UK Interest rates are also expected to fall more slowly than previously anticipated as recent UK inflation data came in higher than expected again. That said, investors have largely priced in a 0.25% rate cut at the Bank of England’s next meeting in August.

In the US, former President Trump survived an assassination attempt and increasing pressure from senior Democrats means President Biden may yet be replaced as the number one candidate for the party in this election.

Unlike the UK election, the US election is expected to have a greater effect on investment markets and volatility may increase as we approach 5th November.

The difficulty is that nobody knows how the markets will be affected. One potential issue which has been reported is whether Trump will politicise the presently independent US Federal reserve. This will certainly rock investors’ confidence in what is deemed to be the safest currency in the world.

We have already seen technology stocks slump this week as Biden announced that the US is looking at further restricting trade with China, a big importer of the chips needed for AI. Trump also plans to restrict trade via increased tariffs if he wins the election.

For the highly valued technology companies this will impact their earnings and thus their share price. Investors have been moving into other areas in the short term such as UK equities to diversify away from this risk. The long-term potential for technology stocks still resonates with investors, as these typically account for the largest holdings in portfolios.

Smaller-company stocks (“small-caps”), having long been neglected by investors, have seen strong returns over the last month.

In Europe, the European Central Bank decided to keep interest rates at the same level, having previously cut rates by 0.25%. This is perhaps a case of acting too early, as the economic data is constantly changing.

US companies with low credit ratings have also been fallen out of favour with investors as the risk of defaults increases. Rates this year have not fallen as much investors originally predicted, putting more pressure on companies, many of which are coming up to refinance their existing borrowing this year. High quality investment grade debt has therefore benefitted.

Areas of Focus

Small-cap stocks have received a much-needed boost to performance as investors diversify away from large cap technology stocks.

Technology stocks may remain under pressure in the short-term as potential export restrictions to China add uncertainty to their earnings.

High-yield bond spreads have widened as investors move into safer bond investments.

Short-term credit continues to be favoured for its high yield, especially as interest rates do not look likely to fall too far this year.

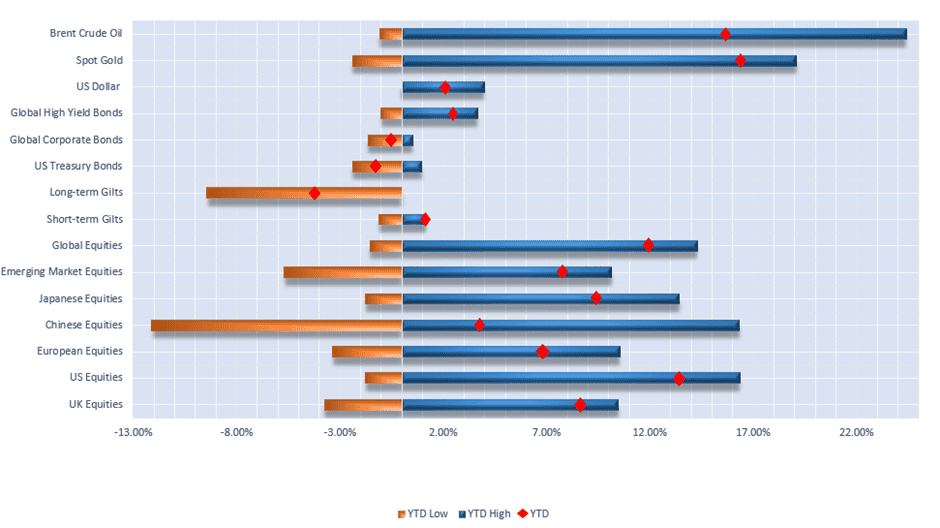

Selection of assets 2024 YTD returns and range of returns as at 19/07/2024 (the two ends of the bars represent the range of YTD returns and the red dots represent the current YTD return). Indexes used: FTSE All-Share, Russell 3000, STOXX Europe 600, MSCI China, MSCI Japan, MSCI Emerging Markets, FTSE UK Conventional Up To 5 Years, FTSE UK Conventional Over 15 Years, ICE BOFA US Treasury, ICE BOFA Global High Yield, ICE BOFA Global Corporate, US Dollar Index, S&P GSCI Gold Spot, S&P GSCI Brent Crude Spot. Returns hedged back to GBP with exception of US Dollar which is in US Dollar terms. Data from FE Analytics and MarketWatch.

UK

Headline inflation (as measured by the Consumer Prices Index, or CPI) dropped last month to the Bank of England’s 2% target for the first time in three years. Inflation in the UK is now below that of the US and Europe. Food prices, one of the main drivers of inflation, have started to decline – which has helped to ease price pressures of late.

While CPI reduced in line with expectations, service sector inflation remains high – currently 5.7%. With services CPI continuing to print to the upside, the Bank of England were all but forced to keep rates at 5.25% in their June meeting.

However, the Monetary Policy Committee opened the door to a quarter-point interest rate cut at their next meeting, which is due to take place on 1st August. As always, this decision will largely be data dependant.

The decision to keep rates steady dealt a sizable blow to the Conservative party, who had hoped that interest rates would fall before the general election – easing mortgage costs for homeowners.

As was widely expected, the general election on July 4th brought an end to 14 years of a Conservative-led government. Given that the outcome was predictable and the difference between the Labour and Conservatives’ fiscal policy was relatively small, markets were unmoved by the Labour landslide victory, and some expect that the Labour party majority will bring some well needed political stability to the UK economy.

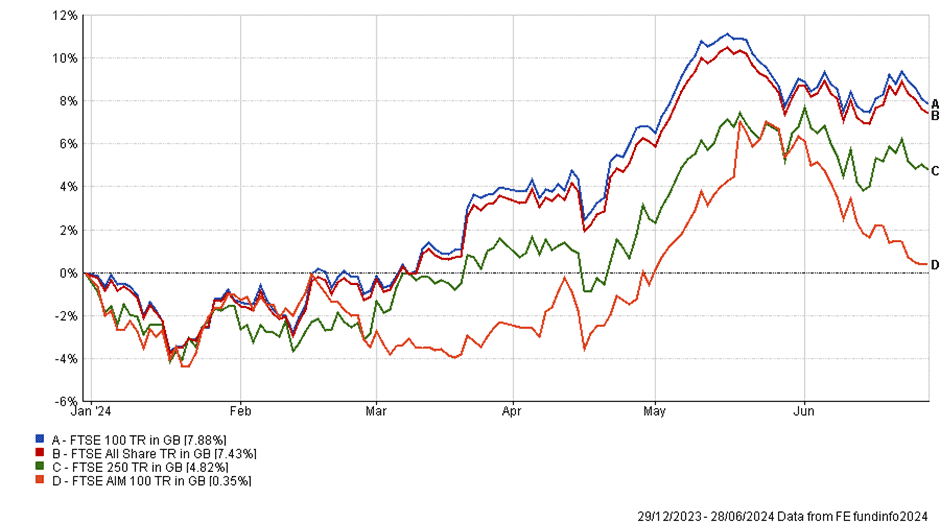

YTD Performance of UK Equity Markets

Broadly, UK equities failed to perform in June, with the FTSE 100 relatively flat over the month. The FTSE has now increased by a respectable 7.88% over 2024.

Revised figures show that the UK economy grew by 0.7% in the first quarter of this year, helped by a growth in the services sector. This higher-than-expected figure means that the UK was the fastest growing economy in the G7 between January and March. Markets reacted positively to this news.

Smaller UK companies, represented by the FTSE 100 AIM index, suffered a 5.65% loss over June, wiping out all year-to-date gains.

With the prospect of interest rate cuts on the rise, UK gilt yields fell significantly last month. The yield on 2Y gilts fell by 4.40% while the 10Y gilt yield fell by 1.92% in June.

| Yields as of 01/07/2024 (%) | Monthly change (%) | YTD Change (%) | |

| 2Y Gilt | 4.23% | -4.40% | 3.81% |

| 10Y Gilt | 4.24% | -1.92% | 14.06% |

UK Bond Yields as at 01/07/2024, monthly change and YTD change

The yield curve (the line showing the interest rates on government bonds of different maturities) has therefore started its ‘disinversion’. At the start of this year, the two-year gilt yield was 0.5% higher than the ten-year gilt yield. Now, the difference between the yield on 2Y and 10Y gilt yields has tightened, with only 0.1% difference between them.

Over the course of this year, longer term yields have risen more than shorter term yields. This is often referred to as a “bear steepener”. This is driven by investors pricing in higher-for-longer interest rates and it traditionally raises the likelihood of a recession.

USA

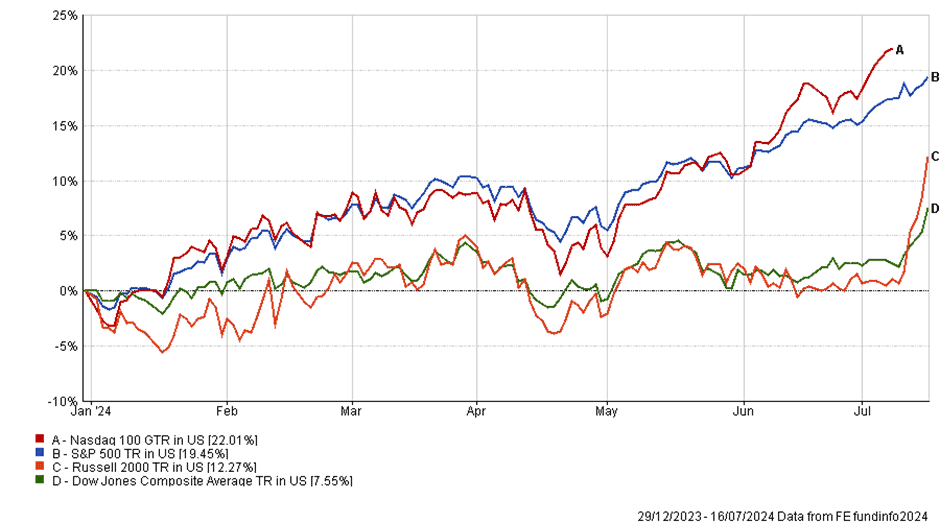

YTD Performance of US Equity Markets

The Russell 2000 joined the party in the month of July with a 11.53% gain (so far), after a first half of underperformance in 2024 relative to the S&P 500 and Nasdaq 100. June showed the same trend as before, with the two tech-heavy indices outperforming the two more traditional indices in the US. The year-to-date score board currently reads: 22.01% for the Nasdaq, 19.45% for the S&P, 12.27% for the Russell, and 7.55% for the Dow Jone Composite Average.

Investors will hope that this incredible performance can continue in the second half of 2024, although as always it cannot be guaranteed – the principal source of uncertainty is from the US election, which is likely to inject volatility as the year goes on.

Those companies that have released second quarter earnings reports have looked strong and various forces are moving interest rate expectations lower, both factors that should boost equity markets. This of course begs the question; how much is now already priced into markets?

Equity markets are what is known as “forward-looking”, meaning that known future good and bad news is reflected in share prices as investors attempt to get ahead of the market in order to capture both up and down moves as they happen. This is just one of the reasons why trying to time the market is so difficult (a long-term approach being preferred to benefit from the historical upward drift).

In June, US CPI inflation fell to 3.00%, lower than forecasts of 3.10%. This was down from May’s 3.30% and has led investors to believe that the Federal Reserve will reduce rates earlier than predicted just a few months ago. On a monthly basis, prices actually fell 0.10%, the first time CPI has come in negative since 2020. Core CPI dropped to 3.30% as it strips out the more volatile items like food and energy (petrol prices fell 3.80% during the month).

Markets now price in a 96.20% of a decrease in interest rates at the Federal Open Market Committee meeting on 18th September, a 94.40% probability of two or more 25 basis point cuts by the end of the year, and a 53.7% probability of three or more. Fed Chair Jerome Powell wrote in a testimony to Congress that the central bank has made “considerable progress” in their fight against inflation but still needs “more good data” before cutting the base rate. June CPI was released two days after this.

Another piece of data that will help the argument for lower rates came in the form of June’s labour market report from the Bureau of Labor Statistics. Some economists have speculated that the report showed signs of cooling and potential cracks in the economy. Unemployment increased to 4.10% from 4.00% and the previous two months of jobs growth were revised lower. In theory, the labour market should hold similar weight in policy decisions as CPI, as the US Federal Reserve has a “dual mandate” to promote maximum employment and stable prices.

| 17th June | 17th July | Change | |

| 2 Year Treasury Yield | 4.77% | 4.48% | -0.29% |

| 10 Year Treasury Yield | 4.29% | 4.19% | -0.10% |

Monthly Change in US Bond Yields

Bond yields dropped over the last month in reaction to the latest news. This has pushed up prices as yields and prices move inversely. Shorter dated bond prices will be less sensitive to interest rate decreases than their longer dated counter parts.

This effect is due to the fact that the longer dated bonds will have more coupon payments at the previously higher rate, making them more valuable. The shorter end of the yield curve dropping more quickly than the longer end (as shown above) is referred to as a “bull steepening” as it is perceived to be more bullish for markets. As opposed to the “bear steepening”, when longer duration rates rise faster than shorter duration rates, as mentioned earlier.

The biggest news from the US this month clearly came from the presidential election race. First, the two candidates faced off in their first debate since 2020. To say Joe Biden didn’t have the best of nights would be an understatement, with numerous long pauses and moments where he lost his train of thought adding to concerns about his age and mental acuity. No new revelations were uncovered, and the Republicans will certainly consider the night a win.

The dramatic attempted assassination of Donald Trump at a recent rally in Pennsylvania – where his life was spared by the skin of his right ear – was almost another tragic moment in American history. This unbelievable moment and the images it generated has only benefited Trump’s already-favourable odds of a November win.

To relate this back to markets, there are many possible consequences for investments but in our view, the main outcome of a Trump presidency will likely be a weaker dollar to make imports more expensive, boosting domestic manufacturing.

Europe

Unlike the UK, European markets have been much more susceptible to political turmoil.

After the far-right National Rally won a record number of seats in the European parliamentary elections, President Macron surprised markets and called a snap election in June. The CAC 40 index fell 6.2% on the news, and bonds prices were also damaged.

In the first round of voting, it seemed like the National Rally were set for a clear victory in France. However, when voters returned to the polls during the second round of voting, the left-wing New Popular Front alliance won the election with 188 seats.

The results mean that no party obtained the 289 sears needed for an overall majority, leaving the country with a hung parliament.

A hung parliament is likely to lead to months of political stalemate and the path forward for France is unclear. With that said, political uncertainty is often negative for markets – and it is predicted that France will be no exception to the rule.

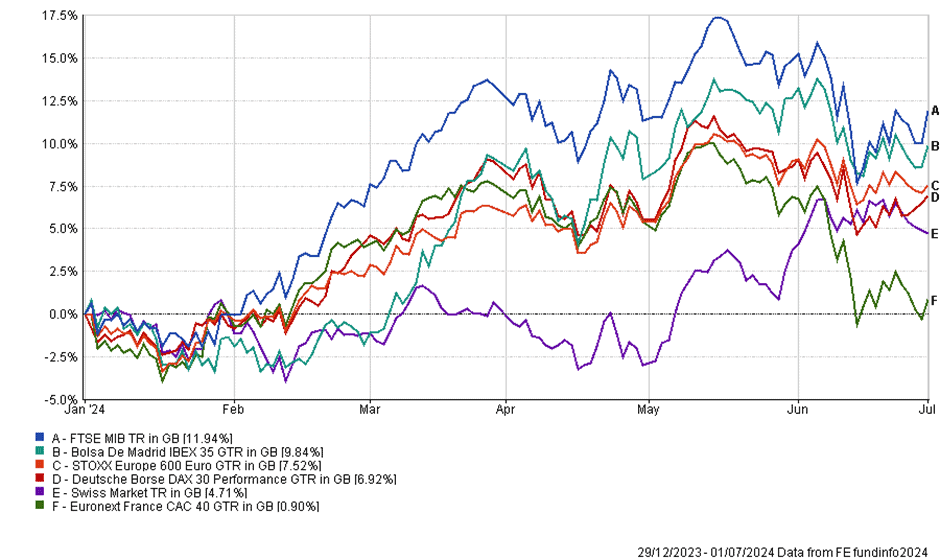

YTD Performance of European Equity Markets

European equities moved lower across the board in June due to dwindling hopes for further interest rate cuts in the region. France’s CAC 40 index was doubly hit by the nation’s political uncertainty and fell by 5.13% over the month.

Political uncertainty also affected European fixed income markets. The threat of a fiscally irresponsible government caused French government bond yields to spike. The yield spread between French bonds and the safer German Bund increased on the snap election by 0.3% – representing the extra risk. As with Rishi Sunak’s surprise general election, it appears to be a gamble which has not paid off.

Robert Dougherty, Independent Financial Adviser

Harry Downing, Associate IFA

Ryan Carmedy, Graduate Trainee IFA

July 2024

This article is not a recommendation to invest and should not be construed as advice. The value of an investment can go down as well as up, and you may get less back than you invested.