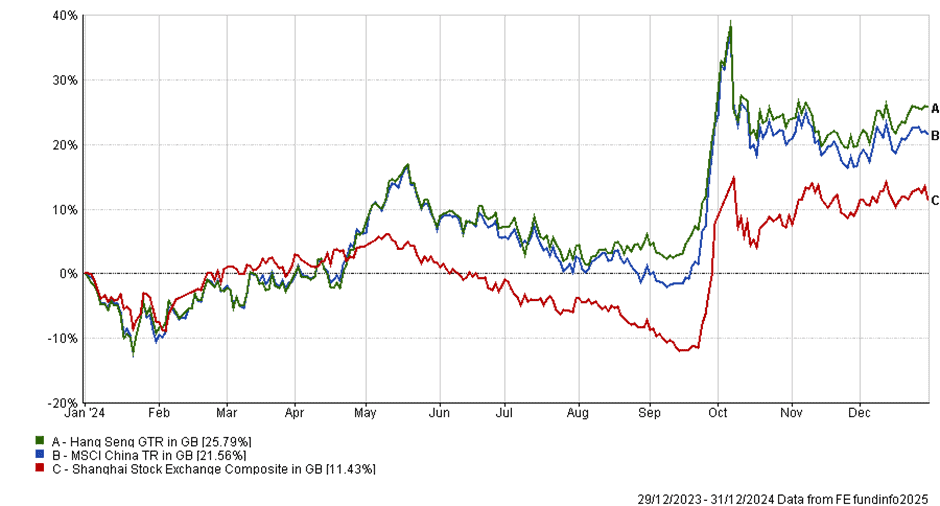

China

2024 performance of Chinese stock market Indices (returns hedged to GBP)

Chinese equities had a mixed 2024 to say the least. The Hang Seng and Shanghai Stock Exchange Composite indices posted gains of 25.79% and 11.43% in sterling terms respectively.

Although these returns are comparable to their American counterparts, it was achieved with over double the level of volatility. The MSCI China index, for example, had a peak to trough decline of 15.81% from May to September and then a huge gain of 39.96% to the start of October. Poor performance from the first half of the year can be attributed to the local property market crisis, whilst gains in the second half are a result of government and central bank stimulus.

In response to sluggish growth and to bolster a recovery from the crisis, the People’s Bank of China announced wide sweeping reforms, including a reduction in the Reserve Requirement Ratio (RRR), a lowering of key interest rates, and a special lending facility for struggling sectors. Despite widespread struggles, sectors such as electric vehicles and technology continued to thrive.

During the year many analysts laughed at the Chinese government’s GDP growth target of 5% for 2024 with the challenges they faced. According to both World Bank and Goldman Sachs, GDP growth for 2024 was 4.9% – although not quite at the 5.0% target, 4.9% for a year with such internal struggles is still more than respectable.

Going into 2025, the consensus forecast for GDP growth is 4.8%. This reflects the likely reduction in exports to the USA due to the increased tariffs but also positive drivers such as structural reforms and an internal consumption uplift. The Chinese government is expected to prioritise “common prosperity” by announcing initiatives that focus on wealth distribution and social stability to improve consumer confidence and therefore spending.

On the corporate side of the equation, it is expected that the Chinese government will also aid companies to maintain their global competitiveness, especially in strategic sectors such as semiconductors, renewable energy, and artificial intelligence.

At present, China’s total annual exports for 2024 is expected to be in the region of $3.74 trillion, $567.60 billion or 15.20% of which went to the United States.

The US imported approximately $3.30 trillion worth of goods in 2024 and given the $567.60 billion imported from China (17.20% of total imports), it is reasonable to infer that both nations need each other to a similar extent. In our opinion, Trump’s protectionist policies will change the make-up of this import/export relationship but it will take far longer than his four-year term for the US to completely move away from Chinese goods.

2025 should be a more positive year for Chinese equites, especially given the starting point in terms of sentiment. That said, major risks do still remain that could reverse this view.

The three major risks we foresee are geopolitical tensions, debt concerns, and demographics. We have already mentioned trade tensions with the US but the other area of tension to keep an eye on will be Taiwan. It has long been known that China wants to reunify with Taiwan, by force if necessary, due to its view that Taiwan is a breakaway province. Movements here will certainly increase volatility and impact not just Chinese, but global markets.

Similarly to the US, China is also burdened with debt but do not have the luxury of the global reserve currency. High corporate and government debt, coupled with a fragile property market poses systematic economic risks. The dollar has constant demand, which will likely make it stronger relative to the yuan. This will make it harder for China to pay its dollar denominated debt; however, its exports will become more competitive globally. The net effect is unknown and will have to be monitored.

Demographics is not just a problem exclusive to China, so it must be looked at on a relative basis. China however does face major challenges with its working age population peaking in 2014 and the fertility rate falling to around 1.2 children per women, well below the 2.1 replacement rate. One point to note here is that with the introduction of artificial intelligence and robotics, human labour could become increasing less important. This trend will become more apparent and more important over the longer term.

The Chinese growth story does still remain intact, driven by innovation, improved consumption, and government intervention; however, the clearly defined risks must also be considered. Select Chinese companies will certainly outperform over the long term but the outlook for Chinese equities more broadly is unclear, and this remains a volatile region to invest in.

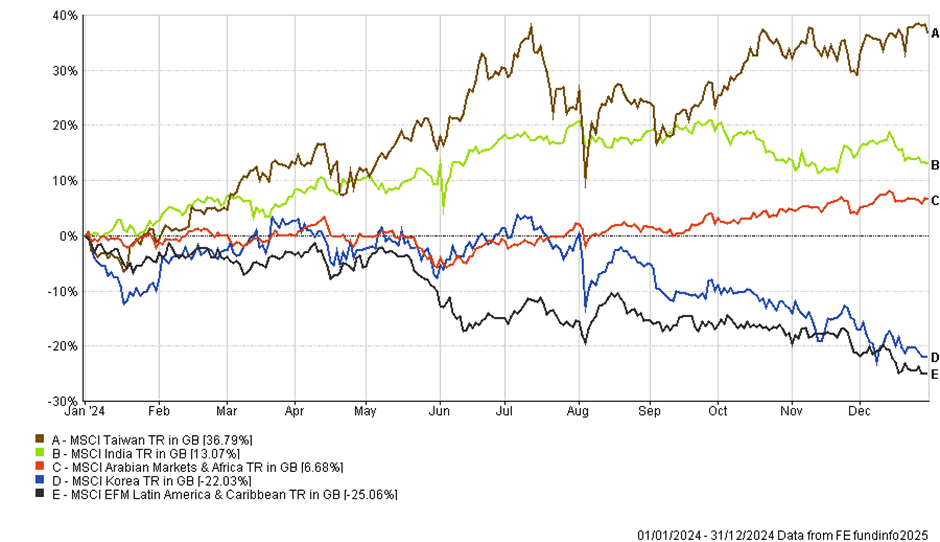

Emerging Markets

The biggest headwind for emerging markets this year again comes from the US. A strong US dollar is generally not good for emerging markets and it looks likely that the US Dollar will remain relatively strong, as the Federal Reserve has already said that there will be fewer interest rates cuts than investors have previously expected.

That being said, there is pressure on the US Dollar as countries switch their Central Bank reserves from the USD towards gold, the aim being to weaken any US influence over sanctions (China is a big purchaser of gold and has continued to increase its reserve holdings).

Emerging market debt has long been attractive to investors for the high yield it offers (reflecting the higher risk of holding the debt). Going forward, in our view investors are less likely to rely on this asset class for its return and more likely to rely on it for its diversification benefit. In simple terms investors should not continue to expect big returns owing to the currency risks.

This marks a change from 2023 and 2024, where emerging market central banks were generally loosening monetary policy at a time when most developed economies were suffering under rapidly rising base rates.

Like Europe, South Korea has seen its share of political instability recently and this will continue to rock the market. Any pullback in technology sector valuations will hurt the country as around half of its stock market is made up of technology companies. As mentioned, high valuations for select stocks may be a feature of markets and we do not see a large sell-off as being likely. Earnings for these big tech companies have beaten expectations and have justified high valuations so far.

Similar to South Korea, Taiwan has benefited from the demand for technology stocks. The bigger risk for Taiwan is the political risk from China.

India continues to remain attractive as long-term structural tailwinds provide great opportunity for the country, namely a population shift from low-income earners to middle income earners and the digitalisation of the country. Although valuations in India are high it looks likely to remain a high-growth economy.

Latin American countries had a tough time in 2024 as commodity prices were much lower and interest rates remained very high (10.25% in Mexico at the end of the year). Generally when commodity prices are higher this region performs well. While the short-term continues to be uncertain, over the long-term we see positives for the region. Commodities such as lithium and copper are likely to be high in demand for the electrification and decarbonisation transition in other countries.

Shorter term, any slowdown in global growth will hurt the performance of the region as the demand for commodities will fall with lower economic growth. Mexico has also been at the direct end of President Trump’s tariff threats.

If global growth remains strong and Trump does not follow through on all of his tariff threats then we may see positive performance across the broad emerging markets. Emerging economies such as Mexico face a tough trade-off: lowering interest rates to stimulate growth, but not lowering them too much so that their local currency weakens further against the Dollar.

One thing to bear in mind with emerging markets is that they are generally not “risk efficient”, meaning that the return you receive for the risk you take on is not sufficiently rewarded. With global volatility higher than in recent years this will likely remain true. That being said, exposure helps to diversify portfolios and there are pockets of returns to be found (India for example).

YTD performance of various emerging market equity indices (returns hedged to GBP)

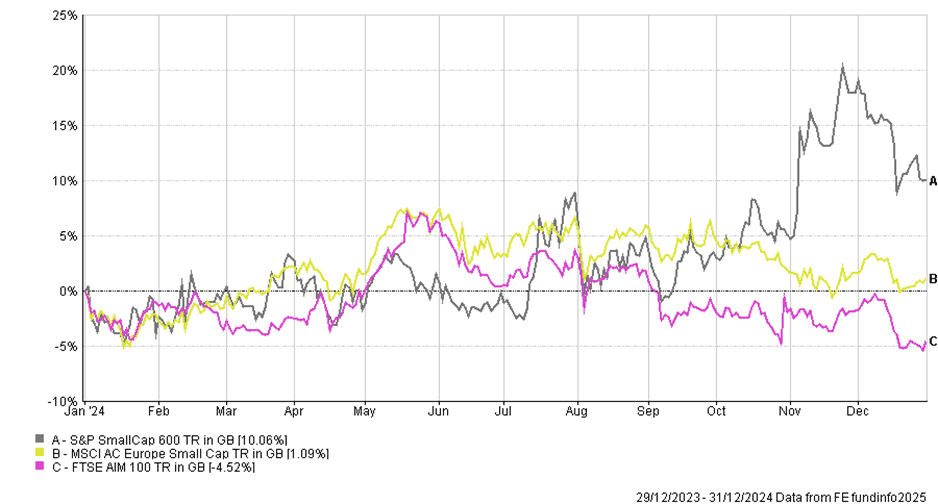

Small Cap Equity

It has been a tough few years for small companies and particularly in the UK. High interest rates have put pressure on margins as interest costs have eaten up a lot of potential profits. Lower pricing power has meant that consumers have switched to cheaper alternatives when prices have gone up, and a general risk aversion and investors’ preference for large tech companies has meant many smaller cap companies have missed out.

The UK in particular has not been attractive for smaller companies. The FTSE AIM 100 for example has declined 35% over the past five years and remained flat over the last year (the FTSE 100 was up 27% and 6% respectively over these periods).

One reason that smaller companies in the UK have underperformed relative to smaller companies in the US is the definition of small-cap stocks is very different. Small cap stocks in the UK tend to be much smaller than their US namesake equivalent – in the US “smaller companies” tend to be comparable to medium-sized UK companies.

So is 2025 the year for small cap stocks? One key driver for performance we will need to see is lower interest rates. Without lower rates companies will need to increase prices to keep their earnings in line. As inflation has been such a hot topic over the past two years, it is unlikely that consumers will stand for much more in the way of price increases.

In the US however the opportunities look more promising. Trump’s use of tariffs will focus more on US production, which will benefit US companies.

Smaller companies (whose goods and services tend to be more expensive than overseas imports) will become more competitive to US consumers and hope to see demand increase. On the other hand, higher tariffs will also mean higher inflation and higher interest rates for longer, so this is very much a double-edged sword.

As the AI theme broadens out we are likely to see smaller companies which have been overlooked start to benefit. Investors may begin to incorporate smaller companies into portfolios to a greater degree to diversify away from larger companies, whose valuations look more expensive.

In the UK, unfortunately the outlook is less bright. Higher national insurance burdens and a significant increase in the national minimum wage will reduce the earnings of companies and constrain their capacity to grow.

The UK also lacks depth in its technology sector, a big beneficiary for future growth. The potential for additional tax rises in future also looks more likely given the present state of the UK’s public finances, further dampening demand and earnings.

Private equity companies are looking to offload some of their holdings into markets and this may present some opportunities for new investment. Klarna, the fintech company is one example of this.

Overall, in our view there are opportunities for growth in smaller companies as their valuations are much discounted, but against a backdrop of tariffs and the potential for higher-than-expected interest rates their time to shine might not be yet.

YTD performance of global small cap stock indices

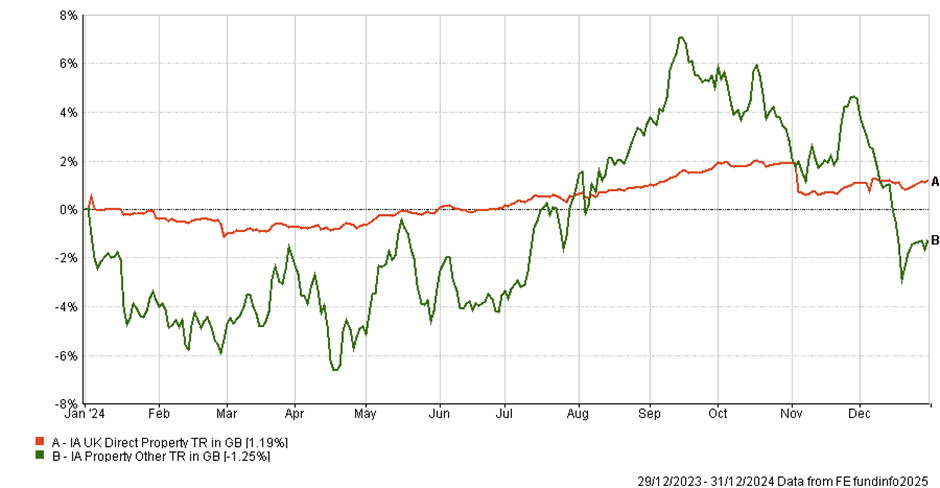

Property

Property, including residential and commercial real estate (both internationally and domestic), is expected to recover gradually in 2025. Lower interest rates and policy reforms addressing housing supply are key drivers, especially in the UK.

YTD performance of UK property investment sectors

Despite an uptick in performance during Q3 2024, the property sector ended the year negative as longer term interest rate expectations increased and global economies started to slow.

Residential

According to Nationwide, UK house prices grew by 4.7% over 2024 – with the average home in the UK costing £269,426 at the end of December. Despite last year’s increase, house prices remain below their peak of 2022.

In 2025, house prices are likely to see modest growth as lower interest rates encourage borrowing. If successful, planning reforms aimed at increasing housing supply may mitigate long-term price pressures.

Offices

Working from home trends continued in 2024, and office real estate struggled over the year. Looking ahead for the new year, prime locations are expected to retain value, while secondary lower quality properties may face challenges.

Limited supply into the market over the next three years, with continued tenant demand, should support the market. How office real estate performs in the new year will heavily depend on the wider economy and the willingness of companies to expand.

Industrial and Logistics

Strong demand for urban distribution centres, driven by e-commerce, positions the logistics sector for further expansion next year.

Structural trends such as increasing urbanisation, rising healthcare expenditures and the use of AI are likely to reinforce demand in research facilities and data centres. The main headwinds to these growth opportunities are slower economic growth and unforeseen regulatory changes.

Commodities

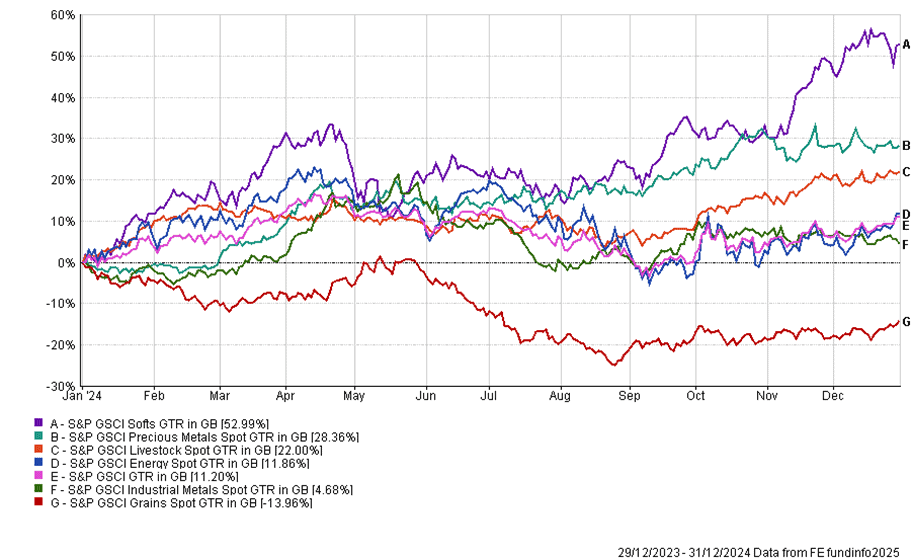

2024 performance of a range of global commodities (returns hedged to GBP)

Commodities had a mostly positive year in 2024 with “softs” and precious metals being the stand outs, returning 52.99% and 28.36% respectively (as measured by the Goldman Sachs Commodity Index). The gains in soft commodities were mostly fuelled by cocoa prices, which surged 50% due to adverse weather conditions and political instability in West Africa which disrupted supply. Coffee also rose due to lower-than-expected harvests in Brazil.

Precious metals had a stellar year with to gold rising above $2,500 an ounce, driven by the prospect of lower interest rates and increased purchasing from global central banks.

Oil fluctuated between $75-$90 per barrel as the Organization of Petroleum Exporting Countries (OPEC) implemented sweeping production cuts to stabilise prices given the reduced global demand. Increased US shale production helped to offset OPEC’s cuts and supply proved to be very resilient despite the uncertainty in Eastern Europe and the Middle East.

Elsewhere in the energy sector, European gas prices declined at the start of the year because of a milder than expected winter and increased Liquified Natural Gas (LNG) supply, but then rebounded as storage levels depleted.

Grains were one of the only commodity sectors to show a decline in prices during 2024. This was mostly due to increased supply coming out of South America and the US Midwest. Despite the ongoing geopolitical tensions, grain exports remained robust, especially through the Black Sea region. Russia and Ukraine, which are usually large exporter of grains, also managed to contribute significantly to supply. Easing fertiliser prices made production more affordable for many producers working with tight margins.

Looking ahead to 2025, another complex year in energy markets looks likely. We expect oil markets to remain elevated, supported by the commitment to supply constraints by OPEC members and the risk of any geopolitical flare ups from key producers.

On the demand side, moderate growth could increase demand slightly, again putting upward pressure on prices. Our view is that OPEC will continue to manage prices as they see fit, and their meeting minutes will dictate where the price is heading. Natural gas markets in Europe face uncertainty again as the reliance on Russian exports becomes evident, counterbalancing the push for greener energy sources.

Precious metals have the conditions to continue their upward trajectory because of persistent inflation concerns and continued central bank accumulation. Declining real yields (inflation rising and base rates declining) will also provide a tailwind. Gold will continue to be an attractive safe-haven asset for many investors, whilst silver sits somewhere between that and being used as an industrial input for renewable technology such as solar panels.

The green energy transition and the demand for industrial metals will remain a dominant theme in 2025, especially for copper, lithium, and nickel.

Copper, often seen as a global economic health indicator, has structural bullish factors in its favour as electric vehicle production will continue to accelerate and developed nations improve their grid infrastructure. Lithium will also be helped by the same factors. China will be the country to watch here, as it makes up nearly half of global industrial metal demand.

Agricultural commodities will remain sensitive to weather driven risks, particularly as El Niño conditions carry over into early 2025. Wheat, corn, and soybean prices are likely to experience volatility as weather can be greatly unpredictable. On top of this, grains may get caught in crossfire from the trade restrictions imposed by the US and the inevitable retaliation from exporting countries.

Overall, our outlook across the commodity complex is mixed. Whilst we do not believe prices will rise as much as they did in 2024, we can see prices remaining elevated for mostly supply driven reasons with demand remaining relatively constant. The prospect of a stronger dollar will also likely provide a headwind for dollar denominated commodities as they become more expensive for non-dollar-denominated buyers.

Robert Dougherty, Investment Specialist

Ryan Carmedy, Associate IFA

Harry Downing, Associate IFA

Fiona Chegwidden, Graduate Trainee IFA

January 2025

This article is not a recommendation to invest and should not be construed as advice. The value of an investment can go down as well as up, and you may get less back than you invested.