This has meant that bond yields have risen yet again this month and equity markets have taken another knock. We are still looking to inflation data to see if the downward trajectory will continue and where rates might end up sticking. Oil prices are rising as demand increases and supply is restricted by OPEC, complicated by the Israel-Palestine conflict, and this could cause inflation to move upwards again, both by consumers spending more at the pump and businesses passing their rising costs onto consumers.

On the other hand, as fuel is an “inelastic” purchase for consumers (meaning demand is not particularly sensitive to price, since for most people it must be bought anyway) we may see that this lowers demand for other products by functioning effectively as a “tax” on consumers. In turn this would bring other inflation factors down.

The US government narrowly avoided a government lockdown again. This is likely to be a recurring problem as US debt continues to rise and the debt ceiling will have to be increased, or government spending cut. An increasing supply of government Treasuries has resulted in rising yields as supply outstrips the present demand.

In contrast UK Gilt yields have remained relatively flat over the past month as the supply issue is not the same. Rather, UK yields remain subdued as economic growth stagnates and recessionary fears loom. Yields have not dropped as we may have expected in past business downturns due to the “higher for longer” market stance on interest rates. The commonly-held interpretation is that rates will stay higher even in an economic downturn as the Bank of England remains committed to reducing inflation.

We are also transitioning away from an environment of easy money, where central banks pumped trillions of dollars into economies to support a growth environment. With this money being pulled back out through the painful process of quantitative tightening, meaning capital allocation is tighter and the risk premium is greater (i.e. values are lower). In short, we should not expect easy returns during this period of high volatility and tight money, although returns will be available in some form nonetheless.

Enthusiasm for Japanese equities continues its sustained run as the Japanese central bank has opted for holding interest rates where they are, letting inflation climb higher. Corporate and shareholder reforms taking place in Japan are also giving investors confidence in a long neglected region. If interest rates do rise those companies incorporating better governance practices are likely to fare better than those that do not.

We have seen further damage to Chinese markets as the economic situation there deteriorates. One explanation for the lacklustre growth since its reopening is that rather than spending, consumers have been seeing their family and friends who they have been isolated from for the past three years. Therefore the prediction is that this spending will happen, but perhaps not until next year. Based on this idea, China therefore looks cheap at the present time. As always, the political risk, economic risk and property sector risk means that this hoped-for recovery could well not materialise.

Areas of focus

- Japanese equities continue to look attractive over the short to medium term. Long-term performance relies on economic and governance targets being met.

- Chinese equities look set to disappoint over the rest of the year.

- Small cap stocks, like they have for the year so far, remain out of favour. Lack of pricing power and tight credit conditions weigh heavily on their values.

- Short-term credit remains attractively priced, and the risk of missing out on capital appreciation from rate cuts remains low.

- Amid a potential economic downturn, cyclical companies remain out of favour while defensive growth companies look set to outperform (think energy, healthcare, consumer staples).

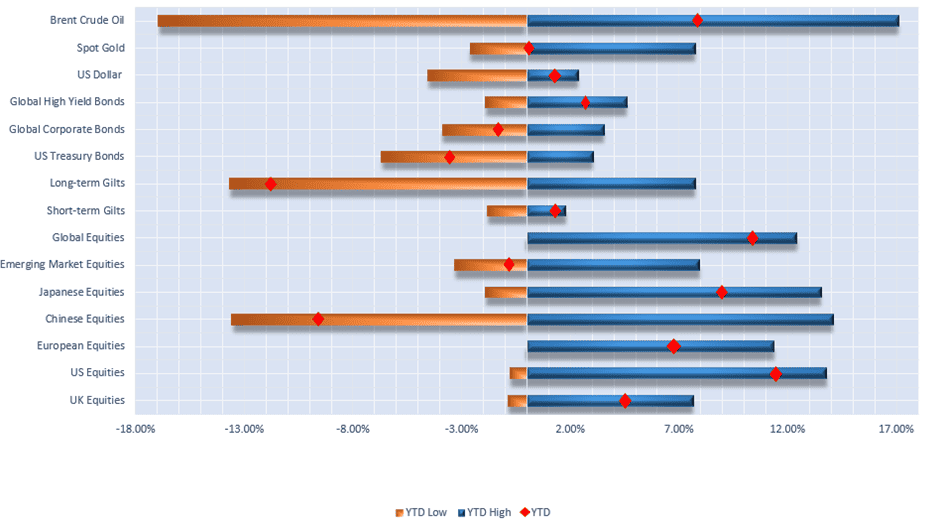

Selection of assets YTD returns and YTD range of returns as at 11.10.2023 (the two ends of the bars represent the range of YTD returns and the red dots represent the current YTD return). Indexes used: FTSE All-Share, Russell 3000, STOXX Europe 600, MSCI China, MSCI Japan, MSCI Emerging Markets, FTSE UK Conventional Up To 5 Years, FTSE UK Conventional Over 15 Years, ICE BOFA US Treasury, ICE BOFA Global High Yield, ICE BOFA Global Corporate, US Dollar Index, S&P GSCI Gold Spot, S&P GSCI Brent Crude Spot. Returns hedged back to GBP with exception of US Dollar which is in US Dollar terms. Data from FE Analytics and MarketWatch. Correct as of 11.10.2023.

Overview

September marked the end of Q3 and it also marked the end of the 14 consecutive rate hikes by the Bank of England. The prospect of interest rates being “higher for longer” drove international equity and bond markets last month and seemingly paused the recent AI-related boom witnessed in US technology companies.

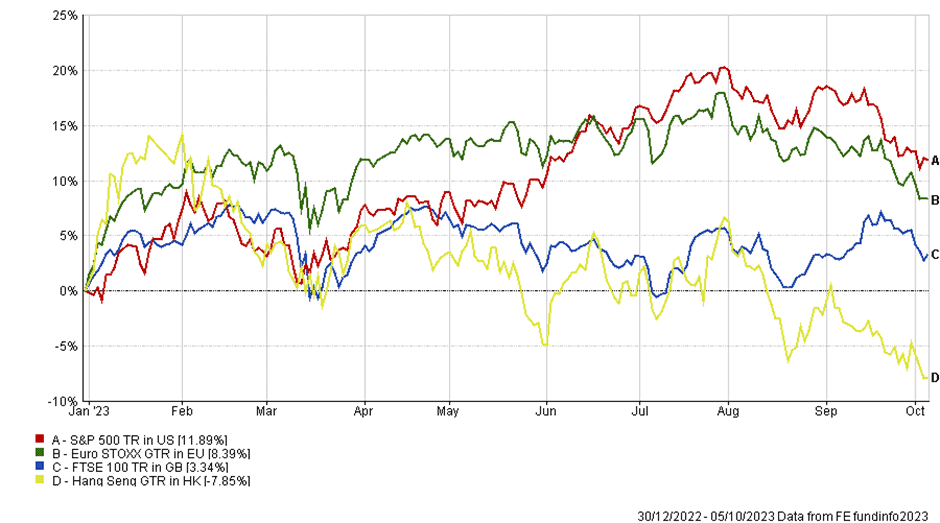

Chart showing YTD performance of global stock market indices

A surprise fall in food prices and services activity caused UK CPI to fall to 6.7% last month. This reduction in prices allowed the Bank of England some breathing room and led the central bank to pause its recent rate hike cycle – after 14 consecutive increases. Whether interest rates have peaked is still up for discussion, as four of the nine Monetary Policy Committee (MPC) members voted to raise rates.

An increase in commodity prices, mainly oil, allowed UK energy companies such as Shell and BP to gain some traction in September, which pushed the FTSE 100 higher over the month – closing some of the year-to-date performance gap between the US and UK equities. Higher interest rates also helped the UK banking sector, which typically benefits from increased spreads when interest rates rise.

The view of rates being higher for longer caused London house prices to fall 4.8% in September, according to Halifax’s House Price Index. Despite this, UK consumer confidence rose – which some economists attribute to a reduction in energy prices. When consumers get used to this reduction, however, some believe that UK consumer confidence will fall once more.

Like the Bank of England, the US Federal Reserve left rates unchanged in September. However, the central bank indicated that at least one more hike is likely – reiterating their commitment to bring inflation back down to target levels.

The Fed’s commitment to keep rates higher for longer caused a sell-off in the US government bond market, driving yields to their highest level since 2007. This was exacerbated by the release of the most recent US jobs data, which showed that 336,000 jobs were added to the US economy in September. While this represents good news for the US economy, global investors see a strong US economy as an issue that will ultimately lead to interest rates remaining – you guessed it – higher for longer.

While the S&P 500 is still positive year-to-date, the index struggled last month – falling almost 5% in September. It seems investors’ expectations of interest rates have finally changed in the US, and this has caused technology companies’ share prices to pull back from the all-time highs witnessed a couple of months ago. In response, the tech-heavy Nasdaq 100 index fell 4.97% over September.

Despite attempts by the government to stimulate the stock market, the Hang Seng index also fell 2.58% in September as the Chinese economy struggled to gain any sort of traction after reopening its economy. The over-leveraged state of the Chinese property sector also caused concerns for the region last month. Despite a flurry of measures aimed at stabilising the sector, Chinese new home prices continued to fall during September.

In Europe, the ECB decided to raise rates to a record high of 4% in its September meeting but signalled this was likely to be the last. Higher interest rate expectations and concerns over the Chinese economy caused the Euro STOXX index to fall last month. The consumer discretionary sector fared the worst in the region, once again highlighting the reliance on luxury goods exports to the Chinese middle class.

Looking forward to Q4, equity and bond prices will largely depend on how the US performs in the short term, and whether the economy can pull off a soft landing. It almost feels like something needs to break before stock markets can return to normal, and the traditional relationship between equity and bond prices returns. During this period, stock markets are likely to be volatile – something that we have become somewhat accustomed to over the past 12 months.

High Yield bonds

You would be forgiven for thinking that bonds have had no appeal in a portfolio over the last two years. With inflation high and interest rates rising from their troughs, we have seen bond capital values fall markedly. There has, however, been good performance in a small corner of the huge $133 trillion global bond market.

High yield bonds, while only accounting for 3.38% of global bonds outstanding, have delivered some of the best bond performance this year, along with holding their capital value to a greater extent than other bond classes in 2022. As always in finance, there is no free lunch and this return does not come without its risks (both present and future!).

High yield bonds are much like any other bond, the main difference is the credit rating of the issuing entity. High yield bonds are issued by companies with low credit ratings, less stable cashflows and a higher risk of default. Investors therefore demand higher interest rates to adequately compensate them for the risks. Depending on the economic outlook, the spread (or difference) between safer government bonds and higher-risk high yield bonds varies.

| Moody’s | Standard & Poor’s | Fitch Ratings | Quality | Risk |

| Aaa | AAA | AAA | Investment grade | Lowest risk |

| Aa1, Aa2, Aa3 | AA+, AA, AA- | AA+, AA, AA- | Investment grade | Low risk |

| A1, A2, A3 | A+, A, A- | A+, A, A- | Investment grade | Low risk |

| Baa1, Baa2, Baa3 | BBB+, BBB, BBB- | BBB+, BBB, BBB- | Investment grade | Medium risk |

| Ba, B, Caa, Ca, C | BB, B, CCC, CC, C | BB, B, CCC, CC, C | High yield/Junk | High risk |

The key question now is, going forward are they still a good investment?

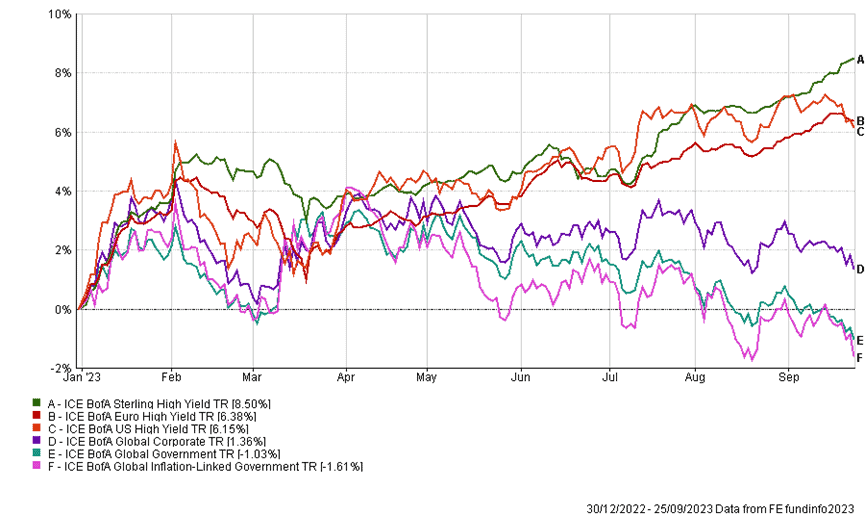

YTD performance of regional and global bond asset classes

The chart above plots the performance of high yield bonds against the performance of global corporate, government and inflation linked bonds so far this year. All of the high yield indices are in positive territory, while the government and inflation-linked bonds are in negative territory, and corporate bonds (while positive) are lagging behind.

Looking at the different regions, US high yield bonds have dipped over the past month while the spread between US High yield bonds and government Treasury yields have ticked up slightly, while still below their 2022 high. Any widening of this spread can be a sign of a lack of investor confidence in the economy, which then filters through to lower demand for high yield bonds.

Euro high yield bonds have also dipped slightly while Sterling bonds have continued their push upwards. Recent central bank rhetoric in the US points towards higher rates for longer which puts pressure on high yield bonds. Continued positive economic performance results in a higher risk that US rates will move even higher. Similarly in the Eurozone, a recession seems likely which moves investor demand back towards safer investments like government bonds.

In the UK, the recent interest rate pause by the Bank of England has been interpreted as good news for UK assets. We have seen government bond yields drop slightly, indicating investors believe interest rates will not stay as high for as long, or a recession is imminent. If the latter is the case, the continued high yield bond performance suggests investors think default rates will be lower in a downturn and do not see as much risk here.

The difference between the US and the UK in terms of yields is that the UK is much more likely to fall into recession, whereas the US has a greater chance of higher medium-term inflation due to stronger economic fundamentals.

The high yield bond outperformance can be attributed to how the different types of bonds react to changes in interest rates (see our article on Inflation Linked bonds for a more in-depth analysis).

In general, all else being equal, bond that have higher yields have a lower sensitivity to interest rates and so when interest rates increase, their prices fall by a lower amount (bond prices and yields are inverse – as one rises the other falls). The measure of a bond’s interest rate sensitivity is called “duration”. The higher a bond’s duration, the greater the magnitude of the change in the bond’s price for a given interest rate change when compared with a lower-duration bond.

With interest rates continuing to rise throughout 2023, we have therefore seen the capital values of high yield bonds hold up to a greater extent than other bonds with higher credit ratings and lower yields.

When you separate this return between the interest payments a bondholder receives and the change in a bond’s price (i.e. the capital growth or loss), the higher interest payments available from high-yield bonds have more than compensated for the falling bond prices, leading to positive performance overall.

Future Outlook

Another key component of a high yield bond’s return is the perceived credit risk in the issuing company, and that is the main issue which will determine investors’ asset allocation decisions to this sector in the short-term.

With interest rates now at decade-high levels and economic growth beginning to stagnate, default rates in the high yield sector are expected to increase. Recent data from Fitch Ratings suggests that we may see the default rate increase to between 4.5% and 5.0% for 2023. While this does not seem high, any default can severely detract from a bond fund’s performance and the perceived credit risk for the sector as a whole will increase.

In turn, as the perceived credit risk increases investors will demand a higher yield, pushing the price even lower. With company earnings slowing, this presents repayment problems for the issuing company (i.e. higher default risk), which becomes even more acute when they look to refinance the debt at the end of its term.

High yield bonds also have shorter maturities then other bonds, often maturing in less than 10 years. Prior to 2022, many companies will have locked in much lower interest rates on their bonds while global interest rates were near zero. With these bonds now beginning to mature, the jump in financing rates will present problems if companies do not have the cashflows needed to service their debts.

It is therefore not just the actual default rates on the bonds that matter, but how other investors view the credit risk in the sector. In slowing economies this is likely to result in higher yields, which we have seen in markets since August.

Yields in the ICE BOFA US High Yield index have increased by 7.12% since August, highlighting our point regarding the spread widening in the sector. This is despite yields on US government debt also increasing.

Aside from the effect of increased credit risk, there are potential positives for the sector. Interest rates may continue to rise and the low duration of these bonds mean we will continue to see smaller price depreciation relative to other bonds. Combined with high interest payments, this will potentially mean continued positive performance.

The consensus is also that interest rates will remain at higher levels with cuts not likely until the second half of next year. Investors therefore will not miss out on any price appreciation that other bonds will experience from rate cuts anytime soon (lower interest rate sensitivity works both ways – when interest rates fall, high yield bond prices rise by a smaller margin relative to other bonds).

Companies looking to refinance are also considering using convertible bonds (which can be converted into equity shareholdings) in order to keep costs low which may keep default rates lower in this sector.

There is therefore a balance to be struck between managing exposure to credit risk while maintaining exposure to quality companies (those with higher credit ratings) and a sensible duration risk. As the year progresses and economic growth or contraction becomes more apparent, this will likely shift allocations away from high yield exposure. For now at least, the high rates of interest they pay are resulting in continued positive performance.

Emerging Market (EM) debt

Emerging market (EM) debt has been a closely followed asset class by investors this year, offering returns away from the traditional developed market government and corporate bonds.

An emerging market bond is a type of debt that is issued by a developing country and can be corporate, government or quasi-government (essentially government-owned companies). Emerging market bonds are often classified into two categories based on the currency in which they are issued, external (or “hard currency”) and local currency.

Hard currency bonds are bonds that are issued in major currencies – almost always US dollars – which are typically more stable than EM currencies. Hard bonds therefore tend to be less volatile than local currency bonds because of the stability and security of a liquid global currency. They therefore have a smaller currency risk.

Hard currency bonds carry other risks, however. For example, this year hard currency bond issues in US Dollars have been subject to movements in US interest rates. As US rates go up, the US Dollar strengthens. This makes it more expensive for the issuing company or government to exchange their local currency into US Dollars to pay the interest on the bond, increasing the default risk on the bond and therefore reducing demand (meaning higher yields).

Local debt refers to bonds issued by EM countries and companies in their local currency. Local currency debt carries more credit risk but has become increasingly popular with investors over the past 12 months.

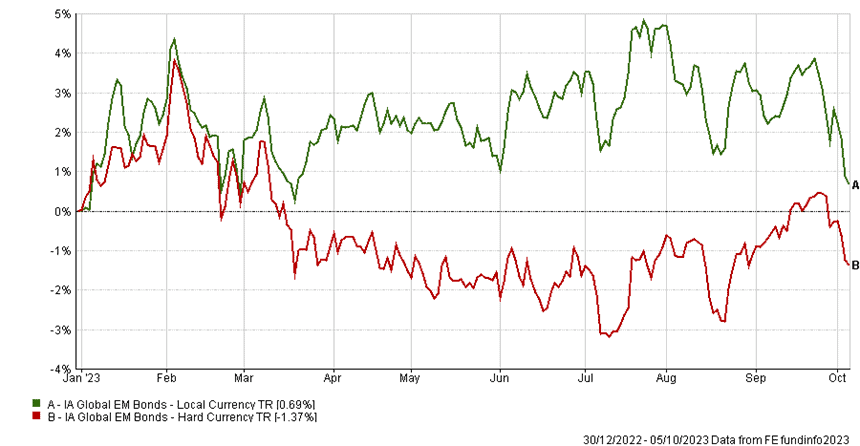

YTD performance of IA emerging market bond sectors in local currencies

As shown above, the price of Global EM bonds has been somewhat volatile year-to-date. In recent weeks, however, local currency EM bonds have performed poorly. This can be explained by the fact that yields on US treasury bonds have increased significantly, which offers a much lower risk return. In addition, emerging markets rely heavily on the performance of developed nations such as the US and China for global trade. An increase in the likelihood of a recession in developed nations will therefore negatively affect emerging market debt and equities alike.

Some investors believe that prospects for local-currency emerging market debt are on the rise. In response to the COVID crisis, many emerging market central banks slashed their interest rates to record lows. To fight the inflation that followed, emerging market central bankers moved, on average, quicker than developed nations. The consensus view is that the central bankers in such nations moved too high, too soon.

This has created an opportunity for emerging market central bankers to cut rates sooner than developed nations. Central banks in several emerging nations have either already initiated a series of interest rate cuts or appear ready to do so.

Some investors believe that there is a large opportunity in Central Europe and Latin America, where supply chain problems and the Russia-Ukraine conflict caused a huge spike in energy and food prices. Central bankers in these areas were forced to make drastic interest rate decisions. The National Bank of Hungary, for example, raised its base rate to 13% last month, marking the end of its rate hike cycle – which has seen interest rates increase by 1200 basis points from 1% since July 2021.

When interest rates in EM countries fall, local currency bonds returns should benefit accordingly. It should be noted that for UK investors any depreciation in local EM currencies relative to the pound will offer “translation” returns as well as bond returns.

There is also an opportunity in hard currency bonds, issued in US dollars. Despite a recent surge in the dollar, the US dollar has weakened against many emerging market currencies over the past year, which has lowered the default risk for most nations as they can convert their local currency into hard currency at a more beneficial exchange rate.

Emerging market securities often carry more risk than similar assets in developed nations. Although EM bonds offer an opportunity for increased capital returns, it is important for all investors to consider risk-adjusted returns when investing in such assets. Emerging assets have historically been inefficient in the sense that the return has not adequately compensated for the risks involved in holding the assets.

Japan

The Japanese economy has been in a state of stagnation for many years, with low growth and low inflation. However, there are some signs that the economy is starting to pick up, with GDP growth of 1.50% in the second quarter of 2023, an annualized increase of 6%. This positive development was driven by robust export expansion.

The major Japanese stock market index, the Nikkei 225, is up 21.19% in 2023 after large volumes of foreign investment. However, much of this increase has been offset for UK investors by currency movements – the year-to-date gains drop to 5.60% when denominated in sterling due to unfavourable exchange rates.

This has helped to boost investor sentiment surrounding the outlook for Japanese equities. This is a rare state since the spectacular crash of 1989 – Japanese markets have notoriously turned even the most optimistic investors cynical.

The Nikkei 225 has failed to reach the high it made at the peak of the Japanese asset price bubble for over 30 years. If you had invested in the Nikkei in December 1989, you would still be down over 19.12% nominally, even more so if you account for inflation. For comparison, the S&P 500 would have returned you over 2000% in the same time period.

Long-term performance of the Nikkei 225 Index.

Since then, the Bank of Japan (BoJ) has maintained an ultra-loose monetary policy, with interest rates set at near-zero, even with the recent tick up in inflation to 4%.

This has helped to support the economy and financial markets, but it has also led to a weakening of the yen. The yen has fallen by around 13.50% against the US dollar since the start of 2023 owing to interest rate differentials. An investor would be unwise to hold Japanese Yen, with rates presently yielding 0%, when you can get over 5% in US rates by holding dollars. This is evidenced by the fact that Japanese investors are the biggest holders of US bonds globally.

The BoJ is also one of the first central banks to experiment with yield curve control, which is a financial device used to supress short- and medium-term bond yields by buying an unlimited amount of government bonds at a set price, therefore creating a ceiling for how high yields can go and a floor for the price. This is vital to fund retirees in a country with severely ageing demographics as pension funds maintain high exposure to government bonds close to retirement age.

The outlook for Japan today looks a lot rosier, with corporate reform coming from government and a focus on healthier capital markets. Blackrock Investment Institute has recently stated that they are going overweight Japanese equities “due to strong earnings, share buybacks, and other shareholder-friendly corporate reforms.”

Analysts state that Japan is changing its corporate view from stakeholder-orientated to shareholder-orientated. The corporate reforms will also help to reduce the number of so-called “zombie companies” (a company that only survives by taking on debt and rolling it over at low interest rates), by potentially tapering back the yield curve control, letting inflation run higher, and incentivising companies to distribute excess cash to shareholders.

According to the regular Bank of America fund manager survey, respondents are the most overweight Japan they have been since 2018. This could spell a near term pullback as markets rarely go with the consensus when everybody is on the same side of the boat. This optimism may be already priced in with the rally we have seen so far in 2023.

However, there is no denying that the longer-term future for Japan looks brighter for shareholders in a world where other developed nations may struggle. Our view is that Japanese equities look attractive at current valuations, with long term performance relying on company performance in the new environment set by the Japanese government.

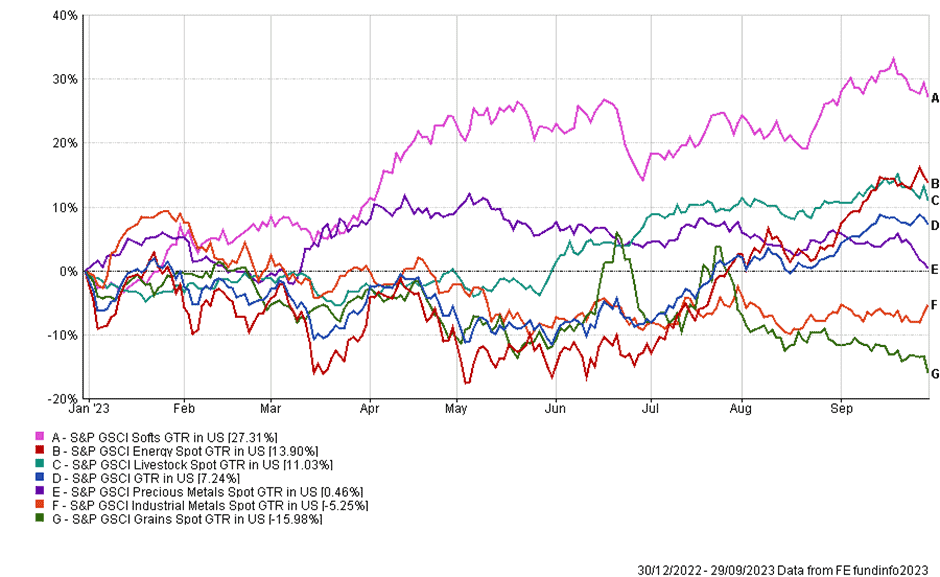

Commodities

2023 has been a very fragmented and volatile year in the commodities industry. Softs, energy, livestock, and precious metals are up 27.31%, 13.90%, 11.03%, and 0.46%, respectively, whilst industrial metals and grains are down 5.25% and 15.98%, respectively. The broader index (the S&P GSCI) is up 7.24%. Commodities are fundamentally driven by demand and supply, both of which play a vital part in the overall price of any given commodity.

Year-to-date performance of various commodity groups.

“Softs” are agricultural commodities that are used to produce food, beverages, and other consumer products, including coffee, cocoa, sugar, and cotton.

As a group, they have been the best performing commodities in 2023 due to a range of factors. Demand for softs has been strong despite calls for a global slowdown. However, the main contributor to the rising prices has been weather-related damage, mainly the hurricanes that hit the US last fall and lower yields in South America due to warmer than average temperatures.

One of the most volatile commodity groups of all and perhaps the one that affects consumers the most is energy. As mentioned in the introduction, the reason is that demand for energy is described by economists as “inelastic”, which means that demand for energy changes very little based on price. If the price of beef goes up, you may just have chicken instead that week. However, if the price of electricity or the price at the fuel pump goes up, you have very little alternatives.

Since the mid-point of this year the S&P GSCI Energy is up 18.12%. This move has largely tracked the rapid rise in oil over the past few months. Oil is often considered to be the most important commodity as it is essentially the fuel for the world. The huge move upwards has mostly been down to two factors: continued strong demand and restricted supply.

Economic activity has been as strong as ever coming out of the pandemic, and global oil consumption is nearly at pre pandemic levels with no sign of slowing down as more developing countries become more dependent on oil-based products. Although the West aims to phase out oil consumption in the transition to net zero, less fortunate and developing countries may not have the luxury choose this more expensive option.

On the supply side, we must talk about the Organisation of Petroleum Exporting Countries (OPEC), mainly Saudi Arabia and Russia. As some of the largest oil exporters in the world, they have an outsized influence over the price of a barrel of oil because of their ability to restrict or expand global supply. So far in 2023, OPEC has restricted supply with talks of further restrictions towards the end of the year.

We believe that Saudi Arabia needs $91 per barrel for oil in order to balance its books and to fund its large infrastructure spending. Therefore, as crude is currently trading at around $85, we see potential for more price increases. Excluding any exogenous events, there is likely heavy resistance above this level as higher prices incentivise producers to come online and oversupply the market, pushing the price back down. This process is not instant and may take time, but the only cure for high prices is high prices.

Livestock commodities include cattle, sheep, hogs, and poultry. This is a commodity price that can easily be tracked at the local butcher when you get the price for your Sunday roast. This, like many other products, has been on the rise recently due to shrinking cattle herds, continued beef demand, and higher labour and fuel costs. To maintain already razor thin margins, farmers have had to pass various increased costs through to buyers. In the US, a prolonged drought in the Midwest has damaged grasslands so much that the U.S. Department of Agriculture forecasts declining supplies potentially through to 2026.

Precious metals are another kettle of fish. This group include metals such as gold, silver, and platinum. Unlike industrial metals where their demand is driven by manufacturing, precious metals are mainly used as a store of value and a hedge against inflation. For example, throughout history gold has widely been used as money because of its ability to act as common value between parties.

In theory, it should be able to protect your money against inflation as it is a real asset and will revalue against the weaker currency. It has a long track record of doing so, however, in more recent times it has failed to do so. Some investors may be sceptical of gold because it does not produce any regular cash flow (unlike a stock or bond, which pay dividends or interest) but we believe that it will continue to work as a long-term hedge against inflation.

On the other hand, you have the more cyclical industrial metals such as copper, steel, and aluminium. These metals have lots of manufacturing uses and tend to be extremely cyclical, generally following the business cycle. As global economic output rises so does demand for these metals, and so too the price. Many investors closely watch the price of copper for its ability to predict where the global economy is going as it is a vital input in most electronic goods. Copper has already fallen this year, siding with those who see the potential for a global slowdown.

The final commodity group that we will discuss is grains such as wheat, corn, and soybeans. Again, demand for these goods is relatively inelastic because it is hard to find an alternative for the foods containing these commodities. Therefore, looking at the supply side tells the majority of the story. No surprise, the GSCI grains index hit its last high since 2014 at the start of 2022, when Russia invaded Ukraine. This had an adverse effect on prices as the Ukraine is a large exporter of grains to most of Europe. This being said, grains have fallen 29.06% since this time, indicating that we have adjusted global supply chains to accommodate for this.

In our view, a granular approach must be taken when investing into commodities as each commodity, even within the same commodity group, will have different supply and demand dynamics. Each side of the equation must be looked at in equal measure to come to a sensible conclusion. Broadly looking at the index, commodities will likely not fare well if we enter a global slowdown, but the opposite will be true in the event of more supply chain shocks. For this reason, it is difficult to tell what the immediate future holds for this sector.

Robert Dougherty, Associate IFA

Ryan Carmedy, Graduate Trainee IFA

Harry Downing, Graduate Trainee IFA

October 2023

This article is not a recommendation to invest and should not be construed as advice. The value of an