While this may seem pessimistic over the short-term, in our view there is still plenty to be optimistic about over the longer-term. With increasingly progressive advances in AI, battery technology and digital banking (to name a few), these growth opportunities serve as big tailwinds for global equity markets. We will touch on this later in the commentary.

Back in the present, global demand is starting to slow with manufacturing output falling and unemployment beginning to rise.

The effect of interest rate rises will be felt in all major economies for months to come. The influence of rate increases takes time to filter through to the real economy and with UK growth already sluggish, the outlook is not bright over the short-term.

The US, on the other hand, has a mixed outlook (depending on who you ask!). Many commentators mention how resilient the US economy has been. This is true but does not reflect what the rest of this year will entail – only in the months to come will we see how the economy performs under the pressure of tighter financial conditions.

European growth is showing signs of a slowdown with the Italian economy shrinking, surprising investors on the downside. Decreases in manufacturing output will hit the Eurozone particularly hard for the rest of the year, with the German economy particularly vulnerable to this downturn.

The outlook for China is also somewhat gloomier. The expected surge in growth from the lifting of pandemic lockdowns has not materialised, leading to pressure on the government to introduce further stimulus into the economy.

The push for a cleaner global economy faces headwinds from China. One of the world’s largest producers and exporters of commodities poses a potential risk to this drive. Recently, for example, China has imposed controls on the exportation of Gallium and Geranium, two key components in battery technology.

Furthermore, China has increased its investment into the metals and mining sector. This looks like the start of a move to capture a large volume of commodity supplies, all of which will put pressure on the clean energy drive and potentially impacting on the US Inflation Reduction Act further down the line.

In more exciting news, a hearing is underway in the US as recent claims from a US intelligence officer suggest that the government is holding alien hardware for research (it is curious that extra-terrestrials always seem to visit the US, and nowhere else in the world). As usual we will update you if this has any implications for investment markets! The truth is out there…

Areas of focus

- US technology stocks continue their drive upwards, with companies like Meta reporting earnings above expectations.

- Quality bonds are overweight in portfolios as high-yield bonds face increased credit risks, especially if a potential recession materialises.

- Global government bonds are preferred to Chinese government bonds as the potential for further monetary loosening will decrease the yield on Chinese debt.

- Small-cap stocks still face further downward pressure, continuing the theme from last year.

- Local currency emerging market debt continues to be popular as local currencies are less swayed by US monetary policy and movements in the US dollar. Emerging market equities are also popular for shorter-term gains

- Emerging market equities are also popular for shorter-term gains.

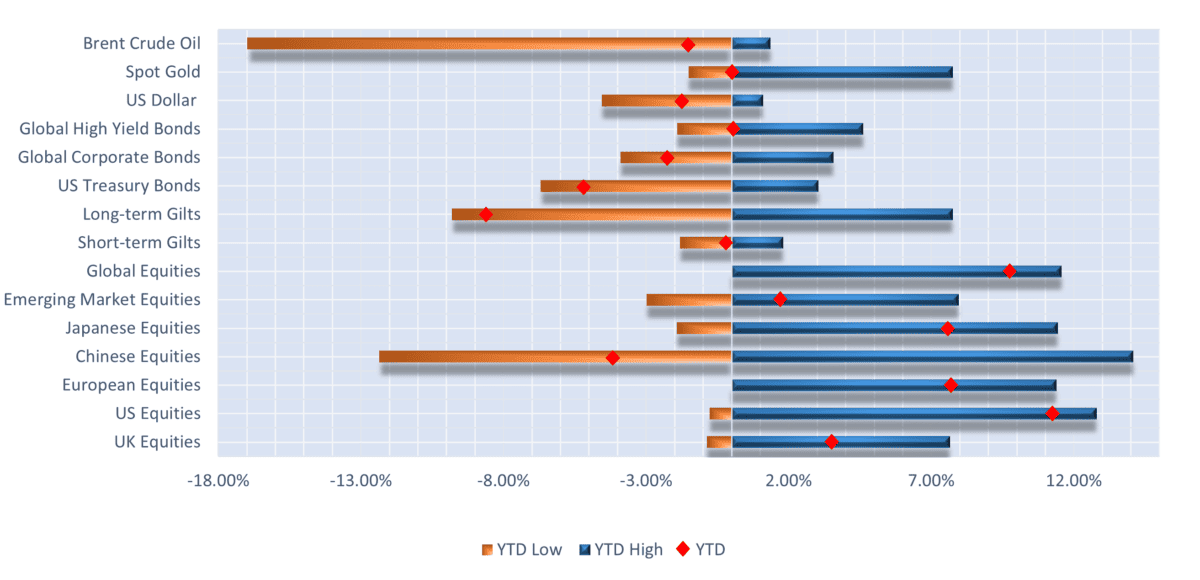

Selection of assets YTD returns and YTD range of returns as at 08.08.2023 (the two ends of the bars represent the range of YTD returns and the red dots represent the current YTD return). Indexes used: FTSE All-Share, Russell 3000, STOXX Europe 600, MSCI China, MSCI Japan, MSCI Emerging Markets, FTSE UK Conventional Up To 5 Years, FTSE UK Conventional Over 15 Years, ICE BOFA US Treasury, ICE BOFA Global High Yield, ICE BOFA Global Corporate, US Dollar Index, S&P GSCI Gold Spot, S&P GSCI Brent Crude Spot. Returns hedged back to GBP with exception of US Dollar which is in US Dollar terms. Data from FE Analytics and MarketWatch. Correct as of 08.08.2023.

UK

Economic backdrop

The big news in the UK this month was that headline CPI inflation finally had a meaningful drop from an annualised rate of 8.7% in May, to 7.9% in June. This was a bigger drop than markets had expected, with markets previously pricing in a rate of 8.2%.

Other inflation measures such as core inflation (which strips out volatile energy and food prices), services inflation and goods inflation fell by 0.2%, 0.2% and 1.2% respectively. Despite these falls, inflation still remains high with core inflation sitting at 6.9%.

Markets reacted very positively to this news as any falls in inflation are potential signs that interest rates may not have to go much higher than the 5.25% they currently sit at. In the US and Europe inflation has fallen markedly and the hope is that the UK will now follow this pattern, having diverged since late last year. However, as we saw inflation still rising in May, the Bank of England will need to see a sustained pattern of falling inflation before any drops in interest rates are considered.

The labour market is still very tight and the risk is that without unemployment rising, wage growth will remain high which will keep inflation elevated. Unemployment rose by 0.2% over the last few months, currently sitting at 4.0%, but again we will need a see a sustained rise above the recent historically low levels. There is a case for unemployment sticking at lower levels as companies fear they may not be able to hire back lost workers when conditions improve, and therefore the UK might experience a “low unemployment” recession.

The biggest risk which has now crossed investors’ minds is that as any changes in interest rates tend to take at least 18 months to have their desired effect on the economy, and as we are 17 months on from the first interest rate rise, we should now start seeing a sustained pattern of economic damage… and we are indeed seeing just that.

Manufacturing and service sector surveys show that companies are cutting back on production, while consumers are spending less on services. Last month we saw consumers withdraw a record amount from savings, and when these savings are exhausted we are likely to see a bigger drop in GDP figures. More consumers will be coming to the end of their fixed rate mortgage deals and will see an increase in their interest costs.

GDP for the three months to May showed no signs of growth, putting the UK in a precarious position. While investors are more accepting that there may be a recession, it could prove to be deeper than anticipated with the effect of further rate rises only now coming into play.

Markets expected the 0.25% increase in interest rates which we saw materialise earlier this week, and now pricing suggests one more interest rate rise is expected this year. Inflation is expected to come down, settling at around 3%, while GDP growth is presently expected to contract but not deeply.

Equity markets

Over the past month all UK equity indices have gained in value, despite lagging earlier in the month. The FTSE 250 gained the most, moving up by 3.71%, while the FTSE 100 and FTSE AIM moved 1.91% and 2.01% respectively. This was on the back of the lower-than-expected inflation figures which drove the indices upwards.

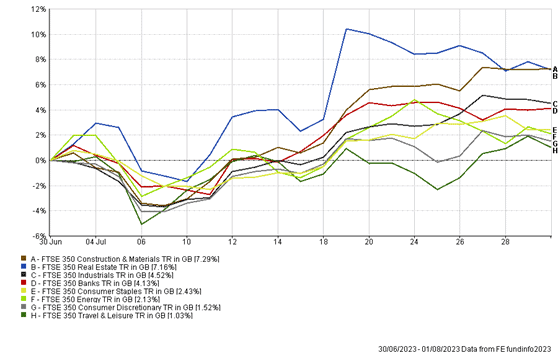

Shares of property companies and construction companies rose the most while travel and leisure companies gained modestly (see chart below).

Property companies have struggled this year, with YTD performance sitting at just 1.16%. Recent gains do not reflect any underlying fundamentals but rather are revised reflections on where interest rates may end up. In our view the property sector will continue to face headwinds for the rest of the year and next year and is still not an attractive asset class to hold.

Despite rising interest rates and tighter consumer disposable income, consumer discretionary and travel and leisure sectors have double digit performance YTD, and over the past month performance has not lagged. It is likely that we will see slower or negative performance in these industries going forward as consumer savings deplete and interest rate effects start to materialise.

1 month performance of FTSE equity sectors

Hedge funds have lost billions of dollars of capital this year betting against the travel industry, while somewhat counter-intuitively the industry has provided strong returns.

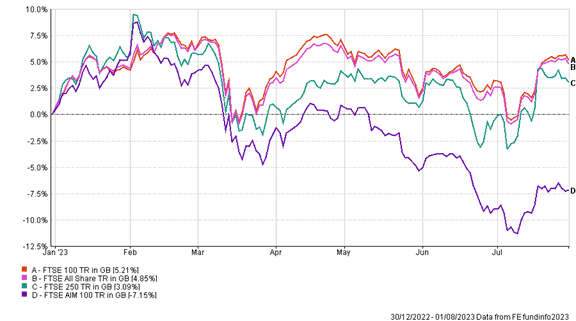

YTD only the AIM index is in negative territory despite some recent respite. In times of economic uncertainty and tighter financial conditions, smaller and newer companies tend to struggle. Small cap stocks generally do best relative to large caps when coming out of a recession and when profit margins are expanding.

Margins currently are contracting, especially for smaller companies with reduced pricing power. Margins usually expand when demand picks up and firms cannot increase productivity or hire workers fast enough. This is not something that we will likely see in the next year.

A global perspective is that companies’ earnings projections do not fully reflect any economic damage ahead. With this in mind, our view is that the AIM index is likely to struggle for the rest of the year. The FTSE 100 and 250 may benefit from a continued shift in investor sentiment to value stocks, which make up a larger proportion of UK markets than others such as the US.

In the long run, the UK economy faces major headwinds from structural issues, a lack of competitiveness, lack of innovation and a depressed consumer confidence. The discount between the value of US and UK equities is around 40% currently, and until these structural issues are fixed it is unlikely this discount will reduce.

YTD performance of UK equity indices

Bond yields

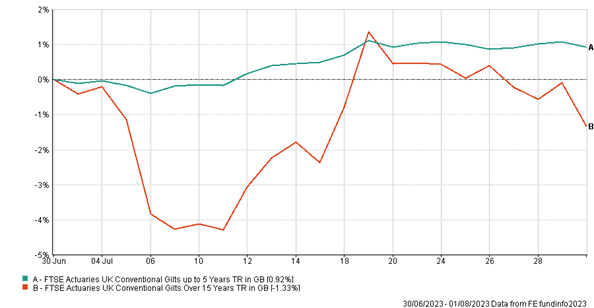

Alongside the fall in the rate of inflation, UK Gilt yields also fell. Both the 2- and 10-year gilt yields have fallen over the past month, but yields still remain highly elevated relative to past periods, and we expect this to continue as investors demand a greater term premium for holding these bonds. Inflation will likely rest at higher levels than the Bank of England’s target of 2% and this will keep yields higher.

The 2-year yield remains above the 10-year yield and this inversion still points to an upcoming recession. The spread has closed slightly which may indicate a softer recession than was previously thought. We will continue to see high volatility in bond yields and direction will be driven by upcoming inflation and labour market data. While investors have mostly focused on these data sets, GDP growth will again come into the picture.

Typically we would see yields fall when a recession is expected, however there is still continued doubt as to how the Bank of England will change interest rates in a recession. We think that rates will not fall nearly as quickly as they typically have in past recessions, keeping bond yields elevated.

| Current Yield (as at 24/07/2023) | One month Change | YTD Change | |

| 2 year Gilt yield | 4.916% | -0.78% | 12.39% |

| 10 year Gilt yield | 4.032% | 2.39% | 7.66% |

Long-term government bond indices have had negative performance over the past month (as we can see by rising yields) while bonds on the shorter maturity have had positive performance. The chart below highlights the increased volatility longer term bonds exhibit due to higher interest rate sensitivity.

One month performance of UK government bond indices

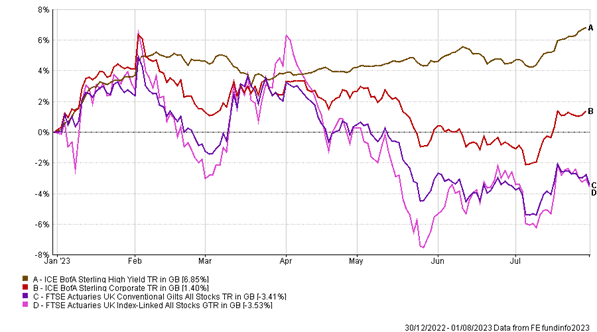

YTD performance of UK corporate and government bond indices

The chart above shows the performance of UK government bonds and corporate bonds. We can see that the government bond indices have dropped in value as yields have risen, but more interesting is the performance of the corporate and higher yield corporate bonds (also referred to as junk bonds due to their low credit rating).

Corporate bonds started the year positively as investors preferred them to government bonds for their higher yields and their equity-like characteristics. Corporate bonds offered good interest and the potential for capital growth if yields came down. We since saw a steady decline in their value as interest rates looked likely to be higher for longer and a recession seemed probable. Recent inflation data boosted their return as yields dropped.

High yield bonds have performed better than corporate bonds with higher credit ratings this year, but in our view this is likely to change over the rest of the year. The reason for this outperformance is that high-yielding bonds have a lower interest rate sensitivity and lose less capital when interest rates increase. They also have higher coupon rates which provide a higher income return.

High-yield bonds are often issued by smaller, higher growth companies. In the UK these bonds are dominated by the retail industry. We can already see the potential trouble ahead looking at Wilko, which has run into financial difficulties.

Companies have had strong balance sheets for a while, but these smaller growth companies tend to be less financially secure and so do not do well in a recessionary or difficult environments. When falling consumer demand leads to lower earnings, we are likely to see increased default rates.

High-yield bonds have risen over the past year, and any smaller company looking to refinance will be refinancing at a yield which has more than doubled, effectively doubling their interest payments.

For the rest of the year yields should moderate but will remain higher than we have previously seen. Short-term yields will remain more stable but will miss out capital growth if and when expectations of lower future interest rates materialise. Historically these bonds have also underperformed longer term bonds in a recessionary environment.

US

Aliens aside, US markets continue to push higher as we move into the second half of the year. This has come on the back of slowing inflation data, a strong Q2 GDP report and the potential for 5.25-5.50% being the Federal Reserve’s terminal rate. Investor sentiment is buoyant as attention focuses on company earnings to evaluate whether equities are truly worth their high valuations.

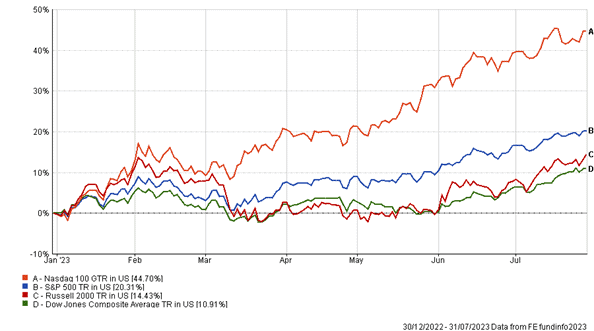

During July the Russell 2000, an equally weighted index composed of smaller market capitalisation stocks, led the markets gaining 6.10%. The Russell has lagged the more technology and large cap orientated indexes since the start of the year as investors have piled into the so-called “magnificent seven” (Microsoft, Apple, Amazon, Google, Tesla, Nvidia, and Meta). We could see this trend continue as investors rotate into smaller cap stocks which have not participated in the recent rally as much as their large cap counterparts.

The Nasdaq 100 and S&P 500 took a short breather, but moved steadily higher, returning 3.84% and 3.18% respectively. We have also seen a resurgence of the Dow Jones Composite Average, up 4.36% on the month, as investors see a brighter future for the blue-chip names if the US miraculously avoids a recession. Large technology companies make up a huge part of these indices now, so for US markets to continue to move higher, tech will likely have to continue to lead the way.

YTD performance of US stock market indices

The bond market is sending different signals, despite the equity market priced for perfection. The 2- and 10-year treasury yields climbed to their highest level since the March banking crisis. As of the end of July, the 2-year treasury is yielding 4.86% and the 10-year is yielding 3.96%, both having traded above 5% and 4% during the month.

The 2-year yield remains relatively flat compared with the start of July while the 10-year has crept up over 0.10%. Nothing has changed in the yield curve situation, the inversion remaining adamant that a recession is on the horizon.

This rate hike cycle has been characterised by catching investors off guard, with most market participants not believing that the Fed could take rates above 3%, let alone 5%. The bond market remains in this mindset and if we do see “higher for longer” rates a lot of investors could be caught out.

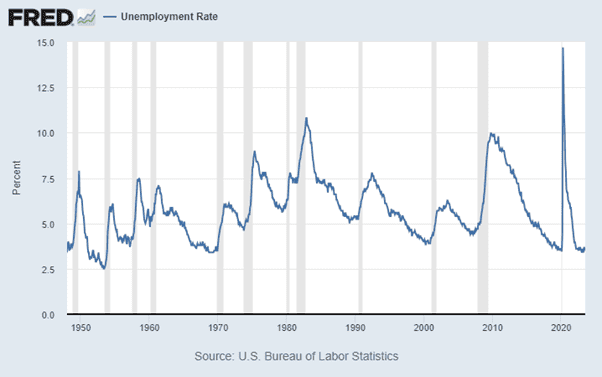

Since our last commentary, US jobs and inflation reports have been released. Non-farm payrolls came in at lower than expected but still increased by 209,000, with the unemployment rate ticking down 0.1% to 3.6%. Government jobs contributed the most to the gain, adding 60,000 jobs, whilst retail lost 11,000 jobs.

Wages also increased by 4.40% from a year earlier, pointing to a resilient US labour force. Investors must be wary that the unemployment rate has often been at its lowest point in the cycle immediately before a recession, based on data going back to 1950 (see below).

Chart showing US unemployment rate (blue line) and past recessions (shaded grey bar). Source U.S. Bureau of Labor Statistics.

Inflation data also fuelled positive market sentiment, rising just 0.2% in June and 3% from a year ago. This is the lowest inflation has been seen March 2021 – however, it is still above the Fed’s 2% inflation target.

As mentioned in July’s asset class commentary, core CPI (CPI minus volatile items like food and energy) is Fed Chairman Jerome Powell’s preferred measure, and this increased by 0.2% and 4.8% year over year. Inflation may change course slightly in the coming months as the base effects of high oil prices from a year ago wear off and the price per barrel starts to rise again.

In response to this data, the Federal Reserve decided to increase its benchmark rate by 25 basis points to a target range of 5.25%-5.5%. This was much anticipated based on guidance from the last meeting. Markets now look forward to the next meeting on September 20th ,where current pricing suggest an 82.5% probability of a pause or “skip”.

One notable takeaway from the July meeting was that Powell stated that they are going to become more data dependent going forward and that they have “a long way to go” to meet their 2% inflation target. The problem with being data dependent is that there is inevitably a lag between waiting for the data and taking the appropriate action. We saw this last year when the Fed was very slow to react to the growing inflation problem in the US.

Second quarter GDP news also came out in July, the report stating that GDP grew at a 2.4% annualized pace during the quarter. Consumer spending was the main driving force for the growth, accounting for 68% of all economic activity.

This consumer spending may be down to excess savings built up during lockdowns and also as a result of government stimulus. However, the San Francisco Federal Reserve estimated that these savings have fallen to around $500 billion from $2.1 trillion in August 2021, leading analysts to suggest that savings might dwindle by the end of the year.

Over half of the companies in the S&P 500 have now reported their second quarter earnings with 80% of them reporting earnings per share above estimates. The 5- and 10-year averages for companies beating their earnings estimates are 77% and 73%, respectively. This being said, S&P earnings are projected to show the largest year over year decline since the second quarter of 2020, down 31.6%. This decline will make it the third quarter in a row where the index has reported a decrease.

All of which, in our view, points to the concept of multiple expansion mentioned in our June 2023 commentary. Earnings are projected to grow in the second half of the year, 0.2% for Q3 and 7.5% for Q4. Twelve-month forward P/E’s are still extended from their 10 -year average of 17.4, currently the S&P 500’s twelve-month forward P/E is 19.4.

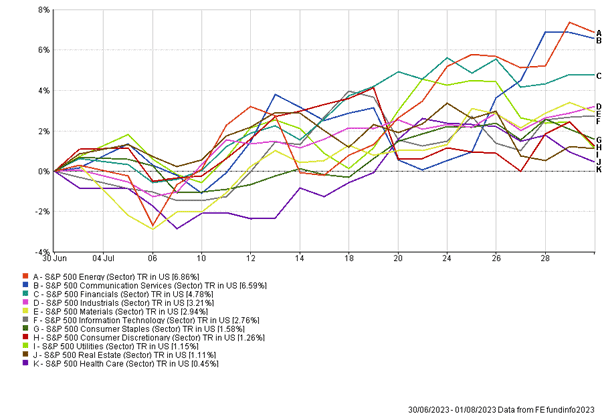

Energy was the best performing sector in the month of July, gaining 6.86%. Although energy earnings have been weak due to a significant decline in the price of a barrel of oil, the fundamentals have started to turn around, leading investors and markets to have a more optimistic outlook on the future.

This was closely followed by communication services, gaining 6.59% in the month. Names such as Alphabet (Google’s parent company), Meta (formerly Facebook), and Netflix are big components of this sector. All these companies have benefitted from the recent rise in AI speculation and more positive data regarding the economy.

One of the weaker performers in the month was real estate as the sector battles with the long, delayed and variable effect of interest rate rises. Sectors which are more sensitive to interest rates may come under more pressure in the second half of this year as companies and consumers have to refinance their debt at higher rates than when the debt was initially issued.

One month performance of select US stock sectors

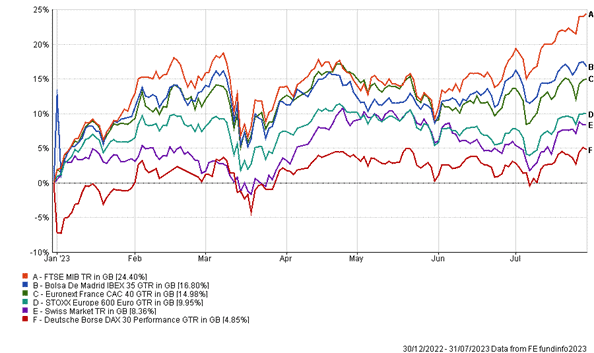

Europe

The Italian stock market continues to outperform in 2023, adding 4.55% in July and a magnificent 24.40% on the year, despite a Q2 GDP decline of 0.3%. This comes as a surprise to analysts predicting a flat reading and 0.9% rise on the year. Despite the gloomy data, the Italian government assures that their 1% growth target for the year is still within reach.

This has put even more pressure on Italian Prime Minister, Meloni, as she already faces backlash on her “citizen’s income” poverty relief scheme. Over 1.7 million households benefited from the scheme last year but employers state that it discourages the unemployed to take jobs, creating artificial labour shortages. The Italian unemployment rate currently sits at 7.4%, higher than the EU rate of 5.9%, a eurozone all-time low.

The German stock market lags the rest of Europe on the year, returning 4.85% on the year and 0.57% in the month. All-time highs remain in sight; however, investors look at slowing manufacturing as a sign of more difficult times to come. The German market is very heavy in automobile manufacturers, and BMW led the pullback after reporting earnings that failed to meet analyst expectations.

European markets have largely been a positive surprise this year, being a viable option for most investors, unlike years gone by. US markets have outperformed Europe to such a degree in the last decade that there has been no alternative. Despite great adversity, European markets have persisted, pointing to favourable returns once difficulties subside.

YTD performance of European stock market indices

Similarly to the US, the German Bund market is also inverted with the 2-year yield at 2.99% and the 10-year yield at 2.62%. This comes on the back of another 25-basis point rate hike from the European Central Bank, raising the deposit rate in the 20-nation bloc to 3.75% with Christine Lagarde reportedly considering a pause in September.

The rationale behind the ninth consecutive rise is to bring Europe’s persistently high inflation down to the target rate. Eurozone inflation is currently running at 5.3%, down from 5.5% in June. Food inflation is the main contributor to this as Europe continues to experience the disruptions from the Russian invasion of Ukraine, a key food exporter. Food inflation was at 11.6% in June.

European bond markets will largely follow base rate changes by the European Central Bank along with future expectations, also looking less attractive when inflation rates are high as investors must price in a lower “real” rate of return. As Europe has higher structural inflation bond yields may have to rise further to compensate, further pushing down prices.

France and Spain both traded sideways for the month as they take a rest from their 14.98% and 16.80% moves since the start of the year. Eurozone second quarter GDP beat expectations, expanding 0.3%. Economists, however, suggest that this number is misleading as GDP growth without France and Ireland would have been 0.04% (France growing 0.5% and Ireland growing 3.3%). Spain also posted a respectable growth rate of 0.4%.

Megatrends driving future markets

It is not untrue to say that when you read the news at the moment, it can appear bleak. Not a day goes by without a reference to economic data, and this is exactly what is driving markets over the short-term. The key is that it is short-term, and that over the long-term markets are driven by structural growth (think railways, the internet and now AI) and not by macroeconomic data or forecasts.

Therefore, when we look to the future we see many opportunities and sources of long-term returns.

These ‘mega trends’ encompass a variety of areas, and some of the most important are listed below. While some trends may prove to be more important than others, all of them in some way will drive innovation which in turn will drive cashflows and shareholder value. The trends will generate value in different ways, with AI technology affecting specific sectors, while income equality shifts affect specific regions or countries.

- AI technology

- Digital banking

- Decarbonisation (i.e. a clean energy shift)

- Space exploration

- Income equality shifts

- Ageing populations

- Emerging markets

If we look at AI technology, we have seen very recently how stock markets have reacted to the recent developments. Nvidia Corporation has climbed by over 210% on the back of impressive results from its generative AI technology. Who had previously mentioned this business? Not many people, but now we are seeing AI everywhere. While this is only short-term performance, as more businesses battle for market share in this industry we should see the value fragment more widely.

An important point to note is that it is not about the value of the business itself but instead the quality of its cashflows that define value. Across most sectors this is being ignored due, mostly, to pessimism over short-term macroeconomic data.

If we look back to the “dot com” bubble in the early 2000s, many businesses which were highly valued failed. This is an example of the value of these companies not actually reflecting the quality of their cashflows. Many of the failed businesses were not profitable and failed to make efficient use of their capital. This is an important lesson when looking at any future trends – not all businesses will succeed and generate value, but all can be caught up in short-term “hype”.

The growing Indian economy has huge potential for investment as the aim is to shift more of the world’s largest population into higher income brackets, i.e. a rebalancing of the income equality. They are also moving towards a completely digital currency.

One of the most talked about areas is the decarbonisation of economies in an effort to combat climate change. A wealth of industries have the potential to benefit from this theme. From companies developing the new technology to infrastructure companies reshoring and building the new energy sources, there is huge long-term potential here.

Of course there are also opportunities from the biggest threats of the future. While cleaner energy has an obvious link to climate change, the insurance industry will feel the effects too, for example. Increased premiums due to higher payouts from increased environmental disasters will affect value and some of the less financially stable businesses will fail.

While this section is a very brief summary, a whole article could be devoted to this topic – showing that there are long-term opportunities that make investing at the moment actually very exciting!

Robert Dougherty, Associate IFA

Ryan Carmedy, Graduate Trainee IFA

Harry Downing, Graduate Trainee IFA

August 2023

This article is not a recommendation to invest and should not be construed as advice. The value of an

investment can go down as well as up, and you may get less back than you invested.