As you may have noticed, AI is the new buzzword at the moment. While some people are worrying about a possible Terminator-like future and the potential for vast numbers of job losses, there are many benefits AI can bring in a wide range of areas such as medicines, healthcare, transport and the environment.

Technology stocks have reacted very well to AI with investors pricing in high levels of growth. The UK unfortunately misses out on most of this activity as it has typically failed at attracting these types of businesses in the past.

Another headline from this month is that UK inflation fell, albeit less than investors and economists had expected. The big energy-price increases of last year fell out of the picture, but food price inflation is still increasing.

Inflation in the UK is higher than that of Europe and the US and this is the concern on investors’ minds. The Bank of England reacted to the recent inflation data by raising interest rates by a further 0.25% to 4.5%. The probability of further rate rises has increased and the likelihood of any rate cuts is lower, with some now predicting a “terminal interest rate” of 5.75% or even 6%.

That said, the FTSE 100 and FTSE 250 are still in positive territory for the year while the FTSE AIM index has been struggling since March. All UK indices are down over the last month.

The US debt ceiling issue, as widely expected, resolved itself. This is not over though, and in our view the longer-term effects could impact markets for years to come. US debt is currently 118% of GDP and is increasing, while inflation is high and expected to stick at higher levels than previously thought.

While inflation reduces the real value of government debt (as inflation increases tax receipts and GDP while reducing the value of debt as a percentage of economic output), it also increases both the expectation and the realisation of increased interest rates.

So what are the long-run impacts? Increased debt costs will almost inevitably lead to either increased taxes, reduced spending or increased borrowing, all of which reduce long-term GDP growth. Furthermore, we expect increasing US debt issuance will lead to higher bond yields – on the basis that an increased supply of bonds without matching demand will lead to lower bond prices and hence higher yields.

The probability of continued global interest rate rises is higher than investors previously thought and this also is likely to keep bond yields elevated.

While European growth has been resilient relative to investors’ expectations, the outlook for individual countries is extremely varied, with Germany moving into a technical recession and Italy upgrading its economic forecasts.

European inflation did indeed fall more than expected, but with Central Banks singing from the same hymn sheet of higher rates for longer, it is likely we will see at least two more interest rate rises in the bloc.

Economic activity in China is worrying investors. With exports dropping by 7.5% year-on-year the pressure will be to stop the declining gains the country benefited from when lockdown restrictions were lifted. Imports however did better than expected, adding some weight to the argument that the domestic recovery from pandemic lockdowns is on track. Monetary policy is loose in China and any further monetary loosening would help to boost equity values while weakening the Chinese currency, the Renminbi.

The direction and magnitude of inflation movements has always been an impossible task to predict, and the best way to manage this risk is to keep a diversified portfolio of bonds and equities, spreading allocations between global regions to minimise any idiosyncratic risk.

Areas of focus

- Amid a potential shift into the recessionary phase of the cycle and still high volatility, quality companies are still preferred and will continue to be.

- UK Gilts yields continue to rise, approaching their one year high. Gilt yields relative to last year are attractive, with shorter duration bonds preferred.

- US Treasury yields continue to rise amid a higher for longer mindset for policy rates.

- Energy stocks are still in favour as energy prices are expected to remain elevated over the medium term. Any further tax pressure on these companies will impact values though.

- With share prices continuing to rise, a recessionary environment is a key risk. In our view equity valuations do not accurately reflect any potential for drops in earnings. Long term are equities are likely to outperform bonds, as has always been the case.

- Corporate bonds are not as popular with investors as they were at the start of the year. With tighter financial conditions, quality is preferred and credit spreads between high yield and government bonds are, we believe, still too tight.

- Large-cap companies are likely to reap the rewards from AI technology developments due to cost accessibility.

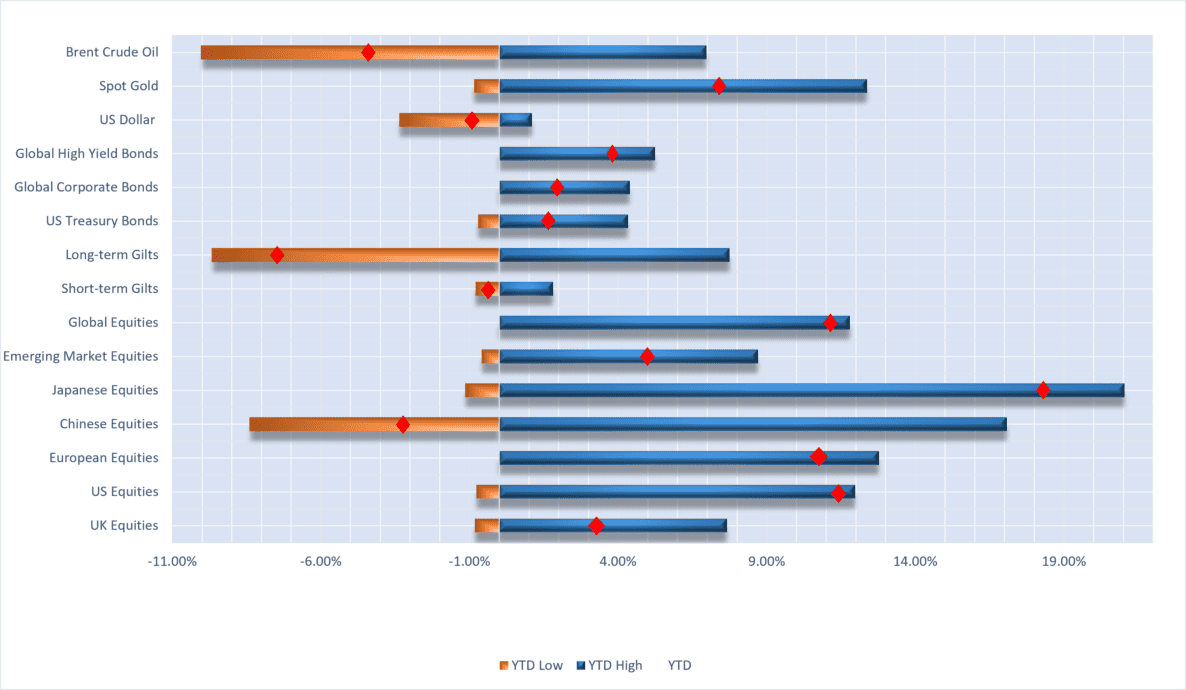

Selection of assets YTD returns and YTD range of returns as at 09.06.2023 (the two ends of the bars represent the range of YTD returns and the red dots represent the current YTD return). Indexes used: FTSE All-Share, Russell 3000, STOXX Europe 600, MSCI China, MSCI Japan, MSCI Emerging Markets, FTSE UK Conventional Up To 5 Years, FTSE UK Conventional Over 15 Years, ICE BOFA US Treasury, ICE BOFA Global High Yield, ICE BOFA Global Corporate, US Dollar Index, Spot Gold, Brent Crude Oil. Returns hedged back to GBP with exception of Spot Gold, Brent Crude Oil and US Dollar which are in US Dollar terms. Data from FE Analytics and MarketWatch. Correct as of 09.06.2023.

UK

Economy

In a 7-2 vote, the Bank of England raised interest rates for the 12th consecutive time in May, lifting its base rate from 4.25% to 4.50% – the highest level in 15 years.

While the headline CPI figure dropped below 10% for the first time since August last year to 8.7%, the UK still has a much bigger inflation problem than most advanced economies. This CPI figure was higher than the 8.2% that markets were expecting, prompting investors to rethink their investments in both bond and equity markets.

While the most recent unemployment data points to a loosening labour market, the Bank of England governor warned that Britain could be entering a wage-price spiral where rising salaries feed through into renewed increases in inflation. Continued public sector strikes could add to this problem over the coming months if the government decides not to meet the demands of the trade unions.

Rising food prices exaggerated UK grocery spending last month and has elevated CPI in recent months, prompting many consumers to cut back on discretionary purchases. Recent figures from KPMG revealed that UK food sales increased by an annual rate of 9.6% in May, above the average rate of 6.9%. Despite this, overall consumer spending only rose 3.6%, well below the rate of inflation. This suggests that consumers are having to forgo luxury purchases to offset the rising price of essential items such as food and energy. This will have future implications for companies with a focus on luxury items, such as car manufacturers and retailers, negatively impacting their future earnings and thus their current share price valuations.

Energy prices

To reflect the recent fall in wholesale gas prices, Ofgem has lowered the energy price cap which is set to expire at the end of June. This means that a typical household will now pay £2,074 a year for their gas and electricity, starting in July. This reduction is a sigh of relief for those struggling with the cost-of-living crisis, but the figure remains over £1,000 more per year than pre-pandemic levels.

While a reduction in the energy price cap means that consumers will pay less in the short term, gas prices are expected to remain elevated for the rest of the decade. Research from energy analysis firm Cornwall Insight suggests that prices will be higher and more volatile until the end of this decade, and this volatility will be passed onto the consumer through higher bills.

This multi-year disruption is partly due to the cost of the transition to clean energy, which is expected to be $9.2 trillion globally per annum until 2050 (the year many governments and companies are aiming to achieve net zero). This comes after Rishi Sunak and Joe Biden met last month, pledging to accelerate the clean energy transition and strengthen critical mineral supply chains between the two major economies.

UK equities

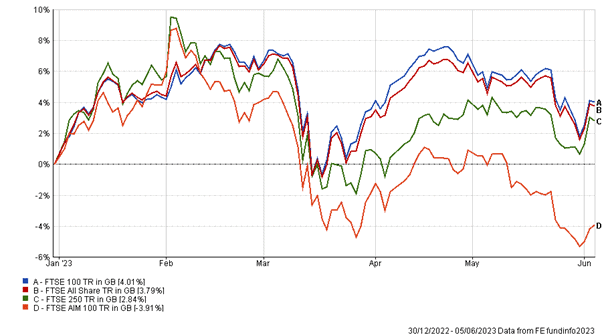

YTD performance of UK stock market indices

Weaker commodity prices led to a difficult May across the board for UK equities, with the FTSE All-Share Index falling 4.60% during the month. The FTSE 100 fell 4.93% while the FTSE AIM 100 suffered the most, down 6.16% over the month. Unlike the tech-driven US indices, UK markets did not receive the same boost from speculative investors looking for returns in AI and the recent boost from London’s energy, mining and commodity stocks seems to be waning for now. However, the expectation for longer-term higher energy prices will provide some support for the companies in these sectors.

This again both highlights and reflects the UK’s lack of competitiveness in attracting global technology companies, particularly when compared to the US stock market, which we discussed in last month’s commentary.

Fixed income

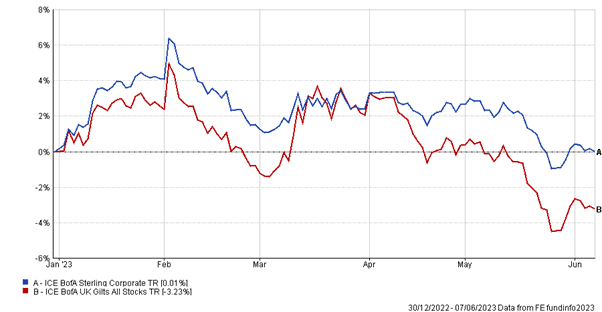

YTD performance of UK bond indices

Higher than expected core CPI figures last month forced markets to rethink future interest rate expectations in the UK. Markets now expect interest rates to peak at 5.5% later this year, with some investors concerned that the terminal rate may be even higher.

This forced UK bond yields up again, and gilts ended the month as one of the worst performers among global government bonds. This is shown in the chart above, with the UK gilts index hitting a YTD low in May and down 3.43% since the start of the year – the yield on a 10-year gilt is around 4.27% at the time of writing, up 16.70% since the beginning of the year.

Mortgages

According to the latest research, over 367,000 five-year fixed-rate mortgage terms are due to be renewed over the next 12 months, most of which are presently enjoying a fixed rate under 2%. These mortgages have an average outstanding balance of £170,000. If existing homeowners revert to a variable rate mortgage, average monthly repayments are expected to increase by around £300. This is expected to cause an even more severe squeeze on the spending power of these consumers.

A recent study by Halifax indicated that house prices fell by 1% in May compared to last year. Despite this decrease in prices, mortgage brokers now believe that the housing market crash many predicted at the end of last year is unlikely.

The latest figures also suggest that housing market transactional activity is down 58%, which signifies a significant reduction in demand. However, unless homeowners in financial difficulty are forced to sell en masse, the limited supply of houses on the market will prevent a crash.

US

YTD Performance of US equity markets

The month of May can be best described as a tale of two economies, the artificial intelligence haves and the artificial intelligence have nots. The technology heavy Nasdaq 100 rose 7.85% during the month (up a huge 32.94% year to date), while the S&P 500 only rose 0.47% (12.43% year to date). Conversely, the Dow Jones Composite Average lost 3.30% in May and is up just 3.21% since the start of the year.

The top 10 stocks in the S&P now make up over 30% of the index. NVIDIA is the poster child of this rising AI wave after posting extremely bullish earnings, above analysts’ expectations – the company now has a market cap of nearly $1 trillion. Although AI technology has the potential to improve economic efficiency significantly, markets may be getting a bit ahead of themselves. New technologies take years to integrate into current infrastructures and this is not something we will see anytime soon.

This is a common theme with new technologies and herd behaviour has, including recently, led to some overly-optimistic share price values. Investors are desperate to find some value in a world of economic despair, so short-term volatility in these recent risers will likely be elevated, we think.

S&P earnings per share are actually down on the year, therefore all the recent growth is just multiple expansion. The price to earnings ratio (which is a measure of how expensive or cheap a company is) of the S&P currently sits at 24.74, against a historical average of 14.93.

This suggests earnings must catch up or prices could suffer. We think it the latter is likely. Why? In our view, stock prices do not fully reflect a recessionary environment (when company earnings will fall). In this scenario of economic contraction, if earnings are falling then company valuations will be adjusted downwards and prices will fall.

Fundamentals do support valuations to some extent in the tech sector, but when this changes is something to monitor.

Going forward, it is likely that large cap companies in the tech sector will benefit more than smaller companies from the AI drive. AI models are hugely expensive to develop and train, meaning the accessibility for larger companies is much greater.

US bond yields increased in reaction to the Fed increasing their benchmark rate to 5.00-5.25%. Since our last commentary the US 2-year and 10-year yield curve has become even more inverted, and the spread has widened from 0.54% to 0.85%. The US 2-year and 10-year bonds now yield 4.56% and 3.72%, respectively.

Markets now price in a 73.60% chance of a pause at the Fed’s next meeting on 13th June. Although recent rate increases in Canada have spooked investors yet again, prompting bond yields to rise as they reassess the chances of interest rate increases.

Bond yields may fall in the next 12 months, sending prices higher if the Fed is forced to cut rates in response to a recession or a so-called “black swan” event. If neither of these situations arise, rates could stay higher for longer as inflation comes down and the labour market stays tight.

We currently believe that the Fed will not cut rates much, if at all, in response to a recession unless inflation comes down drastically. The Fed’s main goal is controlling inflation, and as we have said in past commentaries, they will use a recession as another tool in their inflation battle. Manufacturing data already points to a slowdown in the US economy, while other economic indicators do not.

Research by Goldman Sachs puts a 25% probability of a US recession this year, down from their previous estimate of 35%, with core inflation ending the year at 3.7%. This is still above the Fed’s target rate of 2.0%. Research by Blackrock, however, suggests that a recession will begin in the US.

The US non-farm payroll increased by 339,000 in May, much higher than expectations. The unemployment rate rose slightly to 3.70%, giving the Fed further reason to stick with high rates. Wages have also increased 4.30% from a year ago, although positive, this is nearly in line with current inflation readings of 4.90%. In general, if wages do not keep up with inflation we are likely to see a slowdown in consumption.

As predicted in our last commentary, the debt ceiling fiasco was all just political theatre, with Congress coming to an agreement at the eleventh hour. Markets only rose slightly on this news, as a US default was always the expected outcome. Increasing the debt limit kicks the can down the road and we will likely be having a similar conversation in a few years’ time. A potential impact of this for investors is that the Treasury is now able to increase their debt issuance, putting downward pressure on bond prices which will keep yields elevated for longer.

The US debt to GDP ratio is currently 118.77%, higher than most other developed nations with the exception of Japan. The debt to GDP ratio of a country can be used to gauge how likely a country is to repay its debts. As discussed in the last commentary, the US can take on more debt than other countries because of the higher demand for US dollars. Whether this will be sustainable in the long run is a different question.

Europe

April’s eurozone inflation data confirmed that headline inflation increased by 0.1% to 7.0%, due to a 3.3% increase in energy price inflation. In a sharp contrast to the UK economy, core inflation dropped 0.1% to 5.6% as a rise in services inflation was offset by a move down in food inflation. Food price inflation declined by 1.9% to 13.5%, the first major decline in two years.

In line with expectations, the ECB delivered a 25-basis point hike, raising the base rate to 3.25%. Investors are currently expecting two further rate hikes by the ECB, with deposit rates peaking at 3.75% later this year.

Eurozone consumer confidence barely changed in May but a monthly fall in new car registrations pointed to a continued weakness in the demand for luxury goods in the region, signalling that European consumers are beginning to feel the effects of the cost-of-living crisis.

Although the wider European economy recently avoided a recession, a negative Q1 2023 GDP figure of 0.1% confirmed that the 20 countries using the euro as their currency slipped into a technical recession this past quarter. A recession is defined as two consecutive quarters of economic decline (in the last quarter of 2022, Eurozone GDP also decreased by 0.1%).

A downward revision of previous GDP estimates for Germany released in April meant that Europe’s largest economy slipped into recession in the last quarter. While the German economy seems to have weathered the energy crisis surprisingly well, reduced international demand is starting to take its toll on its industrially-focused economy. Formerly described as the European powerhouse economy, could Germany become Europe’s problem child?

Fixed income

In May, German government bunds witnessed the biggest rally in global bonds markets since the mini banking crisis in March this year, sending yields tumbling by 20 basis points. This was mainly led by cooling inflation figures and a weak German GDP figure, pointing to a possible end to recent ECB rate hikes.

In a weaker economy with falling inflation investors prefer government bonds. Investors’ risk appetite decreases and the risk of default is much lower.

European bond yields have risen in the first week of June due to ‘surprise’ rate hikes from the Reserve Bank of Australia and Bank of Canada banks, indicating that interest rates still have further to go to bring inflation back to targets. In response, 2-year German bund yields currently sit higher at around 3.10% while the yield on 10-year German bunds sits at around 2.47%.

Investors currently need to tread carefully when investing in global fixed income. Government bonds remain hostage to shifting data which one day might support the case for further rate increases and the next day suggest peak rates are close, keeping volatility elevated.

Equities

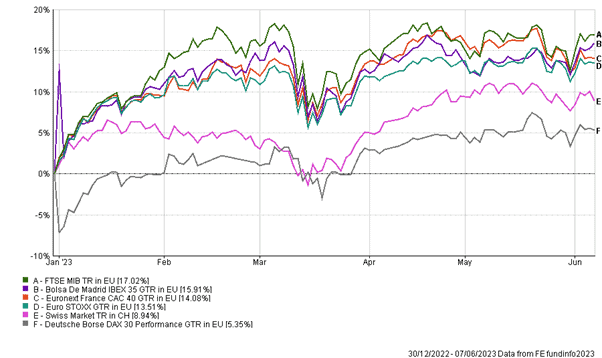

YTD performance of European stock market indices

After a strong start to 2023, European equites dropped 2.1% in May. Despite this, YTD returns for most European indices remain in double digits. European shares were helped by the resolution of the US debt ceiling saga. Furthermore, the European Union revised up its forecasts for the bloc’s growth in 2023, contrary to investors’ growing concerns about a recessionary environment.

In recent years, investors have been questioning whether European stock markets can compete with their US counterparts.

After the pandemic, global central banks cut interest rates to support struggling economies. In response, 2021 smashed records for stock market listings as asset prices surged and companies jumped on to public markets.

In 2022, however, global financial markets were hit by multiple interest rate hikes to tackle record-high inflation.

The value of European listings in 2022 dropped to its lowest point in a decade, according to Dealogic data. Just one deal — the €75bn listing of Porsche in Frankfurt — accounted for 60% of capital raised. In the UK, newly listed companies raised 90% less in 2022 than the year prior, with just 45 companies listing in London.

The massive outperformance of the US financial markets in recent years, both in terms of listing numbers and in the valuations that US listed companies can command, is creating a flight risk for European stock markets, including the London Stock Exchange. This is especially relevant with global economies fighting to create attractive environments for clean energy capital.

How European stocks are expected to perform in the short term remains uncertain and will largely depend on inflation levels throughout the year. If core inflation continues to fall in the region, consumer confidence may rise – increasing demand. If energy prices remain sticky, however, the ECB may be forced to raise rates higher and economic growth may suffer accordingly.

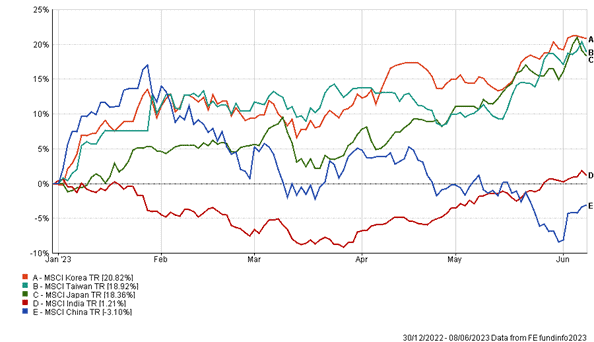

Asia

YTD Performance of Asian stock market indices

Major Asian markets have shown mixed performance in 2023, as the chart above illustrates. South Korea has been leading the pack with gains of 20.82% for the year so far. This increase can be attributed to a return to positive GDP growth of 0.3% in Q1 and strong private consumption data, which grew by 0.5% quarter over quarter. South Korea has a very export-centric economy, which will be influenced by global growth and the risk of a slowdown. China, a big importer of goods from Korea, has helped boost these imports by reopening its economy from the pandemic lockdowns.

Japanese equities have also been strong, returning 18.36% since the start of the year. This is a result of good economic data. Q1 real GDP rose 1.3% year on year as private consumption and foreign investment has been strong. Legendary investor, Warren Buffett, has recently backed Japan by increasing Berkshire Hathaway’s stake in five major Japanese trading houses. Although the outlook may appear positive, Japan’s April inflation figure was high and the Bank of Japan has hinted at winding down their ultra loose monetary policy, both of which could act as headwinds.

The big risk here is unwinding monetary policy too soon and returning to a state of deflation, which has long plagued the Japanese economy.

Taiwan is up 18.92% year to date, riding the new technology and artificial intelligence wave as they are a large computer chip manufacturer. Investing in Taiwan always carries political risk owing to the ongoing tensions with China. China views Taiwan as part of its territory, conducting military drills around the island, and not ruling out taking control by force. As an emerging market, these risks cannot be discounted and so the risk and reward relationship is elevated.

China’s strong start to the year, on recovery hopes, has diminished as the recovery has proved less strong than expected. Exports fell by 7.5% in May from a year ago, far below the 0.4% estimates. After rising by over 15%, the Chinese stock market is now down 3.10% on the year. Geopolitical risk and poor demographics make up the majority of the bear case when investing in China.

Unlike China, India has very strong demographics with a young and growing population. The population of India overtook China for the first time, and while China’s population is declining, India’s is still growing rapidly. This presents a different set of opportunities for India, while China will have a more challenging time ahead.

This is likely to be beneficial for the Indian economy going forward, as GDP growth can essentially be viewed as the sum of population growth and productivity growth plus debt.

After a decade of (mostly) strong stock market returns, the Indian market is relatively flat on the year, having risen by 1.21% since January. Investors may be sceptical that India can replicate the growth seen by China in the last 50 years. Indian manufacturing only makes up 15% of GDP, much lower than that of China and so India will have to find other sources of growth.

Much of India’s future potential depends on whether it can achieve a shift in income equality, moving more consumers from the lower class to the middle class. Investing in India is a long-term strategy with high risks and potentially high rewards. Following India’s strong economic and investment market performance in recent years, investors are now starting to re-evaluate whether the equity market is priced appropriately.

Robert Dougherty, Associate IFA

Ryan Carmedy, Graduate Trainee IFA

Harry Downing, Graduate Trainee IFA

June 2023

This article is not a recommendation to invest and should not be construed as advice. The value of an

investment can go down as well as up, and you may get less back than you invested.